HTC 2010 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2010 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

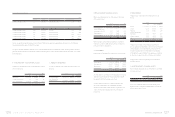

120 2 0 1 0 H T C A N N U A L R E P O R T 121

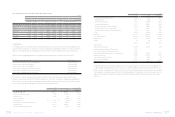

FINANCIAL INFORMATION

HTC CORPORATION

NOTES TO FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2009 AND 2010

(In Thousands, Unless Stated Otherwise)

1. ORGANIZATION AND OPERATIONS

HTC Corporation (the “Company”) was incorporated on May

15, 1997 under the Company Law of the Republic of China to

design, manufacture and sell smart handheld devices. In 1998,

the Company had an initial public oering and, in March 2002,

the Company’s stock was listed on the Taiwan Stock Exchange.

On November 19, 2003, the Company started trading Global

Depositary Receipts on the Luxembourg Stock Exchange.

The Company had 7,284 and 10,843 employees as of December

31, 2009 and 2010, respectively.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The financial statements have been prepared in conformity

with the Guidelines Governing the Preparation of Financial

Reports by Securities Issuers, Business Accounting Law,

Guidelines Governing Business Accounting, and accounting

principles generally accepted in the Republic of China (ROC).

Under these guidelines, laws and principles, certain estimates

and assumptions have been used for the allowance for doubtful

accounts, allowance for loss on inventories, depreciation of

properties, income tax, royalty, pension cost, allowance for

product warranties, bonuses to employees, etc. Actual results

may dier from these estimates.

For readers’ convenience, the accompanying financial

statements have been translated into English from the

original Chinese version prepared and used in the ROC. If

inconsistencies arise between the English version and the

Chinese version or if dierences arise in the interpretations

between the two versions, the Chinese version of the financial

statements shall prevail. However, the accompanying financial

statements do not include the English translation of the

additional footnote disclosures that are not required under

ROC generally accepted accounting principles but are required

by the Securities and Futures Bureau for their oversight

purposes.

The Company’s significant accounting policies are summarized

as follows:

Current/Noncurrent Assets and Liabilities

Current assets include cash, cash equivalents, and those assets

held primarily for trading purposes or to be realized, sold or

consumed within one year from the balance sheet date. All

other assets such as properties and intangible assets are

classified as noncurrent. Current liabilities are obligations

incurred for trading purposes or to be settled within one year

from the balance sheet date. All other liabilities are classified

as noncurrent.

Financial Assets/Liabilities at Fair Value through Profit or Loss

Financial instruments classified as financial assets or financial

liabilities at fair value through profit or loss (“FVTPL”) include

financial assets or financial liabilities held for trading and

those designated as at FVTPL on initial recognition. The

Company recognizes a financial asset or a financial liability on

its balance sheet when the Company becomes a party to the

contractual provisions of the financial instrument. A financial

asset is derecognized when the Company has lost control of its

contractual rights over the financial asset. A financial liability

is derecognized when the obligation specified in the relevant

contract is discharged, cancelled or expired.

Financial instruments at FVTPL are initially measured at fair

value plus transaction costs that are directly attributable to the

acquisition. At each balance sheet date subsequent to initial

recognition, financial assets or financial liabilities at FVTPL are

remeasured at fair value, with changes in fair value recognized

directly in profit or loss in the year in which they arise. Cash

dividends received subsequently (including those received in

the year of investment) are recognized as income for the year.

On derecognition of a financial asset or a financial liability, the

dierence between its carrying amount and the sum of the

consideration received and receivable or consideration paid

and payable is recognized in profit or loss.

A derivative that does not meet the criteria for hedge

accounting is classified as a financial asset or a financial liability

held for trading. If the fair value of the derivative is positive,

the derivative is recognized as a financial asset; otherwise, the

derivative is recognized as a financial liability.

Fair values of financial assets and financial liabilities at the

balance sheet date are determined as follows: Publicly traded

stocks - at closing prices; open-end mutual funds - at net asset

values; bonds - at prices quoted by the Taiwan GreTai Securities

Market; and financial assets and financial liabilities without

quoted prices in an active market - at values determined using

valuation techniques.

Available-for-sale Financial Assets

Available-for-sale financial assets are initially measured at fair

value plus transaction costs that are directly attributable to the

acquisition. At each balance sheet date subsequent to initial

recognition, available-for-sale financial assets are remeasured

at fair value, with changes in fair value recognized in equity

until the financial assets are disposed of, at which time, the

cumulative gain or loss previously recognized in equity is

included in profit or loss for the year.

The recognition, derecognition and the fair value bases of

available-for-sale financial assets are similar with those of

financial assets at FVTPL.

Cash dividends are recognized on the stockholders’ resolutions,

except for dividends distributed from the pre-acquisition

profit, which are treated as a reduction of investment cost.

Stock dividends are not recognized as investment income

but are recorded as an increase in the number of shares. The

total number of shares subsequent to the increase is used for

recalculation of cost per share.

An impairment loss is recognized when there is objective

evidence that the financial asset is impaired. Any subsequent

decrease in impairment loss for an equity instrument classified

as available-for-sale is recognized directly in equity.

Revenue Recognition, Accounts Receivable and Allowance for

Doubtful Accounts

Revenue from sales of goods is recognized when the Company

has transferred to the buyer the significant risks and rewards

of ownership of the goods because the earnings process has

been completed and the economic benefits associated with

the transaction have been realized or are realizable.

Revenue is measured at the fair value of the consideration

received or receivable and represents amounts agreed

between the Company and the customers for goods sold in the

normal course of business, net of sales discounts and volume

rebates. For trade receivables due within one year from the

balance sheet date, as the nominal value of the consideration

to be received approximates its fair value and transactions are

frequent, fair value of the consideration is not determined by

discounting all future receipts using an imputed rate of interest.

An allowance for doubtful accounts is provided on the basis

of a review of the collectability of accounts receivable. The

Company assesses the probability of collections of accounts

receivable by examining the aging analysis of the outstanding

receivables and assessing the value of the collateral provided

by customers.

Inventories

Inventories consist of raw materials, supplies, finished

goods and work-in-process. Eective from January 1, 2008,

inventories are stated at the lower of cost or net realizable

value. Inventory write-downs are made item by item, except

where it may be appropriate to group similar or related items.

Net realizable value is the estimated selling price of inventories

less all estimated costs of completion and costs necessary to

make the sale. Cost is determined using the moving-average

method.

Held-to-maturity Financial Assets

Held-to-maturity financial assets are carried at amortized cost

using the eective interest method. Held-to-maturity financial

assets are initially measured at fair value plus transaction costs

that are directly attributable to the acquisition. Profit or loss

is recognized when the financial assets are derecognized,

impaired, or amortized. All regular way purchases or sales of

financial assets are accounted for using a trade date basis.

An impairment loss is recognized when there is objective

evidence that the investment is impaired. The impairment

loss is reversed if an increase in the investment’s recoverable

amount is due to an event which occurred after the impairment

loss was recognized; however, the adjusted carrying amount

of the investment may not exceed the carrying amount that