Clearwire 2009 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2009 Clearwire annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

|

|

b

roa

db

an

d

networ

k

s

i

nt

h

eUn

i

te

d

States to cover as many as 120 m

illi

on peop

l

e

b

yt

h

een

d

o

f

2010. Our

actual network covera

g

eb

y

the end of 2010 will lar

g

el

y

be determined b

y

our abilit

y

to successfull

y

mana

g

e

ongoing development activities and our performance in our launched markets. We believe that thi

s

d

ep

l

oyment w

ill

ena

bl

e us to rap

idl

y

i

ncrease our su

b

scr

ib

er

b

ase. Our networ

ki

s pos

i

t

i

one

d

to target a

ran

g

e of subscribers, from individuals, households and businesses to market se

g

ments that depend on mobil

e

c

ommun

i

cat

i

ons. We w

ill

o

ff

er our serv

i

ces t

h

roug

h

mu

l

t

i

p

l

e reta

il

sa

l

es c

h

anne

l

s,

i

nc

l

u

di

ng

di

rect an

d

i

n

di

rect sa

l

es representat

i

ves, company-owne

d

reta

il

stores,

i

n

d

epen

d

ent

d

ea

l

ers, Internet sa

l

es, te

l

esa

l

es

,

n

at

i

ona

l

reta

il

c

h

a

i

ns an

d

manu

f

acturers w

h

oem

b

e

d

our

high

spee

di

nternet access capa

bili

t

i

es

i

nt

o

c

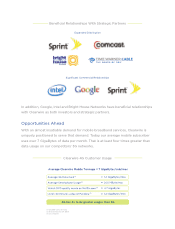

onsumer electronic devices. Our services are also expected to be offered by third parties under wholesale

arrangements, including wholesale services through our Strategic Partners — Sprint, Comcast, Tim

e

Warner Ca

bl

e, Br

igh

t House, Inte

l

an

d

Goo

gl

ew

h

o serve more t

h

an 100 m

illi

on customers

i

nt

h

e

i

r mar

k

ets.

•

Ta

k

ing a

d

vantage of our

l

ea

d

ing spectrum position:

W

e

b

e

li

eve we

h

o

ld

more w

i

re

l

ess s

p

ectrum

i

nt

h

e

United States than any other mobile carrier, with holdings at December 31, 2009 exceeding 44 billion MHz-

P

OPs (

d

e

fi

ne

d

as t

h

e pro

d

uct o

f

t

h

e num

b

er o

f

mega

h

ertz assoc

i

ate

d

w

i

t

h

a spectrum

li

cense mu

l

t

i

p

li

e

db

y

the estimated population of the license’s service area) of spectrum in the 2.5 GHz (2496-2690 MHz) band in

our portfolio, includin

g

spectrum we own, lease or have pendin

g

a

g

reements to acquire or lease. We hol

d

approximately 150 MHz of spectrum on average in the largest 100 markets in the United States. In Europe

,

we

h

o

ld

approx

i

mate

l

y 8.3

billi

on MHz-POPs o

f

spectrum as o

f

Decem

b

er 31, 2009, pre

d

om

i

nant

l

y

i

nt

he

3

.

5

GHz band, with a var

y

in

g

amount of spectrum in each of our markets. We believe that consumers will

c

ont

i

nue to

d

eman

d

greater access to

i

n

f

ormat

i

on, app

li

cat

i

ons an

d

on

li

ne enterta

i

nment over t

h

e Internet,

e

ac

h

o

f

w

hi

c

h

w

ill

requ

i

re serv

i

ce prov

id

ers to

b

ea

bl

etoo

ff

er greater

b

an

d

w

id

t

h

access. W

i

t

h

our grow

i

ng

4G mobile broadband networks and leadin

g

spectrum position, we believe that we are uniquel

y

positioned t

o

s

atisfy this demand. We believe that our significant spectrum holdings, both in terms of spectrum depth an

d

breadth, in the 2.

5

GHz band will be optimal for delivering broadband access services, and we believe tha

t

our su

b

stant

i

a

l

s

p

ectrum

d

e

p

t

h

s

h

ou

ld

a

ll

ow us to o

ff

er

p

rem

i

um serv

i

ces an

dd

ata

i

ntens

i

ve mu

l

t

i

me

di

a

c

on

t

en

t.

