Pottery Barn 2005 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2005 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

maintenance expenses. Although the current term of the lease expires in August 2006, we are obligated to renew

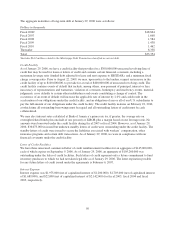

the operating lease on an annual basis until these bonds are fully repaid.

Our other Memphis-based distribution facility includes an operating lease entered into in August 1990 for

another distribution facility that is adjoined to the Partnership 1 facility in Memphis, Tennessee. The lessor is a

general partnership (“Partnership 2”) comprised of W. Howard Lester, James A. McMahan and two unrelated

parties. Partnership 2 does not have operations separate from the leasing of this distribution facility and does not

have lease agreements with any unrelated third parties.

Partnership 2 financed the construction of this distribution facility and related addition through the sale of a total

of $24,000,000 of industrial development bonds in 1990 and 1994. Quarterly interest and annual principal

payments are required through maturity in August 2015. The Partnership 2 industrial development bonds are

collateralized by the distribution facility and require us to maintain certain financial covenants. As of January 29,

2006, $13,809,000 was outstanding under the Partnership 2 industrial development bonds.

During fiscal 2005, we made annual rental payments of approximately $2,600,000, plus applicable taxes,

insurance and maintenance expenses. This operating lease has an original term of 15 years expiring in August

2006, with three optional five-year renewal periods. We are, however, obligated to renew the operating lease on

an annual basis until these bonds are fully repaid.

As of February 1, 2004, the Company adopted FIN 46R, which requires existing unconsolidated variable interest

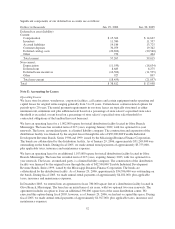

entities to be consolidated by their primary beneficiaries if the entities do not effectively disperse risks among

parties involved. The two partnerships described above qualify as variable interest entities under FIN 46R due to

their related party relationship and our obligation to renew the leases until the bonds are fully repaid.

Accordingly, the two related party variable interest entity partnerships from which we lease our Memphis-based

distribution facilities were consolidated by us as of February 1, 2004. As of January 29, 2006, the consolidation

resulted in increases to our consolidated balance sheet of $18,250,000 in assets (primarily buildings),

$15,696,000 in debt, and $2,554,000 in other long-term liabilities. Consolidation of these partnerships did not

have an impact on our net income. However, the interest expense associated with the partnerships’ debt, shown

as occupancy expense in fiscal 2003, is now recorded as interest expense. In fiscal 2005 and fiscal 2004, this

interest expense approximated $1,462,000 and $1,525,000, respectively.

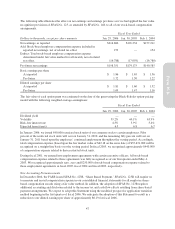

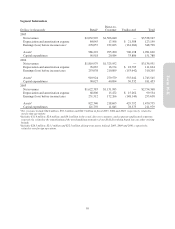

Note G: Earnings Per Share

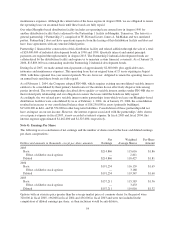

The following is a reconciliation of net earnings and the number of shares used in the basic and diluted earnings

per share computations:

Dollars and amounts in thousands, except per share amounts

Net

Earnings

Weighted

Average Shares

Per-Share

Amount

2005

Basic $214,866 115,616 $1.86

Effect of dilutive stock options — 2,811

Diluted $214,866 118,427 $1.81

2004

Basic $191,234 116,159 $1.65

Effect of dilutive stock options — 3,188

Diluted $191,234 119,347 $1.60

2003

Basic $157,211 115,583 $1.36

Effect of dilutive stock options — 3,433

Diluted $157,211 119,016 $1.32

Options with an exercise price greater than the average market price of common shares for the period were

320,000 in fiscal 2005, 196,000 in fiscal 2004 and 436,000 in fiscal 2003 and were not included in the

computation of diluted earnings per share, as their inclusion would be anti-dilutive.

54