Pep Boys 2010 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2010 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 29, 2011, January 30, 2010 and January 31, 2009

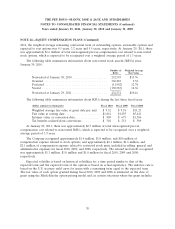

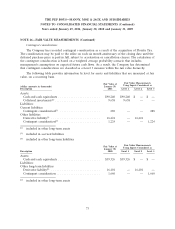

NOTE 14—EQUITY COMPENSATION PLANS (Continued)

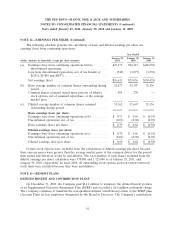

both a market and a service condition, the Month Carlo simulation model is used. The following are

the weighted-average assumptions:

Year ended

January 29, January 30, January 31,

2011 2010 2009

Dividend yield ......................... 1.35% 2.3% 2.93%

Expected volatility ....................... 56% 65% 45%

Risk-free interest rate range:

High ................................ 2.0% 2.3% 3.2%

Low................................. 0.9% 1.6% 2.7%

Ranges of expected lives in years ............ 4–5 4–5 3–4

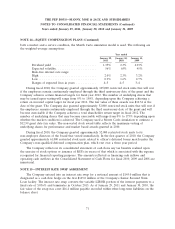

During fiscal 2010, the Company granted approximately 105,000 restricted stock units that will vest

if the employees remain continuously employed through the third anniversary date of the grant and the

Company achieves certain financial targets for fiscal year 2012. The number of underlying shares that

may be issued upon vesting will range from 0% to 150%, depending upon the Company achieving a

return on invested capital target for fiscal year 2012. The fair value of these awards was $10.34 at the

date of the grant. The Company also granted approximately 52,000 restricted stock units that will vest if

the employees remain continuously employed through the third anniversary date of the grant and will

become exercisable if the Company achieves a total shareholder return target in fiscal 2012. The

number of underlying shares that may become exercisable will range from 0% to 175% depending upon

whether the market condition is achieved. The Company used a Monte Carlo simulation to estimate a

$12.99 grant date fair value. The non-vested stock award table reflects the maximum vesting of

underlying shares for performance and market based awards granted in 2010.

During fiscal 2010, the Company granted approximately 52,000 restricted stock units to its

non-employee directors of the board that vested immediately. In the first quarter of 2010, the Company

granted approximately 61,000 restricted stock units related to officer’s deferred bonus match under the

Company’s non-qualified deferred compensation plan, which vest over a three year period.

The Company reflects in its consolidated statement of cash flows any tax benefits realized upon

the exercise of stock options or issuance of RSUs in excess of that which is associated with the expense

recognized for financial reporting purposes. The amounts reflected as financing cash inflows and

operating cash outflows in the Consolidated Statement of Cash Flows for fiscal 2010, 2009 and 2008 are

immaterial.

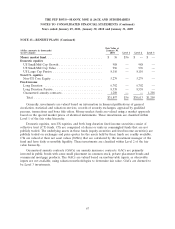

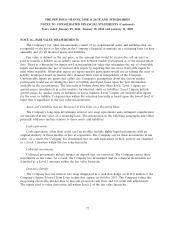

NOTE 15—INTEREST RATE SWAP AGREEMENT

The Company entered into an interest rate swap for a notional amount of $145.0 million that is

designated as a cash flow hedge on the first $145.0 million of the Company’s Senior Secured Term

Loan facility. The interest rate swap converts the variable LIBOR portion of the interest payments to a

fixed rate of 5.036% and terminates in October 2013. As of January 29, 2011 and January 30, 2010, the

fair value of the swap was a net $16.4 million payable recorded within other long-term liabilities on the

balance sheet.

71