Entergy 2011 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2011 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

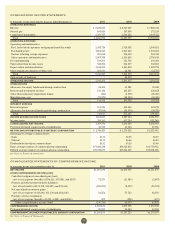

Entergy Corporation and Subsidiaries 2011

MANAGEMENT’S FINANCIAL DISCUSSION AND ANALYSIS continued

generation assets are subject to impairment if adverse market

conditions arise, if a unit ceases operation, or for certain units if

their operating licenses are not renewed. Entergy’s investments in

merchant non-nuclear generation assets are subject to impairment if

adverse market conditions arise or if a unit ceases operation.

In order to determine if Entergy should recognize an impairment

of a long-lived asset that is to be held and used, accounting standards

require that the sum of the expected undiscounted future cash

flows from the asset be compared to the asset’s carrying value.

The carrying value of the asset includes any capitalized asset

retirement cost associated with the recording of an additional

decommissioning liability, therefore changes in assumptions that

affect the decommissioning liability can increase or decrease the

carrying value of the asset subject to impairment. If the expected

undiscounted future cash flows exceed the carrying value, no

impairment is recorded; if such cash flows are less than the carrying

value, Entergy is required to record an impairment charge to write

the asset down to its fair value. If an asset is held for sale, an

impairment is required to be recognized if the fair value (less costs

to sell) of the asset is less than its carrying value.

These estimates are based on a number of key assumptions,

including:

n FUTURE POWER AND FUEL PRICES – Electricity and gas prices

have been very volatile in recent years, and this volatility is

expected to continue. This volatility necessarily increases the

imprecision inherent in the long-term forecasts of commodity

prices that are a key determinant of estimated future cash flows.

n MARKET VALUE OF GENERATION ASSETS – Valuing assets

held for sale requires estimating the current market value of

generation assets. While market transactions provide evidence

for this valuation, the market for such assets is volatile and the

value of individual assets is impacted by factors unique to

those assets.

n FUTURE OPERATING COSTS – Entergy assumes relatively minor

annual increases in operating costs. Technological or regulatory

changes that have a significant impact on operations could cause

a significant change in these assumptions.

n TIMING – Entergy currently assumes, for a number of its nuclear

units, that the plant’s license will be renewed. A change in that

assumption could have a significant effect on the expected future

cash flows and result in a significant effect on operations.

For additional discussion regarding the continued operation of

the Vermont Yankee plant, see “Impairment of Long-Lived Assets” in

Note 1 to the financial statements.

Effective January 1, 2009, Entergy adopted an accounting

pronouncement providing guidance regarding recognition and

presentation of other-than-temporary impairments related to

investments in debt securities. The assessment of whether an

investment in a debt security has suffered an other-than-temporary

impairment is based on whether Entergy has the intent to sell or

more likely than not will be required to sell the debt security before

recovery of its amortized costs. Further, if Entergy does not expect to

recover the entire amortized cost basis of the debt security, an other-

than-temporary-impairment is considered to have occurred and it is

measured by the present value of cash flows expected to be collected

less the amortized cost basis (credit loss). For debt securities held

as of January 1, 2009 for which an other-than-temporary impairment

had previously been recognized but for which assessment under

the new guidance indicates this impairment is temporary, Entergy

recorded an adjustment to its opening balance of retained earnings

of $11.3 million ($6.4 million net-of-tax). Entergy did not have

any material other than temporary impairments relating to credit

losses on debt securities in 2011, 2010 or 2009. The assessment of

whether an investment in an equity security has suffered an other

than temporary impairment continues to be based on a number of

factors including, first, whether Entergy has the ability and intent to

hold the investment to recover its value, the duration and severity

of any losses, and, then, whether it is expected that the investment

will recover its value within a reasonable period of time. Entergy’s

trusts are managed by third parties who operate in accordance with

agreements that define investment guidelines and place restrictions

on the purchases and sales of investments. As discussed in Note 1 to

the financial statements, unrealized losses that are not considered

temporarily impaired are recorded in earnings for Entergy Wholesale

Commodities. Entergy Wholesale Commodities recorded charges

to other income of $0.1 million in 2011, $1 million in 2010, and $86

million in 2009 resulting from the recognition of impairments of

certain securities held in its decommissioning trust funds that are not

considered temporary. Additional impairments could be recorded in

2012 to the extent that then current market conditions change the

evaluation of recoverability of unrealized losses.

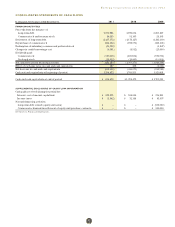

Qualified Pension and Other

Postretirement Benefits

Entergy sponsors qualified, defined benefit pension plans which

cover substantially all employees. Additionally, Entergy currently

provides postretirement health care and life insurance benefits for

substantially all employees who reach retirement age and meet

certain eligibility requirements while still working for Entergy.

Entergy’s reported costs of providing these benefits, as described

in Note 11 to the financial statements, are impacted by numerous

factors including the provisions of the plans, changing employee

demographics, and various actuarial calculations, assumptions,

and accounting mechanisms. Because of the complexity of these

calculations, the long-term nature of these obligations, and the

importance of the assumptions utilized, Entergy’s estimate of these

costs is a critical accounting estimate for the Utility and Entergy

Wholesale Commodities segments.

ASSUMPT IONS

Key actuarial assumptions utilized in determining these costs include:

n Discount rates used in determining future benefit obligations;

n Projected health care cost trend rates;

n Expected long-term rate of return on plan assets;

n Rate of increase in future compensation levels;

n Retirement rates; and

n Mortality rates.

Entergy reviews the first four assumptions listed above on an

annual basis and adjusts them as necessary. The falling interest

rate environment and volatility in the financial equity markets have

impacted Entergy’s funding and reported costs for these benefits.

In addition, these trends have caused Entergy to make a number of

adjustments to its assumptions.

The retirement and mortality rate assumptions are reviewed

every three to five years as part of an actuarial study that compares

these assumptions to the actual experience of the pension and

other postretirement plans. The 2011 actuarial study reviewed plan

experience from 2007 through 2010. As a result of the 2011 actuarial

study, changes were made to reflect the expectation that participants

have longer life expectancies and different retirement patterns than

previously assumed. These changes are reflected in the December

31, 2011 financial disclosures and are a significant factor in the

increase in 2012 pension and other postretirement costs compared

to the 2011 costs.

In selecting an assumed discount rate to calculate benefit

obligations, Entergy reviews market yields on high-quality corporate

debt and matches these rates with Entergy’s projected stream of

benefit payments. Based on recent market trends, the discount rates

used to calculate its qualified pension benefit obligation decreased

from a range of 5.6% to 5.7% for its specific pension plans in 2010 to

51