•

Levera

g

in

g

ke

y

strate

g

ic relationships

:

W

e expect to benefit from our key strategic relationships with our

S

trate

gi

c Partners. Our W

h

o

l

esa

l

e Partners

h

ave

b

e

g

un o

ff

er

i

n

g

our serv

i

ces as part o

f

t

h

e

i

r

b

un

dl

e

db

ran

d

e

d

o

ff

er

i

n

g

,or

h

ave announce

d

t

h

e

i

r

i

ntent

i

ons to o

ff

er t

h

ese serv

i

ces. We

h

ave commerc

i

a

l

a

g

reements w

i

t

h

I

ntel intended to facilitate embeddin

g

mobile WiMAX chipsets in PCs, mobile Internet devices, which w

e

re

f

er to as MIDs, an

d

ot

h

er

d

ev

i

ces. We a

l

so

h

ave agreements w

i

t

h

Goog

l

e to prov

id

e

f

or searc

h

an

d

a

d

vert

i

s

i

n

g

revenue s

h

ar

i

n

g

,aswe

ll

as, to

j

o

i

nt

ly d

eve

l

op open arc

hi

tecture

d

ev

i

ces, an

d

to ma

k

e

d

es

k

to

p

and mobile content and applications available on our 4G networks. Additionall

y

, our a

g

reements with Sprin

t

a

ll

ow us to prov

id

e our customers w

i

t

hd

ua

l

mo

d

e

d

ev

i

ces t

h

at a

ll

ow roam

i

ng

b

etween our 4G networ

k

san

d

S

pr

i

nt’s nat

i

onw

id

e 3G networ

k

,an

d

ena

bl

eusto

l

everage Spr

i

nt’s ex

i

st

i

ng

i

n

f

rastructure

f

or our

b

u

ild

ou

t

and network deplo

y

ment

.

•

Off

ering premium value-added services and content

:

W

e believe that our all – IP 4G mobile broadband

n

etwor

k

pos

i

t

i

ons us to generate

i

ncrementa

l

revenues,

l

everage our cost structure an

di

mprove su

b

scr

ib

e

r

retent

i

on

b

yo

ff

er

i

ng a var

i

ety o

f

prem

i

um serv

i

ces an

d

content over our networ

k

.We

i

nten

di

n

i

t

i

a

ll

yto

f

ocu

s

on voice services as a primar

y

premium service. As of December 31, 2009, we offered VoIP telephon

y

s

ervices on a fixed basis to our subscribers’ homes and offices in

5

6 of our

5

7 domestic markets. We believ

e

t

h

at our p

l

anne

d

4G mo

bil

e

b

roa

db

an

dd

ep

l

o

y

ment w

ill

ena

bl

eustoo

ff

er a

ddi

t

i

ona

l

prem

i

um serv

i

ces an

d

c

ontent over our networ

k

as manu

f

acturers

d

eve

l

op an

d

se

ll

su

b

scr

ib

er

d

ev

i

ces t

h

at ta

k

ea

d

vanta

g

eo

f

t

he

c

apabilities of 4G technology.

•

Achieving e

ff

icient economics: We believe our economic model for deploying our network combine

s

m

ean

i

n

gf

u

l

ear

ly

covera

g

ew

hil

e opt

i

m

i

z

i

n

g

t

h

e cap

i

ta

l

out

l

a

y

requ

i

re

df

or us to

b

u

ild

t

h

e networ

k

an

d

o

b

ta

i

nsu

b

scr

ib

ers. Our

d

ep

l

o

y

ment p

l

an

i

s

b

ase

d

on rep

li

ca

bl

ean

d

sca

l

a

bl

e

i

n

di

v

id

ua

l

mar

k

et

b

u

ild

s

,

allowin

g

us to repeat our build-out processes as we expand. Under our commercial a

g

reements with Sprint

,

we expect to

b

ea

bl

eto

l

everage ex

i

st

i

ng Spr

i

nt networ

ki

n

f

rastructure to

b

ot

h

acce

l

erate t

h

e

b

u

ild

-out an

d

re

d

uce t

h

e costs o

f

networ

kd

ep

l

oyment,

i

nc

l

u

di

ng ut

ili

z

i

ng

i

ts towers, co

ll

ocat

i

on

f

ac

ili

t

i

es an

d fib

er

resources. We also ex

p

ect to achieve lower subscriber ac

q

uisition costs due to manufacturers’ stated

p

lans t

o

7