GNC 2010 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2010 GNC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

Table of Contents

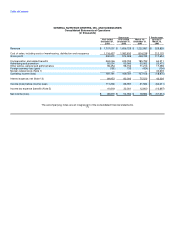

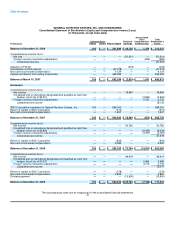

Income Taxes

We are required to estimate income taxes in each of the jurisdictions in which we operate. This process involves estimating the actual

current tax liability together with assessing temporary differences in recognition of income (loss) for tax and accounting purposes. These

differences result in deferred tax assets and liabilities, which are included in our consolidated balance sheet. We then assess the likelihood that

the deferred tax assets will be recovered from future taxable income and, to the extent we believe that recovery is not likely, we establish a

valuation allowance against the deferred tax asset. Further, we operate within multiple taxing jurisdictions and are subject to audit in these

jurisdictions. These audits can involve complex issues which may require an extended period of time to resolve and could result in additional

assessments of income tax. We believe adequate provisions for income taxes have been made for all periods.

We adopted the update to the standard on income taxes at the beginning of fiscal 2007. As a result of the adoption of this standard, we

recognize liabilities for uncertain tax positions based on the two-step process prescribed by the interpretation. The first step requires us to

determine if the weight of available evidence indicates that the tax position has met the threshold for recognition; therefore, we must evaluate

whether it is more likely than not that the position will be sustained on audit, including resolution of any related appeals or litigation processes.

The second step requires us to measure the tax benefit of the tax position taken, or expected to be taken, in an income tax return as the largest

amount that is more than 50% likely of being realized upon ultimate settlement. This measurement step is inherently difficult and requires

subjective estimations of such amounts to determine the probability of various possible outcomes. We reevaluate the uncertain tax positions

each quarter based on factors including, but not limited to, changes in facts or circumstances, changes in tax law, effectively settled issues

under audit, and new audit activity. Such a change in recognition or measurement would result in the recognition of a tax benefit or an

additional charge to the tax provision in the period.

Although we believe the measurement of our liabilities for uncertain tax positions is reasonable, no assurance can be given that the final

outcome of these matters will not be different than what is reflected in the historical income tax provisions and accruals. If additional taxes are

assessed as a result of an audit or litigation, it could have a material effect on our income tax provision and net income in the period or periods

for which that determination is made.

Recently Issued Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board (the "FASB") issued a standard on Generally Accepted Accounting Principles. This

standard establishes the FASB Accounting Standards Codification (the "Codification") as the single source of authoritative nongovernmental

accounting principles generally accepted in the United States of America ("U.S. GAAP"). The Codification is effective for interim and annual

periods ending after September 15, 2009. The adoption of this standard did not have any impact on our financial statements.

In June 2009, the SEC issued a staff accounting bulletin ("SAB") that revises or rescinds portions of the interpretive guidance included in the

codification of SABs in order to make the interpretive guidance consistent with U.S. GAAP. The principal revisions include deletion of material

no longer necessary or that has been superseded because of the issuance of new standards. We adopted this SAB during the second quarter

of 2009; the adoption did not have any impact on our consolidated financial statements.

Fair Value

In September 2006, the FASB issued new standards on fair value measurements and disclosures. These new standards define fair value,

establish a framework for measuring fair value in accordance with U.S. GAAP, and expand disclosures about fair value measurements. The

new standard applies under other accounting pronouncements that require or permit fair value measurements and, accordingly, does not

require any new fair value measurements. The original standard was initially

62