Pitney Bowes 2014 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2014 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

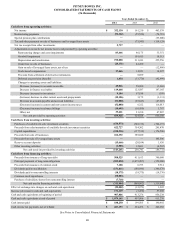

|

|

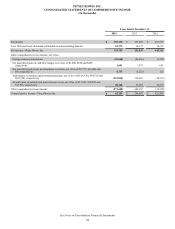

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share amounts)

42

1. Summary of Significant Accounting Policies

Basis of Presentation

The accompanying Consolidated Financial Statements of Pitney Bowes Inc. (we, us, our, or the company) and its wholly owned subsidiaries

have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP). Intercompany

transactions and balances have been eliminated. Certain prior year amounts have been reclassified to conform to the current year

presentation.

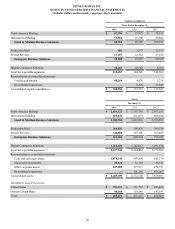

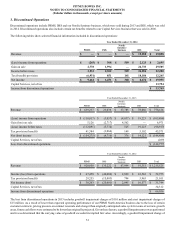

In April 2014, Pitney Bowes of Canada Ltd., a wholly owned subsidiary, completed the sale of its Document Imaging Solutions (DIS)

business, which consisted of hardware (copiers and printers) and document management software solutions to Konica Minolta Business

Solutions (Canada) Ltd. and the related lease portfolio to a business equipment leasing services provider in two separate transactions.

Accordingly, the results of operations of DIS were reclassified as discontinued operations (see Note 3). The cash flows from discontinued

operations are not separately stated or reclassified in the accompanying Consolidated Statements of Cash Flows.

In 2013, we sold our Management Services business (PBMS), Nordic furniture business and International Mailing Services business

(IMS). Further, we made certain organizational changes and realigned our business units and segment reporting to reflect the clients we

serve, the solutions we offer, and how we manage, review, analyze and measure our operations. Historical results have been recast to

present the operating results of these divested businesses as discontinued operations and our segment results have been recast to conform

to the new segment reporting.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires the use of estimates and assumptions that affect the reported

amounts of assets, liabilities, revenues, expenses and accompanying disclosures, including the disclosure of contingent assets and

liabilities. These estimates and assumptions are based on management's best knowledge of current events, historical experience and other

information available when the financial statements are prepared. These estimates include, but are not limited to, revenue recognition for

multiple element arrangements, goodwill and intangible asset impairment review, allowance for doubtful accounts and credit losses,

residual values of leased assets, useful lives of long-lived and intangible assets, restructuring costs, pensions and other postretirement

costs, income tax reserves, deferred tax asset valuation allowance, stock-based compensation expense and loss contingencies. Actual

results could differ from those estimates and assumptions.

Cash Equivalents and Short-Term Investments

Cash equivalents include short-term, liquid investments with maturities of three months or less at the date of purchase. Short-term

investments include investments with a maturity of greater than three months but less than one year from the reporting date.

Investment Securities

Investment securities that management has the positive intent and ability to hold to maturity are classified as held-to-maturity and are

carried at amortized cost. Investment securities not classified as held-to-maturity are classified as available-for-sale and recorded at fair

value, with unrealized gains and losses excluded from earnings and reported in other comprehensive income, net of tax. Purchase premiums

and discounts are recognized in interest income using the effective interest method over the terms of the securities. Gains and losses on

the sale of available-for-sale securities are recorded on the trade date and are determined using the specific identification method.

Investment securities are recorded in the Consolidated Balance Sheets as cash and cash equivalents, short-term investments and other

assets depending on the type of investment and maturity.

During 2014, we determined that for years ended December 31, 2013 and 2012 certain non-cash exchanges of investments were reported

as cash used for purchases of available-for-sale investment securities and cash provided by proceeds from sales/maturities of available-

for-sale investment securities. The Consolidated Statements of Cash Flows for the years ended December 31, 2013 and 2012 have been

revised in this Form 10-K by decreasing cash used for purchases of available-for-sale investment securities and cash provided by proceeds

from sales/maturities of available-for-sale investment securities by $28 million and $64 million, respectively. We have determined that

these adjustments are not material to our consolidated financial statements for any of the affected periods.

Accounts Receivable and Allowance for Doubtful Accounts

We estimate our accounts receivable risks and provide an allowance for doubtful accounts accordingly. We evaluate the adequacy of the

allowance based on historical loss experience, aging of receivables, adverse situations that may affect a customer's ability to pay and

prevailing economic conditions and make adjustments to the allowance as necessary. This evaluation is inherently subjective and actual

results may differ significantly from estimated reserves. Accounts receivable are generally due within 30 days after the invoice date.

Accounts deemed uncollectible are written off against the allowance after all collection efforts have been exhausted and management