HTC 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

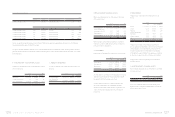

122 2 0 1 0 H T C A N N U A L R E P O R T 123

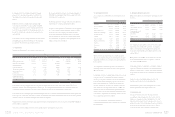

FINANCIAL INFORMATION

would have been determined had no impairment loss been

recognized for the investment in prior years.

Financial Assets Carried at Cost

Investments in equity instruments with no quoted prices in

an active market and with fair values that cannot be reliably

measured, such as non-publicly traded stocks and stocks

traded in the emerging stock market, are measured at their

original cost. The accounting treatment for dividends on

financial assets carried at cost is similar to that for dividends

on available-for-sale financial assets. An impairment loss is

recognized when there is objective evidence that the asset is

impaired. A reversal of this impairment loss is disallowed.

Investments Accounted for by the Equity Method

Investments in which the Company holds 20 percent or more

of the investees’ voting shares or exercises significant influence

over the investees’ operating and financial policy decisions are

accounted for by the equity method.

Prior to January 1, 2006, the dierence between the acquisition

cost and the Company’s proportionate share in the investee’s

equity was amortized by the straight-line method over five

years. Eective January 1, 2006, pursuant to the revised

Statement of Financial Accounting Standard (SFAS) No. 5,

“Long-term Investments Accounted for by Equity Method”, the

acquisition cost is allocated to the assets acquired and liabilities

assumed based on their fair values at the date of acquisition,

and the excess of the acquisition cost over the fair value of

the identifiable net assets acquired is recognized as goodwill.

Goodwill is not being amortized. The excess of the fair value of

the net identifiable assets acquired over the acquisition cost is

used to reduce the fair value of each of the noncurrent assets

acquired (except for financial assets other than investments

accounted for by the equity method, noncurrent assets held

for sale, deferred income tax assets, prepaid pension or other

postretirement benefit) in proportion to the respective fair

values of the noncurrent assets, with any excess recognized

as an extraordinary gain. Eective January 1, 2006, the

accounting treatment for the unamortized investment

premium arising on acquisitions before January 1, 2006 is the

same as that for goodwill and the premium is no longer being

amortized. For any investment discount arising on acquisitions

before January 1, 2006, the unamortized amount continues to

be amortized over the remaining year.

Profits from downstream transactions with an equity-method

investee are eliminated in proportion to the Company’s

percentage of ownership in the investee; however, if the

Company has control over the investee, all the profits are

eliminated. Profits from upstream transactions with an equity-

method investee are eliminated in proportion to the Company’s

percentage of ownership in the investee.

When the Company subscribes for its investee’s newly issued

shares at a percentage dierent from its percentage of

ownership in the investee, the Company records the change

in its equity in the investee’s net assets as an adjustment to

investments, with a corresponding amount credited or charged

to capital surplus. When the adjustment should be debited to

capital surplus, but the capital surplus arising from long-term

investments is insucient, the shortage is debited to retained

earnings.

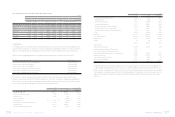

Properties

Properties are stated at cost less accumulated depreciation.

Borrowing costs directly attributable to the acquisition or

construction of properties are capitalized as part of the cost of

those assets. Major additions and improvements to properties

are capitalized, while costs of repairs and maintenance are

expensed currently.

Assets held under capital leases are initially recognized as

assets of the Company at the lower of their fair value at the

inception of the lease or the present value of the minimum

lease payments; the corresponding liability is included in the

balance sheet as obligations under capital leases. The interest

included in lease payments is expensed when paid.

Depreciation is calculated on a straight-line basis over the

estimated service lives of the assets plus one additional year

for salvage value: buildings (including auxiliary equipment) -

3 to 50 years; machinery and equipment - 3 to 5 years; oce

equipment - 3 to 5 years; transportation equipment - 5 years;

and leasehold improvements - 3 years.

Properties still in use beyond their original estimated useful

lives are further depreciated over their newly estimated useful

lives.

The related cost (including revaluation increment) and

accumulated depreciation are derecognized from the balance

sheet upon its disposal. Any gain or loss on disposal of the

asset is included in nonoperating gains or losses in the year of

disposal.

If the properties are leased to others, the related costs and

accumulated depreciation would be transferred from properties

to other assets - assets leased to others.

Intangible Assets

Intangible assets acquired are initially recorded at cost and are

amortized on a straight-line basis over their estimated useful

lives. Patents are amortized on a straight-line basis over 5 to 10

years.

Deferred Charges

Deferred charges are telephone installation charges, computer

software costs and deferred license fees. Installation charges

and computer software are amortized on a straight-line basis

over 3 years, and deferred license fees, over 10 years.

Asset Impairment

If the recoverable amount of an asset is estimated to be less

than its carrying amount, the carrying amount of the asset

is reduced to its recoverable amount. An impairment loss is

charged to earnings unless the asset is carried at a revalued

amount, in which case the impairment loss is treated as a

deduction to the unrealized revaluation increment.

If an impairment loss subsequently reverses, the carrying

amount of the asset is increased accordingly, but the increased

carrying amount may not exceed the carrying amount that

would have been determined had no impairment loss been

recognized for the asset in prior years. A reversal of an

impairment loss is recognized in earnings, unless the asset

is carried at a revalued amount, in which case the reversal of

the impairment loss is treated as an increase in the unrealized

revaluation increment. A reversal of an impairment loss on

goodwill is disallowed.

For long term equity investments for which the Company has

significant influence but with no control, the carrying amount

(including goodwill) of each investment is compared with its

own recoverable amount for the purpose of impairment testing.

Accrued Marketing Expenses

The Company accrues marketing expenses on the basis of

agreements, management’s judgment, and any known factors

that would significantly aect the accruals. In addition,

depending on the nature of relevant events, the accrued

marketing expenses are accounted for as an increase in

marketing expenses or as a decrease in revenues.

Reserve for Warranty Expenses

The Company provides warranty service for one to two years

depending on the contract with customers. The warranty

liability is estimated on the basis of management’s evaluation

of the products under warranty, past warranty experience, and

pertinent factors.

Product-related Costs

The cost of revenues consists of costs of goods sold, write-

downs of inventories and the reversal of write-downs. The

provisions for product warranty are estimated and recorded

under cost of revenues when sales are recognized.

Pension Plan

Pension cost under a defined benefit plan is determined by

actuarial valuations. Contributions made under a defined

contribution plan are recognized as pension cost during the

year in which employees render services.

Curtailment or settlement gains or losses on the defined

benefit plan are recognized as part of the net pension cost for

the year.