Spirit Airlines 2011 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2011 Spirit Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

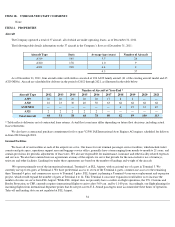

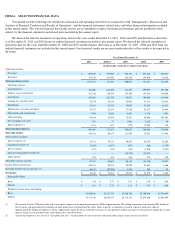

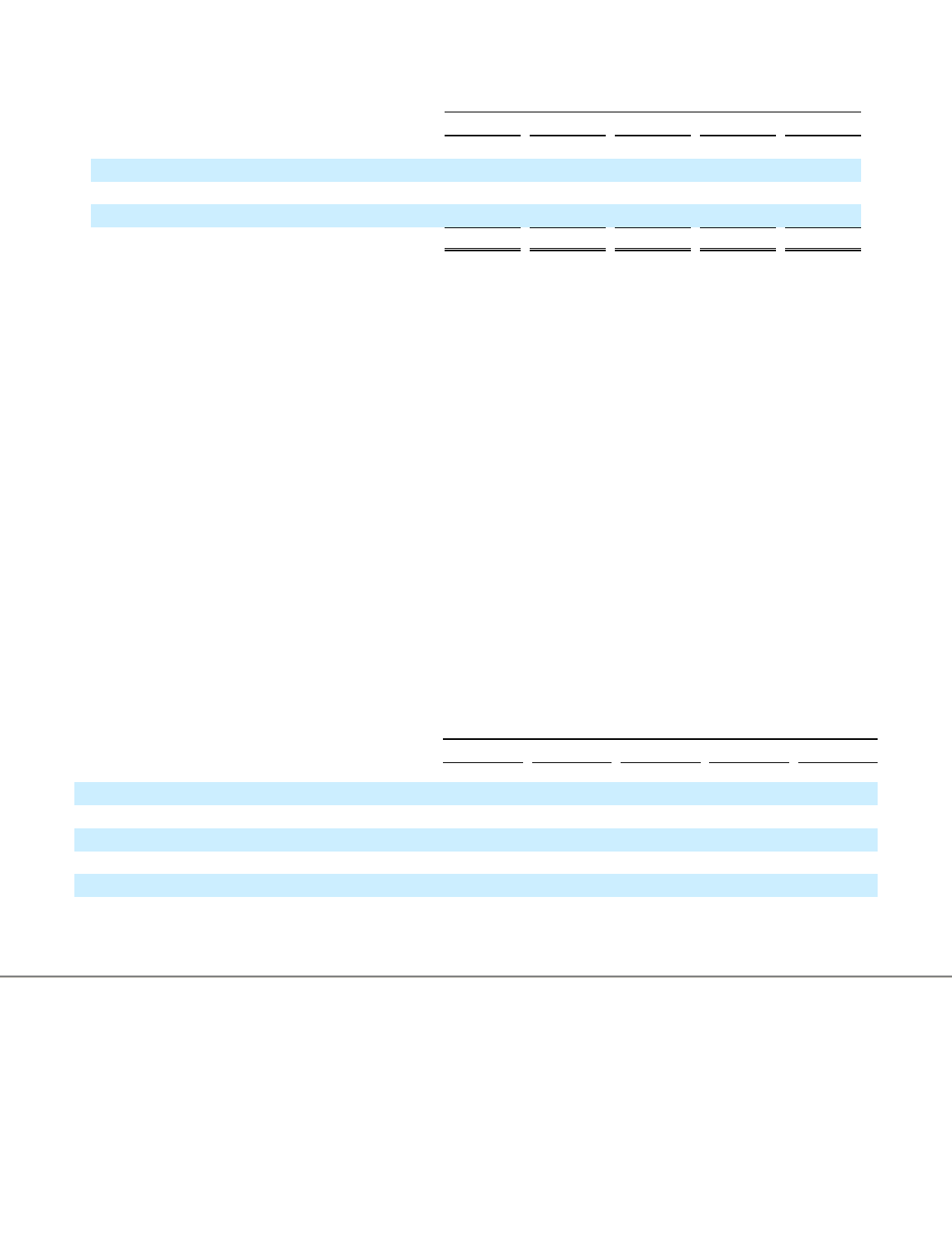

(ii) settlement gains and losses and (iii) unrealized mark-to-market gains and losses associated with fuel hedge contracts. The following table summarizes the components

of aircraft fuel expense for the periods presented:

The following table presents balance sheet data for the periods presented.

