Entergy 2011 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2011 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

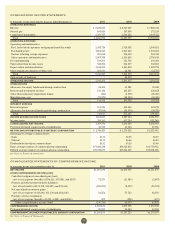

Entergy Corporation and Subsidiaries 2011

MANAGEMENT’S FINANCIAL DISCUSSION AND ANALYSIS concluded

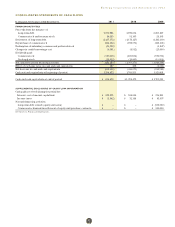

contributed $76.1 million to its postretirement plans in 2011. Entergy’s

current estimate of contributions to its other postretirement

plans is approximately $80.4 million in 2012.

FE DE R AL HE A LTHCA R E LEG I SL ATI ON

The Patient Protection and Affordable Care Act (PPACA) became

federal law on March 23, 2010, and, on March 30, 2010, the Health

Care and Education Reconciliation Act of 2010 became federal law

and amended certain provisions of the PPACA. These new federal

laws change the law governing employer-sponsored group health

plans, like Entergy’s plans, and include, among other things, the

following significant provisions:

n A 40% excise tax on per capita medical benefit costs that exceed

certain thresholds;

n Change in coverage limits for dependents; and

n Elimination of lifetime caps.

The total impact of PPACA is not yet determinable because

technical guidance regarding application must still be issued.

Additionally, ongoing litigation and discussions are in progress

regarding the constitutionality of and the potential repeal of health

care reform, although whether that occurs and what parts of health

care reform would be invalidated or repealed is not yet known.

Entergy will continue to monitor these developments to determine

the possible impact on Entergy as a result of PPACA. Entergy is

participating in the programs currently provided for under PPACA,

such as the early retiree reinsurance program, which has provided

for some limited reimbursements of certain claims for early retirees

aged 55 to 64 who are not yet eligible for Medicare.

One provision of the new law that is effective in 2013 eliminates

the federal income tax deduction for prescription drug expenses of

Medicare beneficiaries for which the plan sponsor also receives the

retiree drug subsidy under Part D. Entergy receives subsidy payments

under the Medicare Part D plan and therefore in the first quarter 2010

recorded a reduction to the deferred tax asset related to the unfunded

other postretirement benefit obligation. The offset was recorded in

2010 as a $16 million charge to income tax expense or, for the Utility,

including each Registrant Subsidiary, as a regulatory asset.

Other Contingencies

As a company with multi-state domestic utility operations and

a history of international investments, Entergy is subject to a

number of federal, state, and international laws and regulations

and other factors and conditions in the areas in which it operates,

which potentially subject it to environmental, litigation, and other

risks. Entergy periodically evaluates its exposure for such risks

and records a reserve for those matters which are considered

probable and estimable in accordance with generally accepted

accounting principles.

ENVI R ONMENTAL

Entergy must comply with environmental laws and regulations

applicable to the handling and disposal of hazardous waste. Under

these various laws and regulations, Entergy could incur substantial

costs to restore properties consistent with the various standards.

Entergy conducts studies to determine the extent of any required

remediation and has recorded reserves based upon its evaluation of

the likelihood of loss and expected dollar amount for each issue.

Additional sites could be identified which require environmental

remediation for which Entergy could be liable. The amounts of

environmental reserves recorded can be significantly affected by the

following external events or conditions:

n Changes to existing state or federal regulation by governmental

authorities having jurisdiction over air quality, water quality,

control of toxic substances and hazardous and solid wastes, and

other environmental matters.

n The identification of additional sites or the filing of other

complaints in which Entergy may be asserted to be a potentially

responsible party.

n The resolution or progression of existing matters through the

court system or resolution by the EPA.

LITIGAT ION

Entergy is regularly named as a defendant in a number of lawsuits

involving employment, customers, and injuries and damages issues,

among other matters. Entergy periodically reviews the cases in

which it has been named as defendant and assesses the likelihood

of loss in each case as probable, reasonably estimable, or remote

and records reserves for cases which have a probable likelihood of

loss and can be estimated. Given the environment in which Entergy

operates, and the unpredictable nature of many of the cases in

which Entergy is named as a defendant, the ultimate outcome of the

litigation to which Entergy is exposed has the potential to materially

affect the results of operations of Entergy or Registrant Subsidiaries.

UNCERTAI N TA X POSITIO N S

Entergy’s operations, including acquisitions and divestitures,

require Entergy to evaluate risks such as the potential tax effects

of a transaction, or warranties made in connection with such a

transaction. Entergy believes that it has adequately assessed and

provided for these types of risks, where applicable. Any provisions

recorded for these types of issues, however, could be significantly

affected by events such as claims made by third parties under

warranties, additional transactions contemplated by Entergy, or

completion of reviews of the tax treatment of certain transactions or

issues by taxing authorities.

NEW ACCOUNTING PRONOUNCEMENTS

The accounting standard-setting process, including projects between

the FASB and the International Accounting Standards Board (IASB) to

converge U.S. GAAP and International Financial Reporting Standards,

is ongoing and the FASB and the IASB are each currently working on

several projects that have not yet resulted in final pronouncements. Final

pronouncements that result from these projects could have a material

effect on Entergy’s future net income or financial position, or cash flows.

In May 2011 the FASB issued ASU No. 2011-4, “Fair Value

Measurement (Topic 820): Amendments to Achieve Common Fair

Value Measurement and Disclosure Requirements in U.S. GAAP

and IFRSs,” which states that the ASU explains how to measure fair

value. The ASU states that: 1) the amendments in the ASU result

in common fair value measurement and disclosure requirements

in U.S. GAAP and International Financial Reporting Standards; 2)

consequently, the amendments change the wording used to describe

many of the requirements in U.S. GAAP for measuring fair value and

for disclosing information about fair value measurements; 3) for

many of the requirements, the FASB does not intend for the ASU to

result in a change in the application of the requirements of current

U.S. GAAP; 4) some of the amendments clarify the FASB’s intent about

the application of existing fair value measurement requirements; and

5) other amendments change a particular principle or requirement

for measuring fair value or for disclosing information about fair

value measurements. ASU No. 2011-4 is effective for Entergy for the

first quarter 2012. Entergy does not expect ASU No. 2011-4 to affect

materially its results of operations, financial position, or cash flows.

In September 2011 the FASB issued ASU No. 2011-8, “Intangibles

– Goodwill and Other (Topic 350): Testing Goodwill for Impairment.”

The amendments permit an entity to first assess qualitative factors

to determine whether it is more likely than not that the fair value

of a reporting unit is less than its carrying amount as a basis for

determining whether it is necessary to perform a quantitative goodwill

impairment assessment. ASU No. 2011-8 is effective for Entergy for

the first quarter 2012. ASU No. 2011-8 will have no effect on Entergy’s

results of operations, financial position, or cash flows.

53