Pitney Bowes 2014 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2014 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

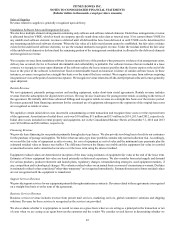

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share amounts)

45

Sales of Supplies

Revenue related to supplies is generally recognized upon delivery.

Standalone Software Sales and Integration Services

We also have multiple element arrangements containing only software and software related elements. Under these arrangements, revenue

is allocated based on VSOE, which is based on company specific stand-alone sales data or renewal rates. If we cannot obtain VSOE for

any undelivered software element, revenue is deferred until all deliverables have been delivered or until VSOE can be determined for

any remaining undelivered software elements. When the fair value of a delivered element cannot be established, but fair value evidence

exists for the undelivered software elements, we use the residual method to recognize revenue. Under the residual method, the fair value

of the undelivered elements is deferred and the remaining portion of the arrangement consideration is allocated to the delivered elements

and recognized as revenue.

We recognize revenue from standalone software licenses upon delivery of the product when persuasive evidence of an arrangement exists,

delivery has occurred, the fee is fixed and determinable and collectability is probable. For software licenses that are included in a lease

contract, we recognize revenue upon shipment of the software unless the lease contract specifies that the license expires at the end of the

lease or the price of the software is deemed not fixed or determinable based on historical evidence of similar software leases. In these

instances, revenue is recognized on a straight-line basis over the term of the lease contract. We recognize revenue from software requiring

integration services at the point of customer acceptance. We recognize revenue related to off-the-shelf perpetual software licenses generally

upon shipment.

Rentals Revenue

We rent equipment, primarily postage meters and mailing equipment, under short-term rental agreements. Rentals revenue includes

revenue from the subscription for digital meter services. We may invoice in advance for postage meter rentals according to the terms of

the agreement. We initially defer these advanced billings and recognize rentals revenue on a straight-line basis over the invoice period.

Revenues generated from financing customers for the continued use of equipment subsequent to the expiration of the original lease term

are recognized as rentals revenue.

We capitalize certain initial direct costs incurred in consummating a rental transaction and recognize these costs over the expected term

of the agreement. Amortization of initial direct costs was $10 million, $11 million and $13 million in 2014, 2013 and 2012, respectively.

Initial direct costs included in rental property and equipment, net in the Consolidated Balance Sheets at December 31, 2014 and 2013

were $22 million and $26 million, respectively.

Financing Revenue

We provide lease financing for our products primarily through sales-type leases. We also provide revolving lines of credit to our customers

for the purchase of postage and supplies. We believe that our sales-type lease portfolio contains only normal collection risk. Accordingly,

we record the fair value of equipment as sales revenue, the cost of equipment as cost of sales and the minimum lease payments plus the

estimated residual value as finance receivables. The difference between the finance receivable and the equipment fair value is recorded

as unearned income and is amortized as income over the lease term using the interest method.

Equipment residual values are determined at inception of the lease using estimates of equipment fair value at the end of the lease term.

Estimates of future equipment fair value are based primarily on historical experience. We also consider forecasted supply and demand

for various products, product retirement and launch plans, regulatory changes, remanufacturing strategies, used equipment markets, if

any, competition and technological changes. We evaluate residual values on an annual basis or sooner if circumstances warrant. Declines

in estimated residual values considered "other-than-temporary" are recognized immediately. Estimated increases in future residual values

are not recognized until the equipment is remarketed.

Support Services Revenue

We provide support services for our equipment primarily through maintenance contracts. Revenue related to these agreements is recognized

on a straight-line basis over the term of the agreement.

Business Services Revenue

Business services revenue includes revenue from presort mail services, marketing services, global ecommerce solutions and shipping

solutions. Revenue for these services is recognized as the services are provided.

We also evaluate whether it is appropriate to record revenue on a gross basis when we are acting as a principal in the transaction or net

of costs when we are acting as an agent between the customer and the vendor. We consider several factors in determining whether we