Kodak 2002 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2002 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Financials

59

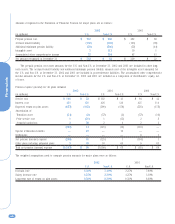

NOTE 11: FINANCIAL INSTRUMENTS

The following table presents the carrying amounts of the assets

(liabilities) and the estimated fair values of financial instruments

at December 31, 2002 and 2001:

(in millions) 2002 2001

Carrying Fair Carrying Fair

Amount Value Amount Value

Marketable securities:

Current $9$9$3$3

Long-term 25 26 34 34

Long-term debt (1,164) (1,225) (1,666) (1,664)

Foreign currency forwards 2211

Silver forwards 2211

Interest rate swap —— (2) (2)

Marketable securities and other investments are valued at

quoted market prices. The fair values of long-term borrowings are

determined by reference to quoted market prices or by obtaining

quotes from dealers. The fair values for the remaining financial

instruments in the above table are based on dealer quotes and

reflect the estimated amounts the Company would pay or receive

to terminate the contracts. The carrying values of cash and cash

equivalents, receivables, short-term borrowings and payables

approximate their fair values.

The Company, as a result of its global operating and

financing activities, is exposed to changes in foreign currency

exchange rates, commodity prices, and interest rates which may

adversely affect its results of operations and financial position.

The Company manages such exposures, in part, with derivative

financial instruments. The fair value of these derivative contracts

is reported in other current assets or accounts payable and other

current liabilities in the accompanying Consolidated Statement of

Financial Position.

Foreign currency forward contracts are used to hedge

existing foreign currency denominated assets and liabilities,

especially those of the Company’s International Treasury Center,

as well as forecasted foreign currency denominated intercompany

sales. Silver forward contracts are used to mitigate the

Company’s risk to fluctuating silver prices. The Company’s

exposure to changes in interest rates results from its investing

and borrowing activities used to meet its liquidity needs. Long-

term debt is generally used to finance long-term investments,

while short-term debt is used to meet working capital

requirements. An interest rate swap agreement was used to

convert $150 million of floating-rate debt to fixed-rate debt. The

Company does not utilize financial instruments for trading or

other speculative purposes.

The Company has entered into foreign currency forward

contracts that are designated as cash flow hedges of exchange

rate risk related to forecasted foreign currency denominated

intercompany sales. At December 31, 2002, the Company had

cash flow hedges for the euro and the Australian dollar, with

maturity dates ranging from January 2003 to August 2003.

At December 31, 2002, the fair value of all open foreign

currency forward contracts hedging foreign currency denominated

intercompany sales was an unrealized loss of $4 million (pre-tax),

recorded in accumulated other comprehensive (loss) income in

the accompanying Consolidated Statement of Shareholders’ Equity.

If this amount were to be realized, all of it would be reclassified

into cost of goods sold during the next twelve months.

Additionally, realized losses of $1 million (pre-tax), related to

closed foreign currency contracts hedging foreign currency

denominated intercompany sales, have been deferred in

accumulated other comprehensive (loss) income. These losses will

be reclassified into cost of goods sold as the inventory transferred

in connection with the intercompany sales is sold to third parties,

all within the next twelve months. During 2002, a pre-tax loss of

$20 million was reclassified from accumulated other

comprehensive (loss) income to cost of goods sold. Hedge

ineffectiveness was insignificant.

The Company does not apply hedge accounting to the foreign

currency forward contracts used to offset currency-related

changes in the fair value of foreign currency denominated assets

and liabilities. These contracts are marked to market through

earnings at the same time that the exposed assets and liabilities

are remeasured through earnings (both in other (charges) income).

The majority of the contracts held by the Company are denominated

in euros, British pounds, Australian dollars, Japanese yen, and

Chinese renminbi. At December 31, 2002, the fair value of these

open contracts was an unrealized gain of $7 million (pre-tax).

The Company has entered into silver forward contracts that

are designated as cash flow hedges of price risk related to

forecasted worldwide silver purchases. The Company used silver

forward contracts to minimize its exposure to increases in silver

prices in 2000, 2001, and 2002. At December 31, 2002, the

Company had open forward contracts with maturity dates ranging

from January 2003 to May 2003.

At December 31, 2002, the fair value of open silver forward

contracts was an unrealized gain of $2 million (pre-tax), recorded

in accumulated other comprehensive (loss) income. If this amount

were to be realized, all of it would be reclassified into cost of

goods sold during the next twelve months. Additionally, realized

losses of less than $1 million (pre-tax), related to closed silver

contracts, have been deferred in accumulated other

comprehensive (loss) income. These gains will be reclassified into

cost of goods sold as silver-containing products are sold, all

within the next twelve months. During 2002, a realized loss of $3

million (pre-tax) was recorded in cost of goods sold. Hedge

ineffectiveness was insignificant.

In July 2001, the Company entered into an interest rate swap

agreement designated as a cash flow hedge of the LIBOR-based

floating-rate interest payments on $150 million of debt issued June

26, 2001 and maturing September 16, 2002. The swap effectively

converted interest expense on that debt to a fixed annual rate of

4.06%. During 2002, $2 million was charged to interest expense

related to the swap. There was no hedge ineffectiveness.