ComEd 2003 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2003 ComEd annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

54 Management’s Discussion and Analysis of Financial Condition and Results of Operations

EXELON CORPORATION AND SUBSIDIARY COMPANIES

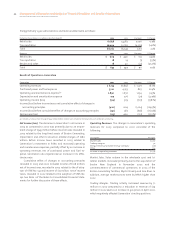

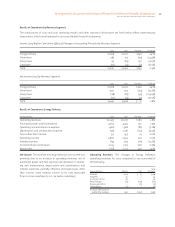

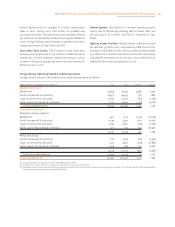

Generation’s average revenue per MWh sold for 2002

and 2001 were as follows:

($/MWh) 2002 2001 % Change

Average revenue

Energy Delivery and Exelon

Energy Company $33.98 $ 33.05 2.8%

Market sales 31.01 37.00 (16.2%)

Total—excluding the

trading portfolio 32.78 34.51 (5.0%)

The factors below contributed to the overall reduction in

Generation’s average margin for 2002.

Generation’s GWh deliveries increased 6% in 2002 pri-

marily due to favorable weather conditions, which increased

demand for Energy Delivery and increased market sales at-

tributable to the availability of increased supply from ac-

quired generation and power uprates at existing facilities,

slightly offset by a decrease in sales to Exelon Energy Com-

pany, Enterprises’ retail energy unit, due to lower demand in

the eastern energy markets.

Generation’s supply mix changed due to:

– increased purchases resulting from the supply agreement

with AmerGen’s Unit No. 1 at Three Mile Island Nuclear Sta-

tion facility which was new in 2002,

– decreased nuclear generation due to an increase in the

number of refueling outages during 2002, slightly offset by

power uprates,

– increased fossil and hydroelectric net generation due to the

acquisition of two generating plants in April, a peaking fa-

cility placed in service in July and the Sithe New England

plants acquired in November, which in total accounted for

an increase of 2,500 GWhs, and strong waterflows which

increased the hydroelectric output by 400 GWhs, and

– lower production in our Mid-Atlantic coal and oil units due

to cooler summer weather conditions and lower power

prices in 2002.

Generation’s average revenue was affected by:

– increased weighted average on and off peak prices per

MWh for supply agreements with ComEd,

– higher contracted prices from Exelon Energy Company, af-

fected by lower actual volumes to those customers, and

– lower market prices.

2002 2001

Nuclear fleet capacity factor(a) 92.7% 94.4%

Nuclear fleet production cost per MWh(a) $13.00 $12.78

Average purchased power cost for wholesale

operations per MWh(b) $41.85 $45.94

(a) Including AmerGen and excluding Salem, which is operated by PSE&G.

(b) Including PPAs with AmerGen.

The lower nuclear capacity factor and increased nuclear

production costs are primarily due to 260 days of planned

outage time in 2002 versus 153 days in 2001. Nuclear pro-

duction cost increased from $12.78 to $13.00 primarily due to

an $80 million increase in outage costs and the number of

refueling outages in 2002 as compared to 2001. These

decreases are slightly offset by a $25 million decrease in pay-

roll costs due to headcount reductions and $4 million in

lower project expenditures. The decrease in purchased

power costs was primarily due to depressed wholesale

power market prices.

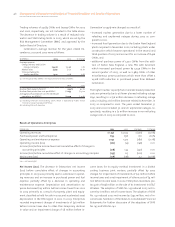

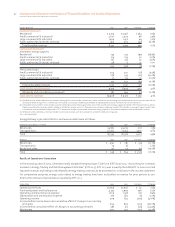

Results of Operations–Enterprises

Enterprises 2002 2001 Variance % Change

Operating revenues $2,033 $2,292 $(259) (11.3%)

Purchased power and fuel expense 658 854 (196) (23.0%)

Operating and maintenance expense 1,327 1,436 (109) (7.6%)

Operating income (loss) (14) (77) 63 (81.8%)

Income (loss) before income taxes and cumulative effect of change in

accounting principle 134 (128) 262 n.m.

Income (loss) before cumulative effect of change in accounting principles 65 (85) 150 (176.5%)

Net income (loss) (178) (85) (93) 109.4%

n.m. —not meaningful

Net Income (Loss). The increase in Enterprises’ income (loss)

before cumulative effect of change in accounting principles

was primarily due to a pre-tax gain of $198 million recorded

in 2002 on the sale of its investment in AT&T Wireless and

decreases in purchased power and fuel expense and operat-

ing and maintenance expense, partially offset by a decrease

in operating revenues. Depreciation and amortization ex-

pense decreased $14 million from 2001 to 2002 primarily as a

result of the discontinuance of goodwill amortization upon

the adoption of SFAS No. 142 on January 1, 2002, partially off-

set by 2002 accelerated depreciation in the PJM region. In

2002, Enterprises recorded impairment charges of invest-

ments of $41 million before income taxes due to other-than-

temporary declines in value and a net impairment of other

assets of $4 million, as compared to 2001 charges for

investment impairments of $13 million and a net impair-

ment of other assets of $2 million before income taxes. In

2002, Enterprises had higher equity in earnings of uncon-