Motorola 2011 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2011 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

98

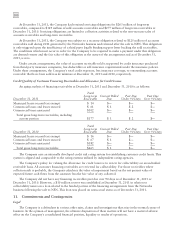

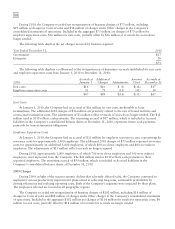

The table above includes securities on loan as part of a securities lending arrangement of $6 million of common

stock and equivalents, $6 million of U.S. government and agency obligations and $1 million of corporate bonds. All

securities on loan are fully cash collateralized.

December 31, 2010 Level 1 Level 2 Level 3 Total

Common stock and equivalents $48 $ — $— $ 48

Commingled equity funds — 62 — 62

U.S. government and agency obligations — 4 — 4

Corporate bonds — 7 — 7

Mortgage-backed bonds — 8 — 8

Asset-backed bonds — 2 — 2

Commingled bond funds — 34 — 34

Commingled short-term investment funds — 4 — 4

Invested cash — 1 — 1

Fair value plan assets $48 $122 — $170

The table above includes securities on loan as part of a securities lending arrangement of $4 million of common

stock and equivalents, $2 million of U.S. government and agency obligations and $1 million of corporate bonds. All

securities on loan are fully cash collateralized.

Valuation Methodologies

Level 1—Quoted market prices in active markets are available for investments in common and preferred stock

and common stock equivalents. As such, these investments are classified within Level 1.

Level 2—The securities classified as Level 2 are comprised primarily of corporate, government, agency and

government-sponsored enterprise fixed income securities. These securities are priced using pricing services, bid/offer,

and last trade. Prices may also be obtained from brokers, counterparties, fund administrators, online securities data

services, or investment managers. Fixed income securities, including short-term instruments, may be priced using

pricing models comprised of observable inputs which include, but are not limited to, market quotations, yields,

maturities, call features, and the security’s terms and conditions.

In determining the fair value of the Company’s foreign currency derivatives, the Company uses forward

contract and option valuation models employing market observable inputs, such as spot currency rates, time value

and option volatilities. Since the Company primarily uses observable inputs in its valuation of its derivative assets

and liabilities, they are classified as Level 2 assets.

Level 3—Securities that do not have actively traded quotes as of the financial statement date. Determining the

fair value of these securities requires the use of unobservable inputs, such as indicative quotes from dealers,

extrapolated data, proprietary models and qualitative input from investment advisors. As such, these securities are

classified within Level 3.

At December 31, 2011, the Company had $437 million of investments in money market mutual funds classified

as Cash and cash equivalents in its consolidated balance sheet. The money market funds have quoted market prices

that are generally equivalent to par.

Using quoted market prices and market interest rates, the Company determined that the fair value of long-term

debt at December 31, 2011 was $1.6 billion, compared to a face value of $1.5 billion. Since considerable judgment

is required in interpreting market information, the fair value of the long-term debt is not necessarily indicative of the

amount which could be realized in a current market exchange.

All other financial instruments are carried at cost, which is not materially different than the instruments’ fair

values.