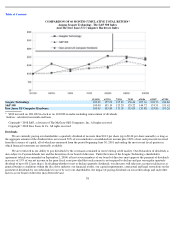

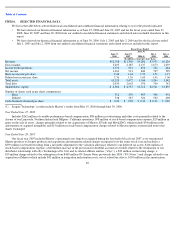

Seagate 2007 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2007 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

Table of Contents

addition, corporate demand is typically higher during the second half of the calendar year when IT budget calendars provide for more spending.

We expect the disc drive industry to experience normal seasonal patterns of increased demand for the September 2008 quarter.

Recording Heads and Media

Due to industry consolidation there are limited number of independent suppliers of recording heads and media available to disc drive

manufacturers. As a result, vertically integrated disc drive manufacturers, who manufacture their own recording heads and media, are less

dependent on external supply of recording heads and media than less vertically integrated disc drive manufacturers. While we believe that there

is adequate supply to meet currently identified industry demand, these consolidations may limit the supply of recording heads and media from

independent suppliers in the long-term.

Commodity and Other Manufacturing Costs

The production of disc drives requires precious metals, scarce alloys and industrial commodities, that are subject to fluctuations in prices,

and the supply of which has at times been constrained. Recent increases in the price of many commodities have resulted in higher costs of

materials used in the manufacture of disc drive products. Additionally, adverse economic conditions such as rising fuel costs may further

increase commodity, manufacturing and freight costs. Should the disc drive industry not be able to pass these costs onto customers, gross

margins may be impacted.

Industry Supply Balance

Historically, the industry has from time to time experienced periods of imbalances between supply and demand. To the extent that the disc

drive industry builds capacity and products based on expectations of demand that do not materialize, there may be an oversupply of products that

could lead to increased price erosion. Conversely, during periods where demand exceeds supply, price erosion is generally more benign. The

industry, excluding Seagate, exited the June 2008 quarter with what we believe to be approximately five weeks of distribution inventory in the

desktop channel, which is consistent with historical seasonal patterns.

Seagate Overview

We are the world

’

s leading provider of hard disc drives, based on revenue and units shipped. Our products address the enterprise, desktop,

mobile computing and CE and branded solutions storage markets. The Seagate 3.5-inch and 2.5-

inch disc drive units used in our branded storage

products are reported in the desktop and mobile market information, respectively. We maintain a highly integrated approach to our business by

designing and manufacturing a significant portion of the components we view as critical to our products, such as read/write heads and recording

media. We believe that our control of these key technologies, combined with our platform design and manufacturing, will enable us to achieve

product performance, time-to-market leadership and manufacturing flexibility, which will allow us to respond to customers and market

opportunities. Our technology ownership, combined with our integrated design and manufacturing approach, has allowed us to effectively

leverage our leadership in traditional computing to enter new markets with only incremental product development and manufacturing costs.

Maxtor Acquisition

During fiscal year 2007, we completed our integration of Maxtor, including customer and product transitions where we replaced Maxtor

designed disc drive products with Seagate designed disc drive products. Our fiscal year 2007 included Maxtor’s operating losses largely

recognized during the first half of fiscal year 2007 as we transitioned Maxtor products to Seagate products and acquisition and integration related

charges recognized over the entire fiscal year. We expect to continue to incur charges, the most significant of which are expected to be the

amortization of acquired intangible assets.

46