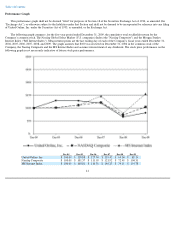

Classmates.com 2009 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2009 Classmates.com annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

Table of Contents

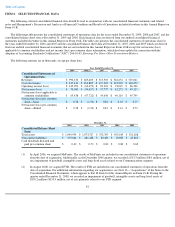

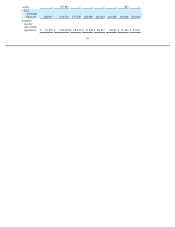

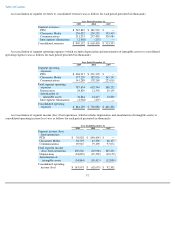

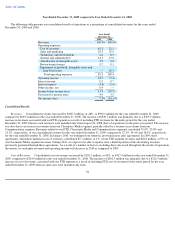

The determination of whether or not goodwill is impaired involves a significant level of judgment in the assumptions underlying the

approaches used to determine the estimated fair value of our reporting units. Our analysis included sufficient tolerance for sensitivity in key

assumptions. The determination of the fair value of our reporting units included a study of market comparables, including the selection of

appropriate valuation multiples and discounted cash flow models based on our internal forecasts and projections.

The estimated fair values for all of our reporting units were determined using a combination of the income approach and the market

approach. Under the income approach, a reporting unit's fair value is estimated based on the discounted cash flow method. The discounted cash

flow method is dependent upon a number of factors, including projections of the amounts and timing of future revenues and cash flows, assumed

discount rates and other assumptions. Under the market approach, using the guideline company method, a reporting unit's fair value is estimated

based on multiples of the cash-free market value of invested capital to revenue and adjusted EBITDA of the guideline companies. Adjusted

EBITDA amounts excluded stock-based compensation expense for the reporting units and guideline companies. The revenue and adjusted

EBITDA multiples of our reporting units were selected based on a comparison of each reporting unit's operating performance and margins,

among other factors, to those of the guideline companies.

Based on our impairment testing in the fourth quarter of 2009, an increase or decrease of 100 basis points in the discount rate or the

terminal growth rate for each of our reporting units would not have resulted in any goodwill impairment. A 100 basis point decrease in the

terminal growth rate for FTD would result in an indicated fair value that was higher than the carrying value of equity by $12.6 million. We

believe the assumptions and rates used in our impairment assessment are reasonable, but they are judgmental, and variations in any assumptions

could result in a materially different calculation of the impairment amount, if any.

Intangible Assets and Other Long

-Lived Assets

We account for identifiable intangible assets and other long-lived assets in accordance with ASC 360, Property, Plant and Equipment ,

which addresses financial accounting and reporting for the impairment and disposition of identifiable intangible assets and other long-lived

assets. Intangible assets acquired in a business combination are initially recorded at management's estimate of their fair values. We evaluate the

recoverability of identifiable intangible assets and other long-lived assets for impairment when events occur or circumstances change that would

indicate that the carrying amount of an asset may not be recoverable. Events or circumstances that may indicate that an asset is impaired include,

but are not limited to, significant decreases in the market value of an asset, significant underperformance relative to expected historical or

projected future operating results, a change in the extent or manner in which an asset is used, shifts in technology, loss of key management or

other personnel, significant negative industry or economic trends, changes in our operating model or strategy, and competitive forces. In

determining if an impairment exists, we estimate the undiscounted cash flows to be generated from the use and ultimate disposition of these

assets. If an impairment is indicated based on a comparison of the assets' carrying values and the undiscounted cash flows, the impairment loss is

measured as the amount by which the carrying amount of the assets exceeds the fair market value of the assets. Definite-lived intangible assets

are amortized on either a straight-line basis or an accelerated basis over their estimated useful lives, ranging from two to ten years. Our

identifiable intangible assets were acquired primarily in connection with business combinations. We did not record any impairment charges

related to our intangible assets in the year ended December 31, 2009.

The process of evaluating the potential impairment of long-

lived intangible assets is subjective and requires significant judgment on matters

such as, but not limited to, the asset group to be tested for recoverability. We are also required to make estimates that may significantly impact

the outcome of the

50