Entergy 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

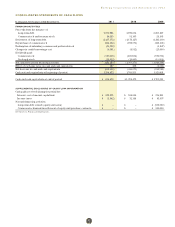

Entergy Corporation and Subsidiaries 2011

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

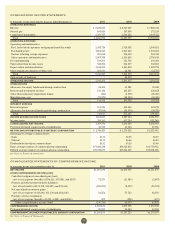

will recover its value within a reasonable period of time. Entergy’s

trusts are managed by third parties who operate in accordance with

agreements that define investment guidelines and place restrictions on

the purchases and sales of investments. See Note 17 to the financial

statements for details on the decommissioning trust funds and other

than temporary impairments recorded in 2011, 2010, and 2009.

Equity Method Investments

Entergy owns investments that are accounted for under the equity

method of accounting because Entergy’s ownership level results

in significant influence, but not control, over the investee and its

operations. Entergy records its share of earnings or losses of the investee

based on the change during the period in the estimated liquidation

value of the investment, assuming that the investee’s assets were to

be liquidated at book value. In accordance with this method, earnings

are allocated to owners or members based on what each partner

would receive from its capital account if, hypothetically, liquidation

were to occur at the balance sheet date and amounts distributed were

based on recorded book values. Entergy discontinues the recognition

of losses on equity investments when its share of losses equals or

exceeds its carrying amount for an investee plus any advances made

or commitments to provide additional financial support. See Note 14 to

the financial statements for additional information regarding Entergy’s

equity method investments.

Derivative Financial Instruments and

Commodity Derivatives

The accounting standards for derivative instruments and hedging

activities require that all derivatives be recognized at fair value on the

balance sheet, either as assets or liabilities, unless they meet various

exceptions including the normal purchase, normal sales criteria. The

changes in the fair value of recognized derivatives are recorded each

period in current earnings or other comprehensive income, depending

on whether a derivative is designated as part of a hedge transaction

and the type of hedge transaction.

Contracts for commodities that will be physically delivered in

quantities expected to be used or sold in the ordinary course of

business, including certain purchases and sales of power and fuel,

meet the normal purchase, normal sales criteria and are not recognized

on the balance sheet. Revenues and expenses from these contracts

are reported on a gross basis in the appropriate revenue and expense

categories as the commodities are received or delivered.

For other contracts for commodities in which Entergy is hedging

the variability of cash flows related to a variable-rate asset, liability,

or forecasted transactions that qualify as cash flow hedges, the

changes in the fair value of such derivative instruments are reported

in other comprehensive income. To qualify for hedge accounting, the

relationship between the hedging instrument and the hedged item

must be documented to include the risk management objective and

strategy and, at inception and on an ongoing basis, the effectiveness

of the hedge in offsetting the changes in the cash flows of the item

being hedged. Gains or losses accumulated in other comprehensive

income are reclassified to earnings in the periods when the underlying

transactions actually occur. The ineffective portions of all hedges are

recognized in current-period earnings.

Entergy has determined that contracts to purchase uranium do not

meet the definition of a derivative under the accounting standards for

derivative instruments because they do not provide for net settlement

and the uranium markets are not sufficiently liquid to conclude that

forward contracts are readily convertible to cash. If the uranium

markets do become sufficiently liquid in the future and Entergy begins

to account for uranium purchase contracts as derivative instruments,

the fair value of these contracts would be accounted for consistent

with Entergy’s other derivative instruments.

Fair Values

The estimated fair values of Entergy’s financial instruments and

derivatives are determined using bid prices and market quotes.

Considerable judgment is required in developing the estimates of

fair value. Therefore, estimates are not necessarily indicative of the

amounts that Entergy could realize in a current market exchange.

Gains or losses realized on financial instruments held by regulated

businesses may be reflected in future rates and therefore do not accrue

to the benefit or detriment of stockholders. Entergy considers the

carrying amounts of most financial instruments classified as current

assets and liabilities to be a reasonable estimate of their fair value

because of the short maturity of these instruments. See Note 16 to the

financial statements for further discussion of fair value.

Impairment of Long-Lived Assets

Entergy periodically reviews long-lived assets held in all of its business

segments whenever events or changes in circumstances indicate that

recoverability of these assets is uncertain. Generally, the determination

of recoverability is based on the undiscounted net cash flows expected

to result from such operations and assets. Projected net cash flows

depend on the future operating costs associated with the assets, the

efficiency and availability of the assets and generating units, and the

future market and price for energy over the remaining life of the assets.

Three nuclear power plants in the Entergy Wholesale Commodities

business segment (Pilgrim, Indian Point 2 and Indian Point 3) have

applications pending for renewed NRC licenses. Various parties have

expressed opposition to renewal of the licenses. Under federal law,

nuclear power plants may continue to operate beyond their license

expiration dates while their renewal applications are pending NRC

approval. If the NRC does not renew the operating license for any of

these plants, the plant’s operating life could be shortened, reducing its

projected net cash flows and impairing its value as an asset.

In March 2011 the NRC renewed Vermont Yankee’s operating license

for an additional 20 years. The renewed operating license expires in

March 2032. In May 2011 the Vermont Department of Public Service

and the New England Coalition petitioned the United States Court

of Appeals for the D.C. Circuit seeking judicial review of the NRC’s

issuance of the renewed operating license, alleging that the license had

been issued without a valid and effective water quality certification

under Section 401 of the Clean Water Act. Entergy Nuclear Vermont

Yankee and Entergy Nuclear Operations, Inc. intervened in the

proceeding. Motions by the parties for summary disposition were

denied by the court, and oral argument is scheduled for May 2012.

Vermont Yankee also is operating under a Certificate of Public Good

from the State of Vermont that expires in March 2012, but has an

application pending before the Vermont Public Service Board (VPSB)

for a new Certificate of Public Good for operation until March 2032.

As the United States district court noted in its decision discussed

below (regarding Entergy’s challenge to certain conditions imposed by

Vermont), title 3, section 814 of the Vermont Statutes provides that a

license subject to an agency’s notice and hearing requirements does

not expire until a final determination on an application for renewal

has been made.

65