ComEd 2003 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2003 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

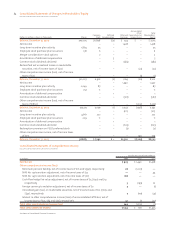

89Notes to Consolidated Financial Statements

EXELON CORPORATION AND SUBSIDIARY COMPANIES

Asset Impairments

Long-Lived Assets. Exelon evaluates the carrying value of

long-lived assets to be held and used for impairment when-

ever indications of impairment exist in accordance with the

requirements of SFAS No. 144, “Accounting for the Impair-

ment or Disposal of Long-Lived Assets” (SFAS No. 144). The

carrying value of long-lived assets is considered impaired

when the projected undiscounted cash flows are less than

the carrying value. In that event, a loss would be recognized

based on the amount by which the carrying value exceeds

the fair value. Fair value is determined primarily by available

market valuations or discounted cash flows. See Note 2 –

Acquisitions and Dispositions for a description of the

impairment recorded in 2003 related to the long-lived assets

of Boston Generating, LLC (Boston Generating), formerly

known as Exelon Boston Generating, LLC.

Upon meeting certain criteria defined in SFAS No. 144,

the assets and associated liabilities that compose a disposal

group are classified as held for sale and the carrying value of

these assets is adjusted downward, if necessary, to the esti-

mated sales price, less cost to sell. See Note 2 – Acquisitions

and Dispositions for a description of assets and liabilities

classified as held for sale as of December 31, 2003 and

impairments recorded related to these assets.

Goodwill. Goodwill represents the excess of the purchase

price paid over the estimated fair value of the assets ac-

quired and liabilities assumed in the acquisition of a busi-

ness. As of January 1, 2002, Exelon adopted SFAS No. 142,

“Goodwill and Other Intangible Assets” (SFAS No. 142). Pur-

suant to SFAS No. 142, goodwill is no longer amortized but is

tested for impairment at least annually or on an interim ba-

sis if an event occurs or circumstances change that would

reduce the fair value of a reporting unit below its carrying

value. Prior to January 1, 2002, goodwill was amortized using

the straight-line method over its estimated period of benefit.

Goodwill associated with the merger of Exelon, Unicom Cor-

poration (Unicom), and PECO on October 20, 2000 (Merger)

was amortized on a straight-line basis over 40 years in 2001.

Goodwill associated with other acquisitions was amortized

over periods from 10 to 20 years in 2001. See Note 8 – Good-

will for information regarding the adoption of SFAS No. 142

and Cumulative Effect of Changes in Accounting Principles

below for pro forma net income and earnings per common

share for the year ended December 31, 2001, adjusted as if

SFAS No. 142 had been applied effective January 1, 2001.

Investments. Investments are considered to be impaired

when a decline in fair value is judged to be other-than-

temporary. If the cost of an investment exceeds its fair value,

Exelon evaluates, among other factors, general market con-

ditions, the duration and extent to which the fair value is

less than cost, as well as its intent and ability to hold the in-

vestment. Exelon also considers specific adverse conditions

related to the financial health of and business outlook for

the investee. Once a decline in fair value is determined to be

other-than-temporary, an impairment charge is recorded

and a new cost basis is established. See Note 3 – Sithe for a

description of the impairments recorded in 2003 related to

Generation’s investment in Sithe.

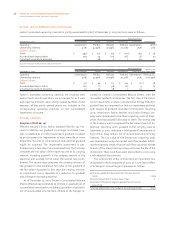

Derivative Financial Instruments

Exelon adopted SFAS No. 133, “Accounting for Derivatives and

Hedging Activities” (SFAS No. 133) on January 1, 2001. As a

result, Generation recognized a non-cash gain of $12 million,

net of income taxes, in earnings and deferred a non-cash

gain of $4 million, net of income taxes, in accumulated other

comprehensive income and PECO deferred a non-cash gain

of $40 million, net of income taxes, in accumulated other

comprehensive income.

Under the provisions of SFAS No. 133, all derivatives are

recognized on the balance sheet at their fair value unless

they qualify for a normal purchases and normal sales ex-

ception. Changes in the derivatives recorded at fair value are

recognized in earnings unless specific hedge accounting cri-

teria are met, in which case those changes are recorded in

other comprehensive income. Gains and losses on “normal”

contracts are recognized when the underlying physical

transaction affects earnings. As part of Exelon’s energy mar-

keting business, Exelon enters into contracts to buy and sell

energy to meet the requirements of its customers. These

contracts include short-term and long-term commitments to

purchase and sell energy and energy-related products in the

retail and wholesale markets with the intent and ability to

deliver or take delivery. While these contracts are considered

derivative financial instruments under SFAS No. 133, the

majority of these transactions have been designated as

“normal purchases” or “normal sales” and are thus not re-

quired to be recorded at fair value, but on an accrual basis of

accounting.

A derivative financial instrument can be designated as a

hedge of the fair value of a recognized asset or liability or of

an unrecognized firm commitment (fair-value hedge), or a

hedge of a forecasted transaction or the variability of cash

flows to be received or paid related to a recognized asset or

liability (cash-flow hedge). Changes in the fair value of a de-

rivative that is highly effective as, and is designated and

qualifies as, a fair-value hedge, along with the gain or loss on

the hedged asset or liability that is attributable to the

hedged risk, are recorded in earnings. Changes in the fair

value of a derivative that is highly effective as, and is des-

ignated as and qualifies as, a cash-flow hedge are recorded

in other comprehensive income, until earnings are affected

by the variability of cash flows being hedged.

In connection with Exelon’s Risk Management Policy

(RMP), Exelon enters into derivatives to manage its exposure