Napa Auto Parts 2015 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2015 Napa Auto Parts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

|

|

Genuine Parts Company and Subsidiaries

Notes to Consolidated Financial Statements — (Continued)

December 31, 2015

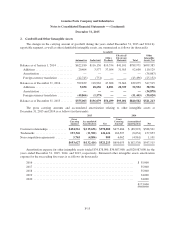

expected defaults and, therefore, the need to revise estimates for bad debts. For the years ended December 31,

2015, 2014, and 2013, the Company recorded provisions for doubtful accounts of approximately $12,373,000,

$7,192,000, and $8,691,000, respectively. At December 31, 2015 and 2014, the allowance for doubtful accounts

was approximately $10,693,000 and $11,836,000, respectively.

Merchandise Inventories, Including Consideration Received From Vendors

Merchandise inventories are valued at the lower of cost or market. Cost is determined by the last-in, first-out

(LIFO) method for a majority of automotive parts, electrical/electronic materials, and industrial parts, and by the

first-in, first-out (FIFO) method for office products and certain other inventories. If the FIFO method had been

used for all inventories, cost would have been approximately $438,510,000 and $434,790,000 higher than

reported at December 31, 2015 and 2014, respectively. During 2014 and 2013, reductions in inventory levels in

automotive parts inventories (2013) and industrial parts inventories (2014 and 2013) resulted in liquidations of

LIFO inventory layers. The effect of the LIFO liquidations in 2014 and 2013 was to reduce cost of goods sold by

approximately $8,000,000 and $5,000,000, respectively.

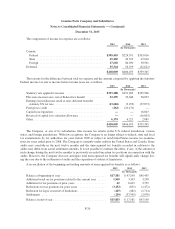

The Company identifies slow moving or obsolete inventories and estimates appropriate provisions related

thereto. Historically, these losses have not been significant as the vast majority of the Company’s inventories are

not highly susceptible to obsolescence and are eligible for return under various vendor return programs. While

the Company has no reason to believe its inventory return privileges will be discontinued in the future, its risk of

loss associated with obsolete or slow moving inventories would increase if such were to occur.

The Company enters into agreements at the beginning of each year with many of its vendors that provide for

inventory purchase incentives. Generally, the Company earns inventory purchase incentives upon achieving

specified volume purchasing levels or other criteria. The Company accrues for the receipt of these incentives as

part of its inventory cost based on cumulative purchases of inventory to date and projected inventory purchases

through the end of the year. While management believes the Company will continue to receive consideration

from vendors in 2016 and beyond, there can be no assurance that vendors will continue to provide comparable

amounts of incentives in the future.

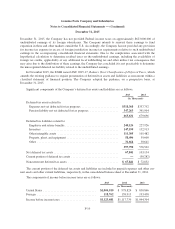

Prepaid Expenses and Other Current Assets

Prepaid expenses and other current assets consist primarily of prepaid expenses, amounts due from vendors,

and income taxes receivable.

Goodwill

The Company reviews its goodwill annually in the fourth quarter, or sooner if circumstances indicate that

the carrying amount may exceed fair value. The Company tests goodwill for impairment at the reporting unit

level, which is an operating segment or a level below an operating segment, which is referred to as a component.

A component of an operating segment is a reporting unit if the component constitutes a business for which dis-

crete financial information is available and management regularly reviews the operating results of that compo-

nent. However, two or more components of an operating segment are aggregated and deemed a single reporting

unit if the components have similar economic characteristics.

The present value of future cash flows approach was used to determine any potential impairment. The

Company determined that goodwill was not impaired and, therefore, no impairments were recognized for the

years ended December 31, 2015, 2014, and 2013.

F-10