JetBlue Airlines 2011 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2011 JetBlue Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

recorded in other comprehensive income is recognized in aircraft fuel expense. All cash flows related to our fuel

hedging derivatives are classified as operating cash flows.

Our current approach to fuel hedging is to enter into hedges on a discretionary basis without a specific target

of hedge percentage needs in order to mitigate potential liquidity issues and cap fuel prices, when possible.

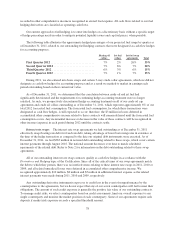

The following table illustrates the approximate hedged percentages of our projected fuel usage by quarter as

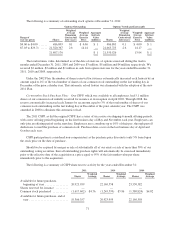

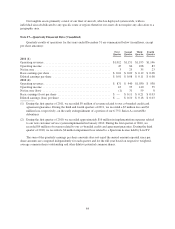

of December 31, 2011, related to our outstanding fuel hedging contracts that were designated as cash flow hedges

for accounting purposes.

Heating oil

collars

Jet fuel

collars

Jet fuel swap

agreements Total

First Quarter 2012 .............................. 7% 2% 26% 35%

Second Quarter 2012 ............................ 7% 6% 7% 20%

Third Quarter 2012 ............................. 6% 3% 6% 15%

Fourth Quarter 2012 ............................ 7% 1% 7% 15%

During 2011, we also entered into basis swaps and certain 3-way crude collar agreements, which we did not

designate as cash flow hedges for accounting purposes and as a result we marked to market in earnings each

period outstanding based on their current fair value.

As of December 31, 2011, we determined that the correlation between crude oil and jet fuel had

significantly deteriorated and the requirements for continuing hedge accounting treatment were no longer

satisfied. As such, we prospectively discontinued hedge accounting treatment on all of our crude oil cap

agreements and crude oil collars outstanding as of December 31, 2011, which represent approximately 6% of our

total 2012 forecasted fuel consumption. The forecasted fuel consumption, for which these transactions were

designated as cash flow hedges, is still expected to occur; therefore, the $3 million in losses deferred in

accumulated other comprehensive income related to these contracts will remain deferred until the forecasted fuel

consumption occurs. Any incremental increase or decrease in the value of these contracts will be recognized in

other income (expense) in each period during 2012 until the contracts settle.

Interest rate swaps: The interest rate swap agreements we had outstanding as of December 31, 2011

effectively swap floating rate debt for fixed rate debt, taking advantage of lower borrowing rates in existence at

the time of the hedge transaction as compared to the date our original debt instruments were executed. As of

December 31, 2011, we had $363 million in notional debt outstanding related to these swaps, which cover certain

interest payments through August 2016. The notional amount decreases over time to match scheduled

repayments of the related debt. Refer to Note 2 for information on the debt outstanding related to these swap

agreements.

All of our outstanding interest rate swap contracts qualify as cash flow hedges in accordance with the

Derivatives and Hedging topic of the Codification. Since all of the critical terms of our swap agreements match

the debt to which they pertain, there was no ineffectiveness relating to these interest rate swaps in 2011, 2010 or

2009, and all related unrealized losses were deferred in accumulated other comprehensive income. We

recognized approximately $10 million, $8 million and $5 million in additional interest expense as the related

interest payments were made during 2011, 2010 and 2009, respectively.

Any outstanding derivative instruments expose us to credit loss in the event of nonperformance by the

counterparties to the agreements, but we do not expect that any of our seven counterparties will fail to meet their

obligations. The amount of such credit exposure is generally the positive fair value of our outstanding contracts.

To manage credit risks, we select counterparties based on credit assessments, limit our overall exposure to any

single counterparty and monitor the market position of each counterparty. Some of our agreements require cash

deposits if market risk exposure exceeds a specified threshold amount.

78