Napa Auto Parts 2015 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2015 Napa Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

Genuine Parts Company and Subsidiaries

Notes to Consolidated Financial Statements — (Continued)

December 31, 2015

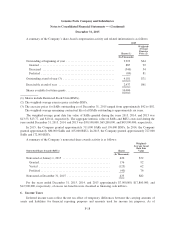

The amount of gross tax effected unrecognized tax benefits, including interest and penalties, as of

December 31, 2015 and 2014 was approximately $17,684,000 and $19,497,000, respectively, of which approx-

imately $9,317,000 and $11,106,000, respectively, if recognized, would affect the effective tax rate. During 2014,

the Company settled certain transfer pricing methodologies with tax authorities, and on a consolidated basis, the

difference, in related payments and refunds and the amount reflected in the tax reserves, was not material.

During the years ended December 31, 2015, 2014, and 2013, the Company paid interest and penalties of

approximately $1,051,000, $14,000,000, and $405,000, respectively. The Company had approximately

$1,746,000 and $1,916,000 of accrued interest and penalties at December 31, 2015 and 2014, respectively. The

Company recognizes potential interest and penalties related to unrecognized tax benefits as a component of

income tax expense.

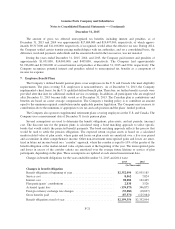

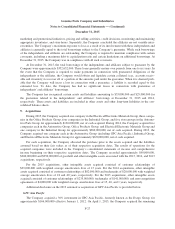

7. Employee Benefit Plans

The Company’s defined benefit pension plans cover employees in the U.S. and Canada who meet eligibility

requirements. The plan covering U.S. employees is noncontributory. As of December 31, 2013, the Company

implemented a hard freeze for the U.S. qualified defined benefit plan. Therefore, no further benefit accruals were

provided after that date for additional credited service or earnings. In addition, all participants who are employed

after December 31, 2013 became fully vested as of December 31, 2013. The Canadian plan is contributory and

benefits are based on career average compensation. The Company’s funding policy is to contribute an amount

equal to the minimum required contribution under applicable pension legislation. The Company may increase its

contribution above the minimum, if appropriate to its tax and cash position and the plans’ funded position.

The Company also sponsors supplemental retirement plans covering employees in the U.S. and Canada. The

Company uses a measurement date of December 31 for its pension plans.

Several assumptions are used to determine the benefit obligations, plan assets, and net periodic (income)

cost. The discount rate for the pension plans is calculated using a bond matching approach to select specific

bonds that would satisfy the projected benefit payments. The bond matching approach reflects the process that

would be used to settle the pension obligations. The expected return on plan assets is based on a calculated

market-related value of plan assets, where gains and losses on plan assets are amortized over a five year period

and accumulate in other comprehensive income. Other non-investment unrecognized gains and losses are amor-

tized in future net income based on a “corridor” approach, where the corridor is equal to 10% of the greater of the

benefit obligation or the market-related value of plan assets at the beginning of the year. The unrecognized gains

and losses in excess of the corridor criteria are amortized over the average future lifetime or service of plan

participants, depending on the plan. These assumptions are updated at each annual measurement date.

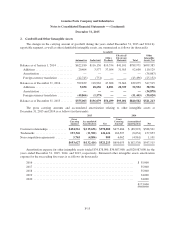

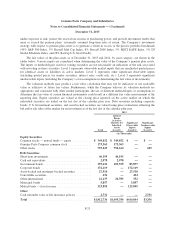

Changes in benefit obligations for the years ended December 31, 2015 and 2014 were:

2015 2014

(In Thousands)

Changes in benefit obligation

Benefit obligation at beginning of year ............................ $2,352,094 $2,035,185

Service cost ................................................. 8,562 7,824

Interest cost ................................................. 98,088 102,465

Plan participants’ contributions .................................. 2,838 3,526

Actuarial (gain) loss .......................................... (139,573) 346,875

Foreign currency exchange rate changes .......................... (35,082) (18,697)

Gross benefits paid ........................................... (87,571) (125,084)

Benefit obligation at end of year ................................. $2,199,356 $2,352,094

F-21