Energizer 2011 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2011 Energizer annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

ENERGIZER HOLDINGS, INC.

(Dollars in millions, except per share and percentage data)

under our credit facilities will be adequate to meet liquidity requirements prior to the maturity of the Company's term loan in

December 2012, although no guarantee can be given in this regard. We anticipate that the term loan, which matures in

December 2012 will be refinanced in some manner, but we can provide no assurances as to the type, nature and cost of this

refinancing.

The counterparties to long-term committed borrowings consist of a number of major financial institutions. The Company

continually monitors positions with, and credit ratings of, counterparties both internally and by using outside ratings agencies.

In fiscal 2011, the Company repurchased 3.7 million shares of Energizer common stock, exclusive of a small number of shares

related to the net settlement of certain stock awards for tax withholding purposes, for a total cost of approximately $276. Since

the end of fiscal 2011 and through November 20, the Company repurchased an additional 0.8 million shares of its common

stock at a total cost of approximately $56. All of the shares were purchased in the open market under the Company's current

authorization from its Board of Directors. The Company has approximately 3.4 million shares remaining on this current

authorization to repurchase its common stock in the future. Future purchases may be made from time to time on the open

market or through privately negotiated transactions, subject to corporate objectives and the discretion of management.

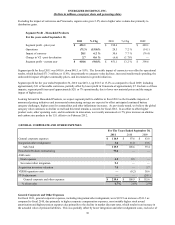

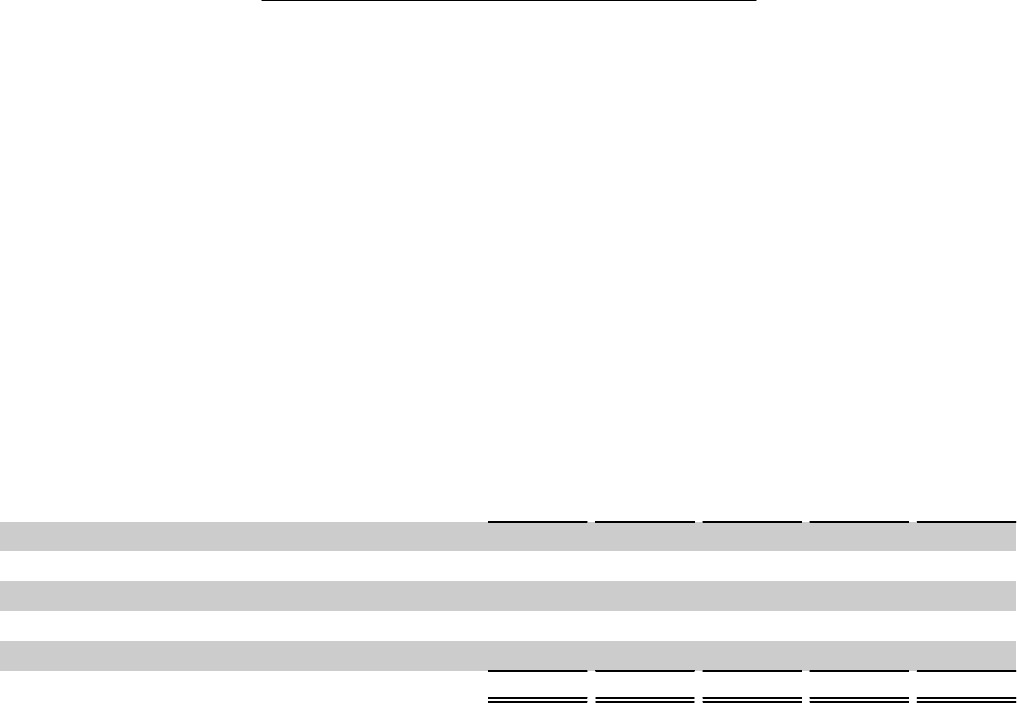

A summary of the Company’s contractual obligations at September 30, 2011 is shown below:

Long-term debt, including current maturities

Interest on long-term debt

Minimum pension funding(1)

Operating leases

Purchase obligations and other(2)

Total

Total

$ 2,312.5

625.6

334.3

121.1

52.3

$ 3,445.8

Less than

1 year

$ 106.0

106.6

65.7

27.8

18.3

$ 324.4

1-3 years

$ 706.5

191.8

140.1

38.1

33.4

$ 1,109.9

3-5 years

$ 440.0

150.9

128.5

24.4

0.6

$ 744.4

More than

5 years

$ 1,060.0

176.3

—

30.8

—

$ 1,267.1

1Globally, total pension contributions for the Company in fiscal 2012 are estimated to be approximately $65.7. The U.S. pension plans constitute 80% of

the total benefit obligations and plan assets for the Company’s pension plans. The estimates beyond 2012 represent future pension payments to comply

with local funding requirements in the U.S. only. The projected payments beyond fiscal year 2016 are not currently determinable.

2The Company has estimated approximately $3.7 of cash settlements associated with unrecognized tax benefits within the next year, which are included

in the table above. As of September 30, 2011, the Company’s Consolidated Balance Sheet reflects a liability for unrecognized tax benefits of $41.2,

excluding $10.4 of interest and penalties. The contractual obligations table above does not include this liability beyond one year. Due to the high degree

of uncertainty regarding the timing of future cash outflows of liabilities for unrecognized tax benefits beyond one year, a reasonable estimate of the

period of cash settlement for periods beyond the next twelve months cannot be made, and thus is not included in this table.

Purchase obligations set forth in the table above represent contractual obligations that generally have longer terms, and are non-

routine in nature. The Company also has contractual purchase obligations for future purchases, which generally extend one to

three months. These obligations are primarily individual, short-term purchase orders for the purchase of routine goods and

services at fair value that are part of normal operations and are reflected in historical operating cash flow trends. In addition, the

Company has various commitments related to service and supply contracts that contain penalty provisions for early

termination. As of September 30, 2011, we do not believe such purchase obligations or termination penalties will have a

significant effect on our results of operations, financial position or liquidity position in the future. As such, these obligations

have been excluded from the table above.

Market Risk Sensitive Instruments and Positions

The market risk inherent in the Company’s financial instruments and positions represents the potential loss arising from adverse

changes in currency rates, commodity prices, interest rates and the Company’s stock price. The following risk management

discussion and the estimated amounts generated from the sensitivity analysis are forward-looking statements of market risk

assuming certain adverse market conditions occur. Company policy allows derivatives to be used only for identifiable

exposures and, therefore, the Company does not enter into hedges for trading purposes where the sole objective is to generate

profits.

Currency Rate Exposure

A significant portion of our product cost is more closely tied to the U.S. dollar and, to a lesser extent, the Euro, than to the local

currencies in which the product is sold. As such, a weakening of currencies relative to the U.S. dollar and, to a lesser extent, the

Euro, results in margin declines unless mitigated through pricing actions, which are not always available due to the competitive

39