39

Year Ended December 31,

2011

2010

2009

2008 (*)

2007

(in thousands)

Into-plane fuel cost

$

392,278

$

251,754

$

181,806

$

359,097

$

265,226

Settlement (gains) losses

(7,436

)

(1,483

)

750

(69,876

)

(3,714

)

Unrealized mark-to-market (gains) losses

3,204

(2,065

)

(1,449

)

9,873

(10,282

)

Aircraft Fuel

$

388,046

$

248,206

$

181,107

$

299,094

$

251,230

(*) In July 2008, we monetized all of our fuel hedge contracts, which included hedges that had scheduled settlement dates during the remainder of 2008 and in

2009. We recognized a gain of $37.8 million representing cash received upon monetization of these contracts, of which a gain of $14.2 million related to 2009

fuel hedge positions on these contracts.

(3) Special charges include: (i) for 2007, amounts relating to the accelerated retirement of our MD-80 fleet; (ii) for 2008 and 2009, amounts relating to the early termination

in mid-2008 of leases for seven Airbus A319 aircraft, a related reduction in workforce and the exit facility costs associated with returning planes to lessors in 2008; (iii)

for 2009 and 2010, amounts relating to the sale of previously expensed MD-

80 parts; (iv) for 2010 and 2011 amounts relating to exit facility costs associated with moving

our Detroit, Michigan maintenance operations to Fort Lauderdale, Florida; and (v) termination costs in connection with the IPO during the three months ended June 30,

2011 comprised of amounts paid to Indigo Partners, LLC to terminate its professional services agreement with us and fees paid to three individual, unaffiliated holders of

our subordinated notes. Special charges for 2011 also include legal, accounting, printing, and filing fees connected with the secondary offering which was consummated

on January 25, 2012 . For more information, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Our Operating

Expenses—Special Charges.”

(4) Substantially all of the interest expense recorded in 2007, 2008, 2009, 2010 and 2011 relates to notes and preferred stock held by our principal stockholders that were

repaid or redeemed, or exchanged for shares of common stock, in connection with the 2011 Recapitalization.

(5)

Interest attributable to funds used to finance the acquisition of new aircraft, including PDPs is capitalized as an additional cost of the related asset. Interest is capitalized at

the weighted average implicit lease rate of our aircraft.

(6) Gain on extinguishment of debt represents the recognition of contingencies provided for in our 2006 recapitalization agreements, which provided for the cancellation of

shares of Class A preferred stock and reduction of the liquidation preference of the remaining Class A preferred stock and associated accrued but unpaid dividends based

on the outcome of the contingencies.

(7)

Net income for 2010 includes a $52.3 million net tax benefit primarily due to the release of a valuation allowance resulting in a deferred tax benefit of $52.8 million in

2010. Absent the release of the valuation allowance and corresponding tax benefit, our net income would have been $19.7 million for 2010. Pursuant to the Tax

Receivable Agreement, we distributed to the Pre-IPO Stockholders the right to receive a pro rata share of the future payments to be made under such agreement. These

future payments to the Pre-IPO Stockholders (estimated as of December 31, 2011 to be approximately $36.5 million) will be in an amount equal to 90% of the cash

savings in federal income tax realized by us by virtue of our future use of the federal net operating loss, deferred interest deductions and certain tax credits held by us as

of March 31, 2011. Please see "Notes to Financial Statements- 20. Initial Public Offering and Tax Receivable Agreement".

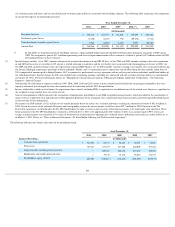

As of December 31,

2011

2010

2009

2008

2007

Balance Sheet Data: (in thousands)

Cash and cash equivalents

$

343,328

$

82,714

$

86,147

$

16,229

$

54,603

Total assets

745,813

475,757

327,866

240,009

257,382

Long-term debt, including current portion —

260,827

242,232

214,480

180,784

Mandatorily redeemable preferred stock —

79,717

75,110

89,685

138,777

Stockholders' equity (deficit)

466,706

(105,077

)

(178,127

)

(261,890

)

(295,154

)