Pizza Hut 1999 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 1999 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

|

|

43

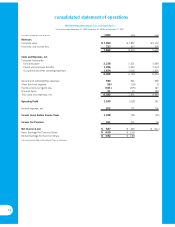

prior to the Spin-off. In connection with the Spin-off, we bor-

rowed $4.55 billion to fund a dividend and repayments to

PepsiCo, which exceeded the net aggregate balance owed at

the Spin-off Date by $1.1 billion.

Segment Disclosures. Effective December 28, 1997, we

adopted SFAS No. 131, “Disclosures About Segments of an

Enterprise and Related Information” (“SFAS 131”). Operating

segments, as defined by SFAS 131, are components of an

enterprise about which separate financial information is avail-

able that is evaluated regularly by the chief operating decision

maker in deciding how to allocate resources and in assessing

performance. This Statement allows aggregation of similar

operating segments into a single operating segment if the busi-

nesses are considered similar under the criteria of SFAS 131.

We identify our operating segments based on management

responsibility within the U.S. and International. For purposes

of applying SFAS 131, we consider our three U.S. Core

Business operating segments to be similar and therefore have

aggregated them into a single reportable operating segment.

Internal Development Costs and Abandoned Site

Costs. We capitalize direct internal payroll and payroll related

costs and direct external costs associated with the acquisition

of a site to be developed as a Company unit and the construc-

tion of a unit on that site. Only those site-specific costs incurred

subsequent to the time that the site acquisition is considered

probable are capitalized. We consider acquisition probable

upon final site approval. If we subsequently make a determi-

nation that a site for which internal development costs have

been capitalized will not be acquired or developed, the previ-

ously capitalized costs are expensed at this date and included

in general and administrative expenses.

Fiscal Year. Our fiscal year ends on the last Saturday in

December and, as a result, a fifty-third week is added every five

or six years. Fiscal years 1999, 1998 and 1997 comprised

52 weeks. Fiscal year 2000 will include a fifty-third week. Each

of the first three quarters of each fiscal year consists of 12 weeks

and the fourth quarter consists of 16 or 17 weeks. Our sub-

sidiaries operate on similar fiscal calendars with period end

dates suited to their businesses. Period end dates are within

one week of TRICON’s period end date with the exception of

our international businesses, which close one period or month

earlier to facilitate consolidated reporting.

Direct Marketing Costs. We report substantially all of our

direct marketing costs in occupancy and other operating

expenses in the Consolidated Statement of Operations, which

include costs of advertising and other marketing activities. We

charge direct marketing costs to expense ratably in relation to

revenues over the year in which incurred. Direct marketing

costs deferred at year-end consist of media and related ad pro-

duction costs. We expense these costs when the media or ad

is first used. Deferred advertising expense, classified as pre-

paid expenses in the Consolidated Balance Sheet, was

$3 million in 1999 and $4 million in 1998. Our advertising

expenses were $385 million, $435 million and $517 million in

1999, 1998 and 1997, respectively. The decline in our adver-

tising expense is a direct result of substantially fewer Company

stores as a result of our major refranchising program.

Research and Development Expenses. Research and

development expenses, which we expense as incurred, were

$24 million in 1999 and $21 million in both 1998 and 1997.

Stock-Based Employee Compensation. We measure

stock-based employee compensation cost for financial state-

ment purposes in accordance with Accounting Principles

Board Opinion No. 25, “Accounting for Stock Issued to

Employees,” and its related interpretations and include pro

forma information in Note 15 as required by Statement of

Financial Accounting Standards No. 123, “Accounting for

Stock-Based Compensation” (“SFAS 123”). Accordingly, we

measure compensation cost for the stock option grants to our

employees as the excess of the average market price of our

Common Stock at the grant date over the amount the employee

must pay for the stock. Our policy is to generally grant stock

options at the average market price of the underlying Common

Stock at the date of grant.

Earnings (Loss) Per Common Share. In the accom-

panying Consolidated Statement of Operations, we have

omitted loss per share information for 1997 as our capital struc-

ture as an independent, publicly owned company did not exist

for the entire year.

Derivative Instruments. From time to time, we utilize inter-

est rate swaps, collars and forward rate agreements to hedge

our exposure to fluctuations in variable interest rates.

We recognize the interest differential to be paid or received on

interest rate swap and forward rate agreements as an adjust-

ment to interest expense as the differential occurs. We

recognize the interest differential to be paid or received on an

interest rate collar as an adjustment to interest expense only if

the interest rate falls below or exceeds the contractual collared

range. We reflect the recognized interest differential not yet set-

tled in cash in the accompanying Consolidated Balance Sheet

as a current receivable or payable. If we were to terminate an

interest rate swap, collar or forward rate position, any gain or

loss realized upon termination would be deferred and amor-

tized to interest expense over the remaining term of the

underlying debt instrument it was intended to modify or would

be recognized immediately if the underlying debt instrument

was settled prior to maturity.

We recognize foreign exchange gains and losses on forward

contracts that are designated and effective as hedges of for-

eign currency receivables each period as the differential

occurs. This is fully offset by the corresponding gain or loss rec-

ognized in income on the currency translation of the receivable,

as both amounts are based upon the same exchange rates. We