Oracle 2014 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2014 Oracle annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

|

|

Table of Contents

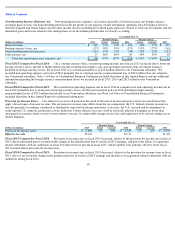

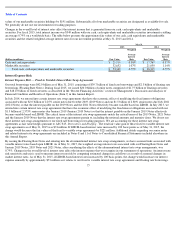

In July 2014, our 3.75% senior notes due July 2014 for $1.5 billion matured and were repaid, and we settled the fixed to variable interest rate

swap agreements associated with such fixed rate senior notes.

Currency Risk

Foreign Currency Transaction and Translation Risks — Foreign Currency Borrowings and Related Hedges

In July 2013, we issued €1.25 billion of 2.25% notes due January 2021 (January 2021 Notes) and we entered into certain cross-currency swap

agreements to manage the related foreign exchange risk by effectively converting the fixed-rate Euro denominated debt, including the annual

interest payments and the payment of principal at maturity, to a fixed-rate, U.S. Dollar denominated debt. The economic effect of the swap

agreements was to eliminate the uncertainty of the cash flows in U.S. Dollars associated with the January 2021 Notes by fixing the principal

amount of the January 2021 Notes at $1.6 billion with an annual interest rate of 3.53%. The critical terms of the cross-currency swap agreements

match the critical terms of January 2021 Notes, including the notional amounts and maturity dates. We do not use these cross-currency swap

arrangements for trading purposes. We are accounting for these interest rate swap agreements as cash flow hedges pursuant to ASC 815. The fair

values of these cross-currency swap agreements as of May 31, 2015 and 2014 were a $(244) million loss and a $74 million gain, respectively.

The changes in the fair values of the cross-currency swap agreements during fiscal 2015 were primarily attributable to the decline in the value of

the Euro relative to the U.S. Dollar. If the Euro weakened by 10% as of May 31, 2015, we estimate the change would decrease the fair values of

the cross-currency swap agreements by $174 million. If interest rates that correspond to the remaining term of the January 2021 Notes decreased

by 100 basis points as of May 31, 2015, we estimate the change would decrease the fair values of the cross-currency swap agreements by $91

million. Additional details regarding our senior notes and related cross-currency swap agreements are included in Notes 8 and 11 of Notes to

Consolidated Financial Statements included elsewhere in this Annual Report.

In July 2013, we also issued €

750 million of 3.125% notes due July 2025 (2025 Notes). We designated the 2025 Notes as a net investment hedge

of our investments in certain of our international subsidiaries that use the Euro as their functional currency in order to reduce the volatility in

stockholders’

equity caused by the changes in foreign currency exchange rates of the Euro with respect to the U.S. Dollar. As a result, the change

in the carrying value of the Euro denominated 2025 Notes due to fluctuations in foreign currency exchange rates on the effective portion is

recorded in accumulated other comprehensive loss on our consolidated balance sheet and is also presented as a line item in our consolidated

statements of comprehensive income included elsewhere in this Annual Report and totaled $208 million of net other comprehensive gains for

fiscal 2015. Any remaining change in the carrying value of the 2025 Notes representing the ineffective portion of the net investment hedge is

recognized in non-operating income (expense), net. We did not record any ineffectiveness during fiscal 2015.

Fluctuations in the exchange rates between the Euro and the U.S. Dollar will impact the amount of U.S. Dollars that we will require to settle the

2025 Notes at maturity. If the U.S. Dollar weakened by 10% in comparison to the Euro as of May 31, 2015, we estimate our obligation to cash

settle the principal portion of the 2025 Notes in U.S. Dollars would increase by approximately $81 million.

Foreign Currency Transaction Risk — Foreign Currency Forward Contracts

We transact business in various foreign currencies and have established a program that primarily utilizes foreign currency forward contracts to

offset the risks associated with the effects of certain foreign currency exposures. Under this program, our strategy is to enter into foreign

currency forward contracts so that increases or decreases in our foreign currency exposures are offset by gains or losses on the foreign currency

forward contracts in order to mitigate the risks and volatility associated with our foreign currency transactions. We may suspend this program

from time to time. Our foreign currency exposures typically arise from intercompany sublicense fees, intercompany loans and other

intercompany transactions. Our foreign currency forward contracts are generally short-term in duration.

We neither use these foreign currency forward contracts for trading purposes nor do we designate these forward contracts as hedging instruments

pursuant to ASC 815. Accordingly, we record the fair values of these contracts as of the end of our reporting period to our consolidated balance

sheet with changes in fair values recorded to our consolidated statement of operations. Given the short duration of the forward contracts, the

amount recorded is

78