Kodak 2002 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2002 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

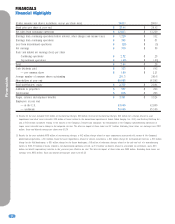

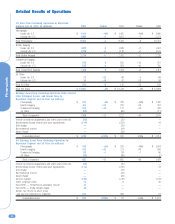

Financials

9

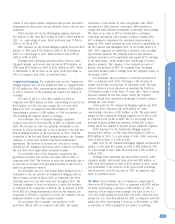

obligations. In the event that the actual results of these items

differ from the estimates, an adjustment to the warranty

obligation would be recorded.

PENSION AND POSTRETIREMENT BENEFITS

Kodak’s defined benefit pension and other postretirement benefit

costs and obligations are dependent on assumptions used by

actuaries in calculating such amounts. These assumptions, which

are reviewed annually by the Company, include the discount rate,

long-term expected rate of return on plan assets, salary growth,

healthcare cost trend rate and other economic and demographic

factors. The Company bases the discount rate assumption for its

significant plans on the estimated rate at which annuity contracts

could be purchased to discharge the pension benefit obligation. In

estimating that rate, the Company looks to the AA-rated corporate

long-term bond yield rate in the respective country as of the last

day of the year in the Company’s reporting period as a guide. The

long-term expected rate of return on plan assets is based on a

combination of formal asset allocation studies, historical results

of the portfolio and management’s expectation as to future returns

that are expected to be realized over the estimated remaining life

of the plan liabilities that will be funded with the plan assets. The

salary growth assumptions are determined based on the

Company’s long-term actual experience and future and near-term

outlook. The healthcare cost trend rate assumptions are based on

historical cost and payment data, the near-term outlook and an

assessment of the likely long-term trends.

The Company evaluates its expected long-term rate of return

on plan asset (EROA) assumption annually for the Kodak

Retirement Income Plan (KRIP). To facilitate this evaluation, every

two to three years, or when market conditions change materially,

the Company undertakes a new asset liability study to reaffirm

the current asset allocation and the related EROA assumption.

Wilshire Associates, a consulting firm, completed a study (the

Study) in September 2002, which led to several asset allocation

shifts and a decrease in the EROA from 9.5% for the year ended

December 31, 2002 to 9.0% for the year ended December 31,

2003. This factor, coupled with a decrease in the discount rate of

75 basis points from 7.25% for 2002 to 6.5% for 2003, and the

fact that the transition asset, which provided approximately $56

million of income in 2002, is fully amortized as of December 31,

2002, is expected to lower total pension income in the U.S. from

$197 million in 2002 to pension income in the range of $49

million to $59 million in 2003. This decrease in income will be

partially offset by a decrease in pension expense in the

Company’s non-U.S. plans in the range of $53 million to $65

million. Additionally, the Company increased its healthcare cost

trend rate assumption with respect to the Company’s most

significant postretirement plan, the U.S. plan, from 9% for 2003,

decreasing to 5% by 2007 (as discussed in the Company’s 2001

Annual Report on Form 10-K), to 12% for 2003, decreasing to

5% by 2010. This increase in the healthcare cost trend rate

assumption, coupled with the decrease in the discount rate, is

expected to increase the cost of this plan from $222 million in

2002 to a range of $254 million to $310 million in 2003. All

these factors have been incorporated into the Company’s earnings

outlook for 2003.

Actual results that differ from our assumptions are recorded

as unrecognized gains and losses and are amortized to earnings

over the estimated future service period of the plan participants

to the extent such total net recognized gains and losses exceed

10% of the greater of the plan’s projected benefit obligation or

the market-related value of assets. Significant differences in

actual experience or significant changes in future assumptions

would affect the Company’s pension and postretirement benefit

costs and obligations.

In accordance with the guidance under Statement of

Financial Accounting Standards (SFAS) No. 87, the Company is

required to record an additional minimum pension liability in its

Consolidated Statement of Financial Position that is at least equal

to the unfunded accumulated benefit obligation of its defined

benefit pension plans. In the fourth quarter of 2002, due to the

decreasing discount rates and the weak performance of the global

equity markets in 2002, the Company increased its net additional

minimum pension liability by $577 million and recorded a

corresponding charge to accumulated other comprehensive income

(a component of stockholders’ equity) of $394 million, net of

taxes of $183 million. If discount rates and the global equity

markets’ performance continue to decline, the Company may be

required to increase its additional minimum pension liabilities and

record further charges to stockholders’ equity in the future.

Likewise, if discount rates increase and the performance of the

global equity markets improve, the Company could be in a

position to reduce its minimum pension liability and reverse the

corresponding charges to equity.

ENVIRONMENTAL COMMITMENTS

Environmental liabilities are accrued based on estimates of known

environmental remediation exposures. The liabilities include

accruals for sites owned by Kodak, sites formerly owned by

Kodak, and other third party sites where Kodak was designated as

a potentially responsible party (PRP). The amounts accrued for

such sites are based on these estimates, which are determined

using the ASTM Standard E 2137-01 “Standard Guide for

Estimating Monetary Costs and Liabilities for Environmental

Matters.” The overall method includes the use of a probabilistic

model that forecasts a range of cost estimates for the

remediation required at individual sites. The Company’s estimate

includes equipment and operating costs for remediation and long-

term monitoring of the sites. Such estimates may be affected by

changing determinations of what constitutes an environmental

liability or an acceptable level of remediation. The Company has

an ongoing monitoring and identification process to assess how

the activities with respect to the known exposures are

progressing against the accrued cost estimates, as well as to

identify other potential remediation sites that are presently

unknown. To the extent that the current work plans are not

effective in achieving targeted results, the proposals to regulatory

agencies for desired methods and outcomes of remediation are

not acceptable, or additional exposures are identified, Kodak’s

estimate of its environmental liabilities may change.