Entergy 2003 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2003 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

|

|

76

ENTERGY CORPORATION AND SUBSIDIARIES 2003

NUCLEAR DECOMMISSIONING COSTS

SFAS 143, “Accounting for Asset Retirement Obligations,”

which was implemented effective January 1, 2003, requires

the recording of liabilities for all legal obligations associated

with the retirement of long-lived assets that result from the

normal operation of those assets. For Entergy, these asset

retirement obligations consist of its liability for decommis-

sioning its nuclear power plants.

These liabilities are recorded at their fair values (which is

the present values of the estimated future cash outflows) in

the period in which they are incurred, with an accompanying

addition to the recorded cost of the long-lived asset. The

asset retirement obligation is accreted each year through a

charge to expense, to reflect the time value of money for this

present value obligation. The amounts added to the carrying

amounts of the long-lived assets will be depreciated over the

useful lives of the assets. The net effect of implementing

this standard for the rate-regulated business of the domestic

utility companies and System Energy was recorded as a

regulatory asset, with no resulting impact on Entergy’s net

income. Entergy recorded these regulatory assets because

existing rate mechanisms in each jurisdiction are based on

the principle that Entergy will recover all ultimate costs of

decommissioning from customers.

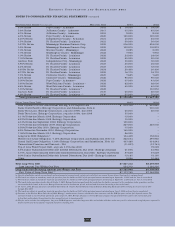

Assets and liabilities increased approximately $1.1 billion

for the domestic utility companies and System Energy as a

result of recording the asset retirement obligations at their

fair values of $1.1 billion as determined under SFAS 143,

increasing utility plant by $287 million, reducing accumu-

lated depreciation by $361 million and recording the

related regulatory assets of $422 million. The implementation

of SFAS 143 for the portion of River Bend not subject to

cost-based ratemaking decreased earnings by approximately

$21 million net-of-tax ($0.09 per share) as a result of a one-

time cumulative effect of accounting change. In accordance

with ratemaking treatment and as required by SFAS 71, the

depreciation provisions for the domestic utility companies

and System Energy include a component for removal costs

that are not asset retirement obligations under SFAS 143.

In accordance with regulatory accounting principles,

Entergy has recorded a regulatory asset for certain of its

domestic utility companies and System Energy of approxi-

mately $72.4 million as of December 31, 2003 and approxi-

mately $79.6 million as of December 31, 2002 to reflect an

estimate of incurred but uncollected removal costs previous-

ly recorded as a component of accumulated depreciation.

The decommissioning and retirement cost liability for cer-

tain of the domestic utility companies and System Energy

includes a regulatory liability of approximately $26.8 million

as of December 31, 2003 and approximately $25.5 million

as of December 31, 2002 representing an estimate of collected

but not yet incurred removal costs. For the Non-Utility

Nuclear business, the implementation of SFAS 143 resulted

in a decrease in liabilities of approximately $595 million due

to reductions in decommissioning liabilities, a decrease in

assets of approximately $340 million, including a decrease

in electric plant in service of $315 million, and an increase

in earnings in the first quarter of 2003 of approximately

$155 million net-of-tax ($0.67 per share) as a result of a

one-time cumulative effect of accounting change.

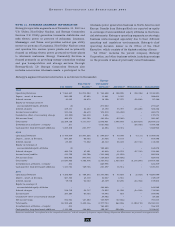

The cumulative decommissioning liabilities and expenses

recorded in 2003 by Entergy were as follows (in millions):

Liabilities Liabilities

as of SFAS 143 as of

Dec. 31, 2002 Adoption Accretion Spending Dec. 31, 2003

ANO 1 & ANO 2 $ 310.7 $ 221.0 $ 35.8 $ – $ 567.5

River Bend 237.0 41.2 20.6 – 298.8

Waterford 3 125.3 179.4 20.6 – 325.3

Grand Gulf 1 153.5 137.2 21.8 – 312.5

Pilgrim 490.2 (292.6) 15.8 – 213.4

Indian Point 1 & 2 456.9 (207.3) 19.9 11.8 257.7

Vermont Yankee 316.7 (95.1) 17.7 – 239.3

$2,090.3 $ (16.2) $152.2 $11.8 $2,214.5

In addition, an insignificant amount of removal costs

associated with non-nuclear power plants are also included

in the decommissioning line item on the balance sheet.

Entergy periodically reviews and updates estimated decom-

missioning costs. The actual decommissioning costs may

vary from the estimates because of regulatory require-

ments, changes in technology, and increased costs of labor,

materials, and equipment.

If Entergy had applied SFAS 143 during prior periods,

the following impacts would have resulted:

For the years ended December 31, 2002 2001

Asset retirement obligations

actually recorded $2,090,269 $1,679,738

Pro forma effect

of SFAS 143 $ (46,041) $ 28,512

Asset retirement obligations -

pro forma $2,044,228 $1,708,250

Earnings applicable to

common stock - as reported $ 599,360 $ 726,196

Pro forma effect

of SFAS 143 $ 14,119 $ 9,613

Earnings applicable to

common stock - pro forma $ 613,479 $ 735,809

Basic earnings per average

common share - as reported $2.69 $3.29

Pro forma effect

of SFAS 143 $0.06 $0.04

Basic earnings per average

common share - pro forma $2.75 $3.33

Diluted earnings per average

common share - as reported $2.64 $3.23

Pro forma effect

of SFAS 143 $0.06 $0.04

Diluted earnings per average

common share - pro forma $2.70 $3.27

For the Indian Point 3 and FitzPatrick plants purchased

in 2000, NYPA retained the decommissioning trusts and

the decommissioning liability. NYPA and Entergy executed

decommissioning agreements, which specify their decom-

missioning obligations. NYPA has the right to require

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

continued