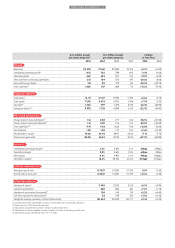

Food Lion 2014 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2014 Food Lion annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

Delhaize Group Annual Report 2014 • 9

• Increasing consumer demand for trans-

parency about our products; for example,

where they are from and how they are

produced.

• Health trends including the increase of

diet-related diseases (obesity, diabetes,

malnutrition) impacting customer health

needs and expectations.

• Increasing pressure on both agriculture

and oceanic resources impacts price and

availability of our products; for example,

the increasing global demand for food,

decreasing availability of water, diminishing

soil quality, and climate change impacts

such as droughts and storms.

So, to prepare us to stay competitive in this

changing world, we established the Super-

good 2020 strategy. On the path to meeting

our 2020 goals, we are changing how we do

business – from how we design and source

our private brand products, to how we foster

healthy living among our customers and

associates.

Being a Supergood company underpins the

way we operate and is simply good business:

our Supergood ambition is to delight our

customers and energize our associates by

helping them live happier and eat healthier in

thriving local communities.

The following pages show our strategy in

action across our markets as we meet today’s

challenges and prepare for those we will face

tomorrow.

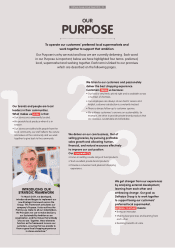

2015 PRIORITIES

Put the customer back

at the center

• Provide a great local shopping

experience in stores and on-line

Engage great people

• Develop a strong performance

culture

• Offer development opportunities

Connect with communities

• Support thriving communities

• Improve our offer of nutritious,

sustainable, and affordable

private brands

• Empower healthy and

sustainable living

Create value in line with our peers

• Support growth opportunities

• Realize operating excellence

and efficiencies

• Maximize our assets’ potential

and return

Align our information technology (IT)

and business priorities

Concretely, in the U.S., we will be

further focusing and careful rolling

out the Food Lion “Easy, Fresh &

Affordable… You Can Count on Food

Lion Every Day!” commercial strategy.

We will also continue to accelerate

growth at Hannaford. In order to

realize operating excellence and

efficiencies, we will implement the

Transformation Plan in Belgium and

maximize the benefits of Coopernic,

our European buying alliance. In

Southeastern Europe and Indonesia,

we remain focused on further store

expansion and comparable store

sales growth.

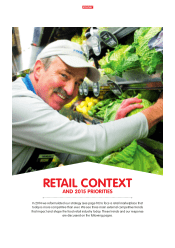

First, large format stores, particularly

hypermarkets are being challenged. Several

large players are experiencing a slowdown

of comparable store sales (CSS) in their core

large formats. Thus they are developing

smaller formats as well as on-line alternatives

to try to revive growth. Second, the rise of the

discounters has progressed unabated. Thirdly,

as the number of channels proliferates –

discount, traditional, hypermarket, club, dollar,

online – the blurring of boundaries between

formats continues. Food retailers are joining

other industries in developing, testing, and

refining different business models to adapt to

both new consumer demands as well as a

changing competitive landscape. The result is

that shoppers no longer distinguish between

formats; they only want their favorite products

at the best prices. In addition, and because of

these trends, margins in the retail sector are

increasingly being squeezed.

Our response to these trends is to refine

and update our formats and intensify our

e-commerce efforts while continuing to invest

in the customer proposition. Our goal is to be

known as the best in fresh, with an efficient

yet innovative assortment, delivering the best

shopping experience at the best everyday

value.

Our sustainability strategy is called “Super-

good”. Our Supergood strategy is in response

to other trends we see impacting food retail:

Our goal is to be known as the

best in fresh, with an efficient yet

innovative assortment, delivering

the best shopping experience at

the best everyday value.