Entergy 2003 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2003 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

46

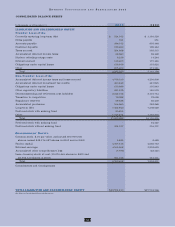

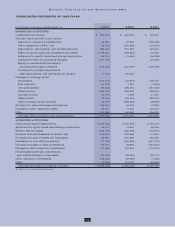

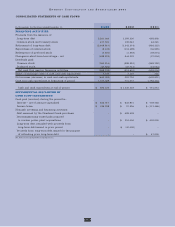

ENTERGY CORPORATION AND SUBSIDIARIES 2003

Conversely, commodity contracts that are not considered

derivatives, generally because they involve physical

delivery of a commodity to the purchaser, are not marked

to market. Examples of commodity contracts that are

not marked to market include:

the PPAs for Entergy’s Non-Utility Nuclear plants;

capacity purchases and sales by the U.S. Utility

companies; and

forward contracts that will result in physical delivery.

Fair value estimates of the commodity instruments that

are marked to market are made at discrete points in time

based on relevant market information. Market quotes are

used in determining fair value whenever they are available.

When market quotes are not available (e.g., long-dated

commodity contract), other information is used, including

transactional data and internally developed models. Fair

value estimates based on these other methodologies are

necessarily subjective in nature and involve uncertainties

and matters of significant judgment. These uncertainties

include projections of macroeconomic trends and future

commodity prices, including supply and demand levels and

future price volatility. The impact of these uncertainties,

however, is lessened by the relatively short-term nature of

the mark-to-market positions held by Entergy and EKT.

PENSION AND OTHER POSTRETIREMENT BENEFITS

Entergy sponsors defined benefit pension plans which

cover substantially all employees. Additionally, Entergy

provides postretirement health care and life insurance

benefits for substantially all employees who reach retirement

age while still working for Entergy. Entergy’s reported costs

of providing these benefits, as described in Note 11 to the

consolidated financial statements, are impacted by numerous

factors including the provisions of the plans, changing

employee demographics and various actuarial calculations,

assumptions, and accounting mechanisms. Because of the

complexity of these calculations, the long-term nature of

these obligations, and the importance of the assumptions

utilized, Entergy’s estimate of these costs is a critical

accounting estimate for the U.S. Utility and Non-Utility

Nuclear segments.

Assumptions

Key actuarial assumptions utilized in determining these

costs include:

Discount rates used in determining the future benefit

obligations;

Projected health care cost trend rates;

Expected long-term rate of return on plan assets; and

Rate of increase in future compensation levels.

Entergy reviews these assumptions on an annual basis

and adjusts them as necessary. The falling interest rate

environment and poor performance of the financial equity

markets over the past several years have impacted

Entergy’s funding and reported costs for these benefits. In

addition, these trends have caused Entergy to make a

number of adjustments to its assumptions.

In selecting an assumed discount rate, Entergy reviews

market yields on high-quality corporate debt. Based on

recent market trends, Entergy reduced its discount rate

from 7.5% in 2001 and 6.75% in 2002 to 6.25% in 2003.

Entergy reviews actual recent cost trends and projected

future trends in establishing health care cost trend rates.

Based on this review, Entergy increased its health care cost

trend rate assumption used in calculating the 2003

accumulated postretirement benefit obligation. The assumed

health care cost trend rate is a 10% increase in health care

costs in 2004 gradually decreasing each successive year

until it reaches a 4.5% annual increase in health care costs

in 2010 and beyond.

In determining its expected long-term rate of return on

plan assets, Entergy reviews past long-term performance,

asset allocations, and long-term inflation assumptions.

Entergy targets an asset allocation for its pension plan

assets of roughly 66% equity securities, 30% fixed income

securities, and 4% other investments. The target allocation

for Entergy’s other postretirement benefit assets is

45% equity securities and 55% fixed income securities.

Based on recent market trends, Entergy decreased its

expected long-term rate of return on plan assets from 9% in

2001 to 8.75% for 2002 and 2003. The trend of reduced

inflation caused Entergy to reduce its assumed rate of

increase in future compensation levels from 4.6% in 2001 to

3.25% in 2002 and 2003.

Cost Sensitivity

The following chart reflects the sensitivity of pension cost

to changes in certain actuarial assumptions (in thousands):

Actuarial Change in Impact on 2003 Impact on Projected

Assumption Assumption Pension Cost Benefit Obligation

Increase/(Decrease)

Discount rate (0.25%) $4,882 $83,651

Rate of return

on plan assets (0.25%) $4,346 –

Rate of increase

in compensation 0.25% $4,039 $ 28,101

MANAGEMENT’S FINANCIAL DISCUSSION AND ANALYSIS

continued