HTC 2010 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2010 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

108 2 0 1 0 H T C A N N U A L R E P O R T 109

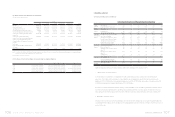

FINANCIAL INFORMATION

3. Profitability Analysis

Consumers are increasingly recognizing the value of HTC’s innovation and the HTC brand. The market success of many flagship

products launched in 2010 helped grow revenues by 90% and net income by 75% to new historic highs. Earnings per share (EPS)

rose to NT$48.49. Operating income and pre-tax income to paid-in capital ratios rose by 517% and 544%, respectively. Return on

equity (ROE) rose to 56% from 37% in 2009.

4. Cash Flow Analysis

Reflecting strong business growth, net cash flows from operating activities grew 48% over 2009 levels to NT$40.8 billion. Current

liabilities also rose 103%, resulting in a 37% reduction in our 2010 cash flow ratio. During 2010 HTC continued expanding production

capacity and oce space to meet anticipated future growth. This, coupled with increased inventory levels necessary to meet

market demand, reduced the cash flow adequacy ratio to 157%. Cash flow reinvestment ratio rose to 26% due to a 179% rise in the

numerator (net cash flows from operating activity – cash dividends) due to a 48% growth in net cash flows from operating activities

and a similar cash dividend payments compared to 2009.

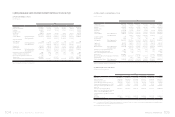

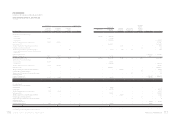

(2) Financial Analysis (Consolidated)

Year

Item (Note 2~3) 2010 2009 2008 2007(Note 1) 2006(Note 1) As of 2011.3.31

Capital

Structure

Analysis

Debt Ratio (%) 61 45 48 39 36 59

Long-term Fund to Fixed Assets

Ratio (%)

533 664 681 1,333 1,347 615

Liquidity

Analysis

Current Ratio (%) 146 195 190 244 264 148

Quick Ratio (%) 120 176 171 217 230 121

Times Interest Earned (Times) 12,624 11,683 3,041 26,595 90,413 6,983

Operating

Performance

Analysis

Average Collection Turnover (Times) 6.14 6.03 6.12 6.06 6.25 6.65

Days Sales Outstanding 59 61 60 60 58 55

Average Inventory Turnover (Times) 10.06 11.46 10.95 9.68 11.34 9.27

Average Payment Turnover (Times) 4.35 4.03 3.92 3.66 4.65 4.49

Average Inventory Turnover Days 36 32 33 38 32 39

Fixed Assets Turnover (Times) 19.88 14.60 17.09 28.01 33.23 28.54

Total Assets Turnover (Times) 1.46 1.21 1.32 1.29 1.59 1.88

Profitability

Analysis

Return on Total Assets (%) 26 21 28 37 47 29

Return on Equity (%) 56 37 49 58 77 72

Operating Income to Paid-in Capital

Ratio (%)

540 312 402 535 590 201

Pre-tax Income to Paid-in Capital

Ratio (%)

550 322 420 562 617 209

Net Margin (%) 14 16 19 24 24 14

Basic Earnings Per Share (NT$) 48.49 27.35 34.44 34.74 30.07 18.36

Cash Flow Cash Flow Ratio (%) 40 52 68 113 104 18

Cash Flow Adequacy Ratio (%) 150 192 211 273 271 153

Cash Flow Reinvestment Ratio (%) 32 11 28 47 43 25

Leverage Operating Leverage 1.43 1.54 1.44 1.20 1.16 1.35

Financial Leverage 1.00 1.00 1.00 1.00 1.00 1.00

Significant changes in various performance indicators reflected the doubling of HTC’s business in 2010.

1. Capital Structure & Liquidity Analyses

As of year-end 2010, our debt ratio stood higher at 61% while current and quick ratios were both lower at 146% and 120%,

respectively. This situation reflected increases in current liabilities due to rapid business growth that saw notes and accounts

payable rise 149% to NT$63.9 billion, accrued marketing expense rise 97% to NT$17.3 billion, accrued bonus to employees rise 75%

to NT$8.5 billion, and product warranty liabilities grow 73% to NT$9.1 billion.

2. Operating Performance Analysis

Fixed asset turnover and total asset turnover were all higher due to strong revenue growth. Days sales outstanding fell to 59 days

in 2010. Average inventory turnover days increased to 36 days due to aggressive increases of inventory to meet strong market

demand and higher inventory amount in transit at 2010 year-end.

3. Profitability Analysis

Consumers are increasingly recognizing the value of HTC’s innovation and the HTC brand. The market success of many flagship

products launched in 2010 helped grow revenues by 93% and net income by 75% to new historic highs. Earnings per share (EPS)

rose to NT$48.49. Operating income and pre-tax income to paid-in capital ratios rose by 540% and 550%, respectively. Return on

total asset (ROA) and Return on equity (ROE) rose to 26% and 56% from 21% and 37% in 2009, respectively.

4. Cash Flow Analysis

Reflecting strong business growth, net cash flows from operating activities grew 66% over 2009 levels to NT$46.0 billion. Current

liabilities also rose 115%, resulting in a 40% reduction in our 2010 cash flow ratio. During 2010 HTC and its subsidiaries continued

expanding production capacity and oce space to meet anticipated future growth. This, coupled with increased inventory levels

necessary to meet market demand, reduced the cash flow adequacy ratio to 150%. Cash flow reinvestment ratio rose to 32% due to

a 241% rise in the numerator (net cash flows from operating activity – cash dividends) due to a 66% growth in net cash flows from

operating activities and a similar cash dividend payments compared to 2009.

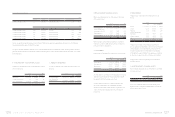

Note 1: Excluded employee bonus expenses

Note 2: In accordance with 2008, 2009 and 2010 financial reporting requirements, write-downs of inventories or reversal of write-downs and product warranty costs registered

during the period 2006 to 2007 have been reclassified as cost of revenues items.

Note 3: Glossary

a. Capital Structure Analysis

(1) Debt Ratio=Total Liabilities / Total Assets.

(2) Long-term Fund to Fixed Assets Ratio=(Shareholders' Equity + Long-term Liabilities) / Net Fixed Assets.

b. Liquidity Analysis

(1) Current Ratio=Current Assets / Current Liabilities.

(2) Quick Ratio:(Current Assets - Inventories - Prepaid Expenses) / Current Liabilities.

(3) Times Interest Earned:Earnings before Interest and Taxes / Interest Expenses.

c. Operating Performance Analysis

(1) Average Collection Turnover: Net Sales / Average Trade Receivables.

(2) Days Sales Outstanding: 365 / Average Collection Turnover.

(3) Average Inventory Turnover:Cost of Sales / Average Inventory.

(4) Average Payment Turnover=Cost of Sales / Average Trade Payables.