Food Lion 2014 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2014 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

90 // DELHAIZE GROUP FINANCIAL STATEMENTS 2014

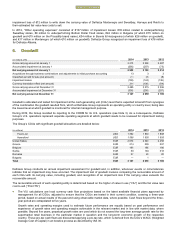

2.5 Standards and Interpretations Issued but not yet Effective

The following standards, amendments to or revisions of existing standards or interpretations have been published and are

mandatory applicable for the Group’s accounting periods beginning on January 1, 2015, or later. Unless otherwise indicated

below, Delhaize Group is still in the process of assessing the impact of these new standards, interpretations, or amendments to

its consolidated financial statements and does not plan to early adopt them:

Improvements to IFRS 2010 – 2012 and 2011 – 2013 Cycles (applicable for annual periods beginning after January 1, 2015

except for the Amendments to IFRS 13, as disclosed in Note 2.2): Late 2013, the IASB issued the final omnibus annual

improvements standard for the 2010 – 2012 Cycle containing eight changes to seven IASB pronouncements and the 2011 –

2013 Cycle containing four changes to four IASB pronouncements. On September 25, 2014 the IASB issued the

Improvements to IFRS 2012 – 2014 Cycle (applicable for annual periods beginning after January 1, 2016) containing five

changes to four IASB pronouncements. The Group is still in process in analyzing these amendments, but does not believe

that any of these amendments will have a significant impact on its consolidated financial statements as most of the Group’s

accounting policies were already in line with the clarifications included in these improvements.

Amendments to IAS 19 Defined Benefit Plans: Employee Contributions (applicable for annual periods beginning after

January 1, 2015): The amendments were issued in late 2013 and clarify how an entity should account for contributions made

by employees or third parties to defined benefit plans, based on whether those contributions are dependent on the number

of years of service provided by the employee.

For contributions that are independent of the number of years of service, the entity may either recognize the contributions as

a reduction in the service cost in the period in which the related service is rendered, or attribute them to the employees’

periods of service using the projected unit credit method. For contributions that are dependent on the number of years of

service, the entity should attribute the contributions to the employees’ periods of service. The Group expects that the new

guidance will have little or no impact on its consolidated financial statements.

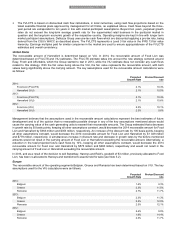

Amendments to IAS 16 and IAS 38 Clarification of Acceptable Methods of Depreciation and Amortisation (applicable for

annual periods beginning after January 1, 2016): In 2014, the IASB issued amendments to IAS 16 and IAS 38. The new IAS

16 pronouncements prohibit entities from using revenue-based depreciation method for items of property, plant and

equipment while the amendments to IAS 38 introduce a presumption that revenue is not an appropriate basis for

amortization of an intangible asset, which is rebuttable only in two limited circumstances. The amendments will have no

impact on the Group.

Amendments to IFRS 11 Accounting for Acquisitions of Interest in Joint Operations (applicable for annual periods beginning

after January 1, 2016): The amendments to IFRS 11 provide guidance on how to account for the acquisition of a joint

operation that constitutes a business as defined by IFRS 3 Business Combinations. Specifically, the amendments state that

the relevant principles on accounting for business combinations should be applied. The same requirements should be

applied to the formation of a joint operation if and only if an existing business is contributed to the joint operation by one of

the parties that participate in the joint operation. The amendment has so far no impact on the consolidated financial

statements of the Group.

Amendments to IFRS 10 and IAS 28 Sale or Contribution of Assets between an Investor and its Associate or Joint Venture

(applicable for annual periods beginning after January 1, 2016): During 2014, the IASB issued the amendments which

address a conflict between the requirements of IAS 28 and IFRS 10 by clarifying that in a transaction involving an associate

or joint venture the extent of gain or loss recognition depends on whether the assets sold or contributed constitute a

business. The amendment has so far no impact on the consolidated financial statements of the Group.

Amendments to IAS 1 Disclosure Initiative (applicable for annual periods beginning after January 1, 2016): At the end of

2014, the IASB issued amendments to IAS 1 which provide (a) clarification on materiality, (b) guidance on the list of line

items to be presented in the statement of financial position and in the statement of profit or loss and other comprehensive

income which can be disaggregated and aggregated as relevant and on subtotals in these statements, (c) clarification that

an entity's share of OCI of equity-accounted associates and joint ventures should be presented in aggregate as single line

items based on whether or not it will subsequently be reclassified to profit or loss and (d) additional examples of possible

ways of ordering the notes.

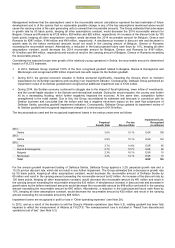

IFRS 9 Financial Instruments (applicable for annual periods beginning after January 1, 2018): During 2014, the IASB issued

the complete version of IFRS 9 which will replace the guidance in IAS 39 upon the former’s effective date.

IFRS 9 retains, but simplifies the mixed measurement model and establishes three primary measurement categories for

financial assets: (a) amortized cost, (b) fair value through OCI and (c) fair value through P&L. The basis of classification

depends on the entity’s business model and the contractual cash flow characteristics of the financial asset. Investments in

equity instruments are required to be measured at fair value through profit or loss with the irrevocable option at inception to

present changes in fair value in OCI without any future recycling possibility.

The standard introduces the expected credit losses model and replaces the incurred credit loss impairment model used in

IAS 39. The expected credit loss model requires an entity to account for expected credit losses and changes in those

expected credit losses at each reporting date to reflect changes in credit risk since initial recognition which effectively results

that it will be no longer necessary for a credit event to have occurred before credit losses are recognized.

FINANCIAL STATEMENTS