Seagate 2007 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2007 Seagate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

|

|

Table of Contents

SEAGATE TECHNOLOGY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

—

(

Continued)

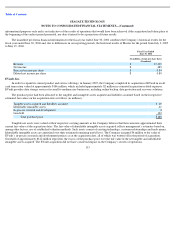

The fair value of customer relationships was determined using the Excess Earnings Method under the Income Approach based on the

estimated revenues to be derived from Maxtor’s OEM, distribution and retail customers. This approach reflects the present value of projected

cash flows that a market participant would expect to generate from these customer relationships less charges related to the contribution of other

assets to those cash flows. The fair values of the customer relationships are being amortized to Operating Expenses on a straight-line basis over

the estimated lives of three to four years.

Trade names reflect the value associated with Maxtor’s brand names. Trade names were valued using the Relief-from-Royalty Method, a

form of the Income Approach, which estimates the royalty cost avoided by owning the trade names as opposed to having to license them from an

independent third party. The resulting cash flow savings estimated over the remaining useful life of the trade names are then discounted to

present value to arrive at the fair value allocated to this intangible. Trade names are being amortized to Operating Expenses over the estimated

useful life of four years.

In-Process Research and Development

As of the date of the acquisition, all future development activities at Maxtor were discontinued. Therefore there were no assets that

qualified as in-process research and development.

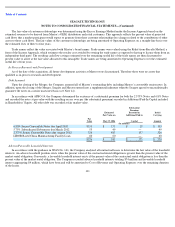

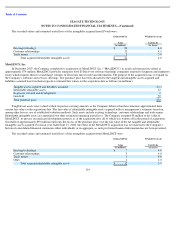

Debt Assumed

Upon the closing of the Merger, the Company assumed all of Maxtor’s outstanding debt, including Maxtor’s convertible senior notes. In

addition, upon the closing of the Merger, Seagate and Maxtor entered into a supplemental indenture whereby Seagate agreed to unconditionally

guarantee the notes on a senior unsecured basis (see Note 14).

In accordance with APBO 14, the Company determined the existence of a substantial premium for both the 2.375% Notes and 6.8% Notes

and recorded the notes at par value with the resulting excess over par (the substantial premium) recorded in Additional Paid-In Capital included

in Shareholders’ Equity. All other debt was recorded at fair market value.

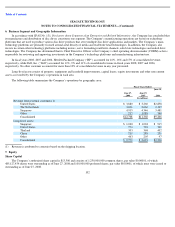

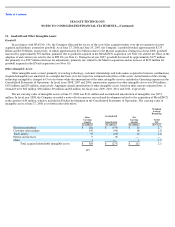

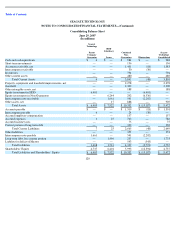

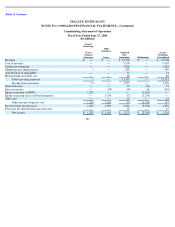

Adverse/Favorable Leasehold Interests

Par

Value

Estimated

Fair Value on

May 19, 2006

Substantial

Premium

Recorded in

Additional Paid in

Capital

Initial

Carrying

Amount

(In millions)

6.80% Senior Convertible Notes due April 2010

$

135

$

153

$

18

$

135

5.75% Subordinated Debentures due March 2012

55

49

—

49

2.375% Senior Convertible Notes due August 2012

326

483

157

326

LIBOR Based China Manufacturing Facility Loan

60

60

—

60

$

576

$

745

$

175

$

570

In accordance with the guidance in SFAS No. 141, the Company analyzed all contractual leases to determine the fair value of the leasehold

interests. An adverse leasehold position exists when the present value of the contractual rental obligation is greater than the present value of the

market rental obligation. Conversely, a favorable leasehold interest exists if the present value of the contractual rental obligation is less than the

present value of the market rental obligation. The Company recorded adverse leasehold interests totaling $74 million and favorable leasehold

interest aggregating $4 million, which have been and will be amortized to Cost of Revenue and Operating Expenses over the remaining duration

of the leases.

111