Pep Boys 2010 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2010 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

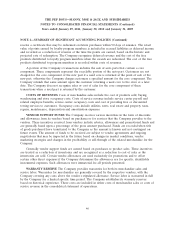

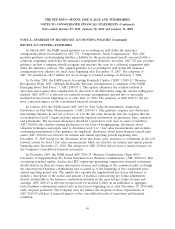

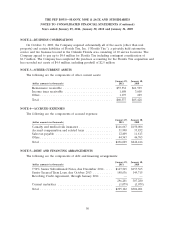

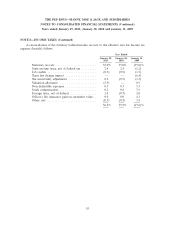

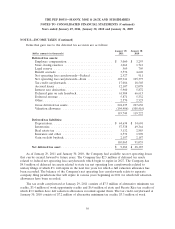

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended January 29, 2011, January 30, 2010 and January 31, 2009

NOTE 5—DEBT AND FINANCING ARRANGEMENTS (Continued)

7.50% Senior Subordinated Notes, due December 2014

On December 14, 2004, the Company issued $200.0 million aggregate principal amount of 7.50%

Senior Subordinated Notes (the ‘‘Notes’’) due December 2014. During fiscal 2010 and 2009, the

Company repurchased Notes in the principal amount of $10.0 million and $17.0 million, respectively,

resulting in a loss from debt repurchases of $0.2 million and a gain from debt repurchases of

$6.2 million, respectively.

Senior Secured Term Loan Facility, due October 2013

The Company has a Senior Secured Term Loan facility (the ‘‘Term Loan’’) due October 2013. This

facility is secured by a collateral pool consisting of real property and improvements associated with

stores, which is adjusted periodically based upon real estate values and borrowing levels. Interest

accrues at the London Interbank Offered Rate (LIBOR) plus 2.0% on this facility. As of January 29,

2011, 126 stores collateralized the Term Loan.

Revolving Credit Agreement, through January 2014

On January 16, 2009, the Company entered into a new Revolving Credit Agreement (the

‘‘Agreement’’) with available borrowings up to $300.0 million. The Company’s ability to borrow under

the Revolving Credit Agreement is based on a specific borrowing base consisting of inventory and

accounts receivable. Total fees of $6.8 million were capitalized and are being amortized over the five

year life of the Agreement. The interest rate on this credit line is LIBOR or Prime plus 2.75% to

3.25% based upon the then current availability under the Agreement. Fees based on the unused

portion of the facility range from 37.5 to 75.0 basis points. As of January 29, 2011, there were no

outstanding borrowings under the Agreement.

The weighted average interest rate on all debt borrowings during fiscal 2010 and 2009 was 6.3%

and 4.2%, respectively.

Other Matters

Several of the Company’s debt agreements require compliance with covenants. The most restrictive

of these requirements is contained in the Revolving Credit Agreement. During any period the

availability under the Agreement drops below the greater of $50,000 or 17.5% of the borrowing base,

the Company is required to maintain a consolidated fixed charge coverage ratio of at least 1.1:1.0,

calculated as the ratio of (a) EBITDA (net income plus interest charges, provision for taxes,

depreciation and amortization expense, non-cash stock compensation expenses and other non-recurring,

non-cash items) minus capital expenditures and income taxes paid to (b) the sum of debt service

charges and restricted payments made. The failure to satisfy this covenant would constitute an event of

default under the Agreement, which would result in a cross-default under the Notes and Term Loan.

As of January 29, 2011, the Company had no borrowings outstanding under the Revolving Credit

Agreement, additional availability of approximately $138.2 million and was in compliance with its

financial covenants.

51