Pep Boys 2010 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2010 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

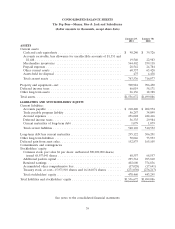

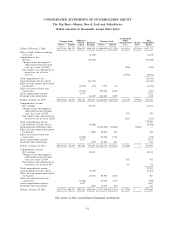

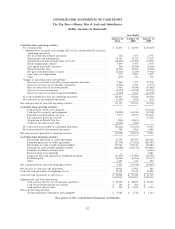

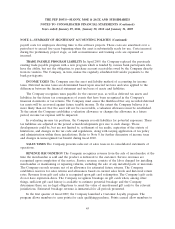

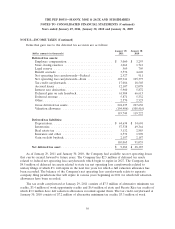

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 29, 2011, January 30, 2010 and January 31, 2009

NOTE 1—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

RECENT ACCOUNTING STANDARDS

In March 2007, the FASB issued guidance on accounting for split dollar life insurance

arrangements which was included in ASC 718 ‘‘Compensation—Stock Compensation.’’ This ASC

provides guidance on determining whether a liability for the postretirement benefit associated with a

collateral assignment split-dollar life insurance arrangement should be recorded. ASC 718 also provides

guidance on how a company should recognize and measure the asset in a collateral assignment split-

dollar life insurance contract. The original guidance for accounting for split dollar life insurance

arrangements was effective for fiscal years beginning after December 15, 2007. The adoption of

ASC 718 resulted in a $1.2 million net of tax charge to retained earnings on February 3, 2008.

In October 2009, the FASB issued Accounting Standards Update (‘‘ASU’’) 2009-13 ‘‘Revenue

Recognition (Topic 605)—Multiple-Deliverable Revenue Arrangements a consensus of the FASB

Emerging Issues Task Force,’’ (‘‘ASU 2009-13’’). This update eliminates the residual method of

allocation and requires that consideration be allocated to all deliverables using the relative selling price

method. ASU 2009-13 is effective for material revenue arrangements entered into or materially

modified in fiscal years beginning on or after June 15, 2010. The adoption of ASU 2009-13 did not

have a material impact on the consolidated financial statements.

In January 2010, the FASB issued ASU 2010-06 ‘‘Fair Value Measurements—Improving

Disclosures on Fair Value Measurements’’ (‘‘ASU 2010-06’’). This guidance requires new disclosures

surrounding transfers in and out of level 1 or 2 in the fair value hierarchy and also requires that the

reconciliation of level 3 inputs includes separately reported information on purchases, sales, issuances

and settlements. The increased disclosures should be reported for each class of assets or liabilities.

ASU 2010-06 also clarifies existing disclosures for the level of disaggregating, disclosures about

valuation techniques and inputs used to determine level 2 or 3 fair value measurements and includes

conforming amendments to the guidance on employers’ disclosures about postretirement benefit plan

assets. ASU 2010-06 was effective for interim and annual reporting periods beginning after

December 15, 2009 except for the disclosures about purchases, sales, issuances or settlements in the roll

forward activity for level 3 fair value measurements which are effective for interim and annual periods

beginning after December 15, 2010. The adoption of ASU 2010-06 did not have a material impact on

the Company’s consolidated financial statements.

In December 2010, the FASB issued ASU 2010-29 ‘‘Business Combinations (Topic 805)—

Disclosure of Supplementary Pro Forma Information for Business Combinations’’ (ASU 2010-29). This

accounting standard update clarifies that SEC registrants presenting comparative financial statements

should disclose in their pro forma information revenue and earnings of the combined entity as though

the current period business combinations had occurred as of the beginning of the comparable prior

annual reporting period only. The update also expands the supplemental pro forma disclosures to

include a description of the nature and amount of material, nonrecurring pro forma adjustments

directly attributable to the business combination included in the reported pro forma revenue and

earnings. ASU 2010-29 is effective prospectively for material (either on an individual or aggregate

basis) business combinations entered into in fiscal years beginning on or after December 15, 2010 with

early adoption permitted. The Company does not believe the adoption of those requirements of

ASU 2010-29 will have a material impact on the consolidated results of operations and financial

condition.

49