Express Scripts 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 Express Scripts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

Express Scripts 2012 Annual Report76

75

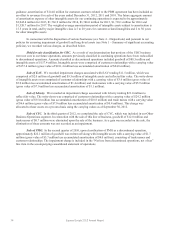

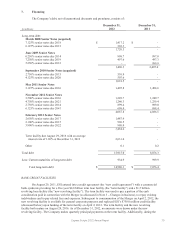

fourth quarter of 2012, the Company paid down $1,000.0 million of the term facility. As of December 31, 2012,

$2,631.6 million was outstanding under the term facility with an average interest rate of 1.96%, of which $631.6

million is considered current maturities of long-term debt. Upon consummation of the Merger, Express Scripts

assumed the obligations of ESI and became the borrower under the new credit agreement.

The new credit agreement requires interest to be paid at the LIBOR or adjusted base rate options, plus a

margin. The margin over LIBOR ranges from 1.25% to 1.75% for the term facility and 1.10% to 1.55% for the new

revolving facility, and the margin over the base rate options ranges from 0.25% to 0.75% for the term facility and

0.10% to 0.55% for the new revolving facility, depending on our consolidated leverage ratio. Under the new credit

agreement, we are required to pay commitment fees on the unused portion of the $1.5 billion new revolving facility.

The commitment fee ranges from 0.15% to 0.20% depending on Express Scripts’ consolidated leverage ratio.

On August 13, 2010, ESI entered into a credit agreement with a commercial bank syndicate providing for a

three-year revolving credit facility of $750.0 million (the “2010 credit facility”). The 2010 credit facility was

terminated and replaced by the new revolving facility on April 2, 2012, as described above.

BRIDGE FACILITY

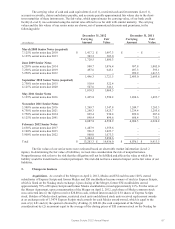

On August 5, 2011, ESI entered into a credit agreement with Credit Suisse AG, Cayman Islands Branch, as

administrative agent, Citibank, N.A., as syndication agent, and the other lenders and agents named within the

agreement. The credit agreement provided for a one-year unsecured $14.0 billion bridge term loan facility (the

“bridge facility”) to be used to pay a portion of the cash consideration in connection with the Merger in the event

that more favorable financing arrangements could not be secured. No amounts were withdrawn under the bridge

facility, and subsequent to consummation of the Merger on April 2, 2012, the bridge facility was terminated.

FIVE-YEAR CREDIT FACILITY

On April 30, 2007, Medco entered into a senior unsecured credit agreement, which was available for

general working capital requirements. The facility consisted of a $1.0 billion, 5-year senior unsecured term loan and

a $2.0 billion, 5-year senior unsecured revolving credit facility. The facility was due to mature on April 30, 2012.

Medco refinanced the $2.0 billion senior unsecured revolving credit facility on January 23, 2012. Upon completion

of the Merger, the $1.0 billion senior unsecured term loan and all associated interest, and the $1.0 billion then

outstanding under the senior unsecured revolving credit facility, were repaid in full and terminated.

ACCOUNTS RECEIVABLE FINANCING FACILITY

Upon consummation of the Merger, Express Scripts assumed a $600 million, 364-day renewable accounts

receivable financing facility that was collateralized by Medco’s pharmaceutical manufacturer rebates accounts

receivable. On September 21, 2012, Express Scripts terminated the facility and repaid all amounts drawn down.

INTEREST RATE SWAP

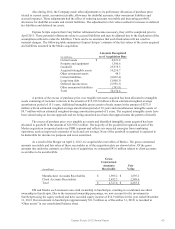

Medco entered into five interest rate swap agreements in 2004. These swap agreements, in effect, converted

$200 million of Medco’s $500 million of 7.250% senior notes due 2013 to variable interest rate debt. Under the

terms of these swap agreements, Medco received a fixed rate of interest of 7.25% on $200 million and paid variable

interest rates based on the six-month LIBOR plus a weighted-average spread of 3.05%. The payment dates under the

agreements coincided with the interest payment dates on the hedged debt instruments and the difference between the

amounts paid and received was included in interest expense. These swaps were settled on May 7, 2012. Express

Scripts received $10.1 million for settlement of the swaps and the associated accrued interest receivable through

May 7, 2012, and recorded a loss of $1.5 million related to the carrying amount of the swaps and bank fees.

SENIOR NOTES

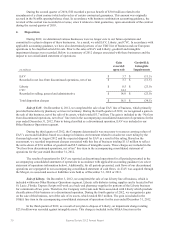

Following the consummation of the Merger on April 2, 2012, several series of senior notes issued by

Medco are reported as debt obligations of Express Scripts on a consolidated basis.

In August 2003, Medco issued $500.0 million aggregate principal amount of 7.250% senior notes due 2013

(the “August 2003 Senior Notes”). On May 7, 2012, the Company redeemed the August 2003 Senior Notes. These

notes were redeemable at a redemption price equal to the greater of (i) 100% of the principal amount of the notes

being redeemed, or (ii) the sum of the present values of 107.25% of the principal amount of these notes being