Entergy 2011 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2011 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

Entergy Corporation and Subsidiaries 2011

MANAGEMENT’S FINANCIAL DISCUSSION AND ANALYSIS continued

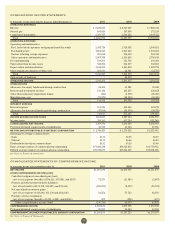

Energy 2012 2013 2014 2015 2016

Percent of planned generation

sold forward:

Unit-contingent 61% 38% 14% 12% 12%

Unit-contingent with

guarantee of availability(1) 16% 19% 15% 13% 13%

Firm LD 24% 24% 10% –% –%

Offsetting positions (13%) –% –% –% –%

Total energy sold forward 88% 81% 39% 25% 25%

Planned generation (TWh)(2)(3) 41 40 41 41 40

Average revenue under

contract per MWh(4) $49 $45-50 $49-54 $49-57 $50-59

Capacity 2012 2013 2014 2015 2016

Percent of capacity sold forward:

Bundled capacity and

energy contracts 18% 16% 16% 16% 16%

Capacity contracts 39% 26% 25% 11% –%

Total capacity sold forward 57% 42% 41% 27% 16%

Planned net MW in operation(3) 4,998 4,998 4,998 4,998 4,998

Average revenue under

contract per kW per month $2.4 $3.2 $3.1 $2.9 $–

(applies to capacity contracts only)

Blended Capacity and Energy Recap (based on revenues)

% of planned generation and capacity

sold forward 90% 80% 43% 27% 26%

Average revenue under contract

per MWh(4) $51 $47 $51 $52 $52

(1) A sale of power on a unit-contingent basis coupled with a guarantee of

availability provides for the payment to the power purchaser of contract

damages, if incurred, in the event the seller fails to deliver power as a

result of the failure of the specified generation unit to generate power at

or above a specified availability threshold. All of Entergy’s outstanding

guarantees of availability provide for dollar limits on Entergy’s maximum

liability under such guarantees.

(2) Amount of output expected to be generated by Entergy Wholesale

Commodities nuclear units considering plant operating characteristics,

outage schedules, and expected market conditions which impact dispatch.

(3) Assumes NRC license renewal for plants whose current licenses expire

within five years and the continued operation of all six plants. NRC license

renewal applications are in process for three units, as follows (with current

license expirations in parentheses): Pilgrim (June 2012), Indian Point 2

(September 2013), and Indian Point 3 (December 2015). For a discussion

regarding the continued operation of the Vermont Yankee plant, see

“Impairment of Long-Lived Assets” in Note 1 to the financial statements.

(4) Revenue on a per unit basis at which generation output, capacity, or

a combination of both is expected to be sold to third parties (including

offsetting positions), given existing contract or option exercise prices based

on expected dispatch or capacity, excluding the revenue associated with the

amortization of the below-market PPA for Palisades. Revenue may fluctuate

due to factors including positive or negative basis differentials, option

premiums and market prices at time of option expiration, costs to convert

firm LD to unit-contingent, and other risk management costs. Also, average

revenue under contract excludes payments owed under the value sharing

agreement with NYPA.

Entergy estimates that a $10 per MWh change in the annual

average energy price in the markets in which the Entergy Wholesale

Commodities nuclear business sells power, based on the respective

year-end market conditions, planned generation volumes, and hedged

positions, would have a corresponding effect on pre-tax net income of

$48 million in 2012 and would have had a corresponding effect on pre-

tax net income of $17 million in 2011.

Entergy’s purchase of the FitzPatrick and Indian Point 3 plants

from NYPA included value sharing agreements with NYPA. In October

2007, NYPA and the subsidiaries that own the FitzPatrick and Indian

Point 3 plants amended and restated the value sharing agreements to

clarify and amend certain provisions of the original terms. Under the

amended value sharing agreements, the Entergy subsidiaries agreed

to make annual payments to NYPA based on the generation output of

the Indian Point 3 and FitzPatrick plants from January 2007 through

December 2014. Entergy subsidiaries will pay NYPA $6.59 per MWh

for power sold from Indian Point 3, up to an annual cap of $48 million,

and $3.91 per MWh for power sold from FitzPatrick, up to an annual

cap of $24 million. The annual payment for each year’s output is due

by January 15 of the following year. Entergy will record the liability

for payments to NYPA as power is generated and sold by Indian

Point 3 and FitzPatrick. In 2011, 2010, and 2009, Entergy Wholesale

Commodities recorded a $72 million liability for generation during

each of those years. An amount equal to the liability was recorded

each year to the plant asset account as contingent purchase price

consideration for the plants. This amount will be depreciated over the

expected remaining useful life of the plants.

Some of the agreements to sell the power produced by Entergy

Wholesale Commodities’ power plants contain provisions that

require an Entergy subsidiary to provide collateral to secure its

obligations under the agreements. The Entergy subsidiary is required

to provide collateral based upon the difference between the current

market and contracted power prices in the regions where Entergy

Wholesale Commodities sells power. The primary form of collateral

to satisfy these requirements is an Entergy Corporation guaranty.

Cash and letters of credit are also acceptable forms of collateral.

At December 31, 2011, based on power prices at that time, Entergy

had liquidity exposure of $133 million under the guarantees in

place supporting Entergy Wholesale Commodities transactions, $20

million of guarantees that support letters of credit, and $6 million

of posted cash collateral to the ISOs. As of December 31, 2011, the

liquidity exposure associated with Entergy Wholesale Commodities

assurance requirements would increase by $132 million for a $1

per MMBtu increase in gas prices in both the short-and long-term

markets. In the event of a decrease in Entergy Corporation’s credit

rating to below investment grade, based on power prices as of

December 31, 2011, Entergy would have been required to provide

approximately $44 million of additional cash or letters of credit

under some of the agreements.

As of December 31, 2011, substantially all of the counterparties

or their guarantors for 100% of the planned energy output under

contract for Entergy Wholesale Commodities nuclear plants through

2016 have public investment grade credit ratings.

NUCLEAR MATTERS

After the nuclear incident in Japan resulting from the March 2011

earthquake and tsunami, the NRC established a task force to

conduct a review of processes and regulations relating to nuclear

facilities in the United States. The task force issued a near term

(90-day) report in July 2011 that has made recommendations, which

are currently being evaluated by the NRC. It is anticipated that the

NRC will issue certain orders and requests for information to nuclear

plant licensees by the end of the first quarter 2012 that will begin

to implement the task force’s recommendations. These orders may

require U.S. nuclear operators, including Entergy, to undertake plant

modifications or perform additional analyses that could, among

other things, result in increased costs and capital requirements

associated with operating Entergy’s nuclear plants.

CRITICAL ACCOUNTING ESTIMATES

The preparation of Entergy’s financial statements in conformity with

generally accepted accounting principles requires management to

apply appropriate accounting policies and to make estimates and

judgments that can have a significant effect on reported financial

position, results of operations, and cash flows. Management has

identified the following accounting policies and estimates as critical

because they are based on assumptions and measurements that

involve a high degree of uncertainty, and the potential for future

changes in these assumptions and measurements could produce

estimates that would have a material effect on the presentation of

Entergy’s financial position, results of operations, or cash flows.

49