Symantec 2002 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2002 Symantec annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

|

|

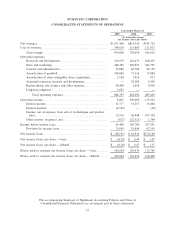

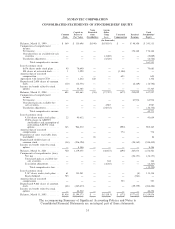

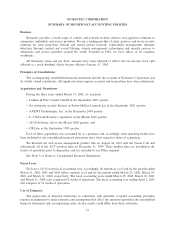

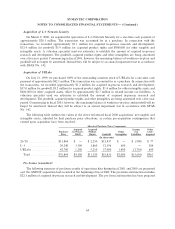

SYMANTEC CORPORATION

SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Ì (Continued)

The lessors associated with lease agreements relating to certain of our facilities, described under Synthetic

Leases in Note 7 of Notes to Consolidated Financial Statements, are special purpose entities or equivalent

structures. Presently, we account for these leases as operating leases, while the special purpose entities or

equivalent structures own and account for the leased assets and related liabilities in their records. The FASB

has indicated that it will, prior to June 30, 2002, issue proposed new rules on accounting for ""Entities That

Lack SuÇcient Independent Economic Substance'', including special purpose entities, in the form of an

Interpretation to SFAS No. 94, Consolidation of All Majority-Owned Subsidiaries, and Accounting Research

Bulletin No. 51, Consolidated Financial Statements. Based on public comments from the FASB to date, the

proposed interpretation will provide guidance for determining when an entity (such as us), the Primary

BeneÑciary, should consolidate another entity, a special purpose entity or equivalent structure (such as the

lessor), that functions to support the activities of the Primary BeneÑciary. The expected proposed Interpreta-

tion may result in us having to consolidate the operating results of the special purpose entities and equivalent

structures, which are the lessors under the aforementioned operating lease agreements. The eÅective date of

these proposed new rules on our current operating leases could be as early as the beginning of our Ñscal year

2004, and sooner on any new leases entered into after the new rules' eÅective date which utilize special

purpose entities or equivalent structures.

ReclassiÑcations

Certain previously reported amounts have been reclassiÑed to conform to the current presentation format

with no impact on net income (loss). All related Ñnancial information has been restated to conform to this

presentation.

60