Google 2008 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2008 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

Google Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

experience, must consider assumptions that market participants would use about renewal or extension as adjusted

for SFAS 142’s entity-specific factors. FSP 142-3 is effective for us beginning January 1, 2009. We do not expect

the impact of the adoption of FSP 142-3 to be material.

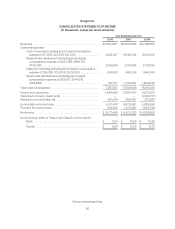

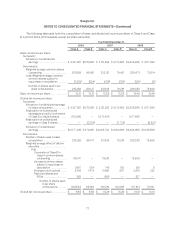

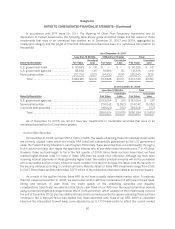

Note 2. Net Income Per Share of Class A and Class B Common Stock

We compute net income per share of Class A and Class B common stock in accordance with SFAS No. 128,

Earnings per Share (SFAS 128) using the two-class method. Under the provisions of SFAS 128, basic net income

per share is computed using the weighted average number of common shares outstanding during the period

except that it does not include unvested common shares subject to repurchase or cancellation. Diluted net income

per share is computed using the weighted average number of common shares and, if dilutive, potential common

shares outstanding during the period. Potential common shares consist of the incremental common shares

issuable upon the exercise of stock options, warrants, restricted shares, restricted stock units and unvested

common shares subject to repurchase or cancellation. The dilutive effect of outstanding stock options, restricted

shares, restricted stock units and warrants is reflected in diluted earnings per share by application of the treasury

stock method. The computation of the diluted net income per share of Class A common stock assumes the

conversion of Class B common stock, while the diluted net income per share of Class B common stock does not

assume the conversion of those shares.

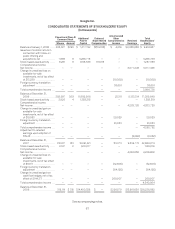

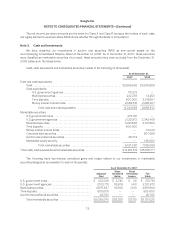

The rights, including the liquidation and dividend rights, of the holders of our Class A and Class B common

stock are identical, except with respect to voting. Further, there are a number of safeguards built into our

Certificate of Incorporation, as well as Delaware law, which preclude our board of directors from declaring or

paying unequal per share dividends on our Class A and Class B common stock. Specifically, Delaware law provides

that amendments to our Certificate of Incorporation which would have the affect of adversely altering the rights,

powers or preferences of a given class of stock (in this case the right of our Class A common stock to receive an

equal dividend to any declared on our Class B common stock) must be approved by the class of stock adversely

affected by the proposed amendment. In addition, our Certificate of Incorporation provides that before any such

amendment may be put to a stockholder vote, it must be approved by the unanimous consent of our Board of

Directors. As a result, and in accordance with EITF Issue No. 03-6, Participating Securities and the Two-Class

Method under FASB Statement No. 128, the undistributed earnings for each year are allocated based on the

contractual participation rights of the Class A and Class B common shares as if the earnings for the year had been

distributed. As the liquidation and dividend rights are identical, the undistributed earnings are allocated on a

proportionate basis. Further, as we assume the conversion of Class B common stock in the computation of the

diluted net income per share of Class A common stock, the undistributed earnings are equal to net income for that

computation.

76