Nordstrom 2007 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2007 Nordstrom annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

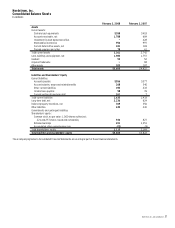

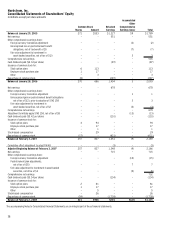

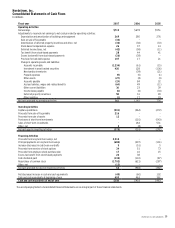

Nordstrom, Inc. and subsidiaries 31

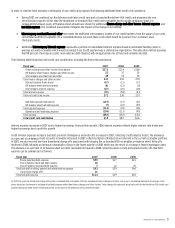

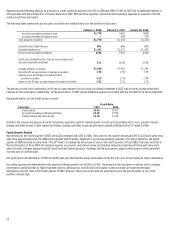

Allowance for Doubtful Accounts

Our allowance for doubtful accounts represents our best estimate of the losses inherent in our Nordstrom private label card and co-branded Nordstrom

VISA credit card receivables as of the balance sheet date. We evaluate the collectibility of our accounts receivable based on several factors, including

historical trends of aging of accounts, write-off experience and expectations of future performance. We recognize finance charges on delinquent

accounts until the account is written off. Delinquent accounts are written off when they are determined to be uncollectible, usually after the passage

of 151 days without receiving a full scheduled monthly payment. Accounts are written off sooner in the event of customer bankruptcy or other

circumstances that make further collection unlikely. Management believes the allowance for doubtful accounts is adequate to cover anticipated losses

in our credit card accounts receivable under current conditions; however, significant deterioration in any of the factors mentioned above or in general

economic conditions could materially change these expectations. In prior years, we have not made material changes to our estimates involved in the

allowance for doubtful accounts. A 10% change in our allowance for doubtful accounts would have affected net earnings by $4 for the fiscal year ended

February 2, 2008.

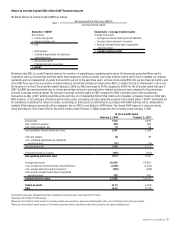

Income Taxes

In accordance with Statement of Financial Accounting Standards No. 109, “Accounting for Income Taxes,” we calculate income taxes using the asset

and liability approach. We recognize deferred tax assets and liabilities based on the difference between the financial statement carrying amounts and

respective tax bases of assets and liabilities. Deferred tax assets and liabilities are measured using enacted tax rates currently in effect for the years in

which we expect those temporary differences to reverse.

Inherent in the measurement of deferred balances are certain judgments and interpretations of enacted tax law and published guidance. Our

assumptions have been materially accurate in the past. We continuously monitor any changes in enacted tax rates in the jurisdictions in which we have

a filing obligation and adjust our deferred tax balances accordingly. We regularly evaluate whether our deferred tax assets will more likely than not be

realized in the foreseeable future and record a valuation allowance when appropriate.

In accordance with FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes,” we regularly evaluate the likelihood of recognizing

the benefit for income tax positions we have taken in various federal, state and foreign filings by considering all relevant facts, circumstances and

information available. For those benefits we believe more likely than not will be sustained, we recognize the largest amount we believe is cumulatively

greater than 50% likely to be realized. Our assumptions for these benefits have been materially accurate in the past. A liability for the unrecognized

portion of the income tax benefit will carry forward until the effective settlement of the issue on audit, the lapse in the statute of limitations to

consider the issue, or a favorable change in law.

RECENT ACCOUNTING PRONOUNCEMENTS

In September 2006, the FASB issued Statement of Financial Accounting Standards No. 157,

Fair Value Measurements

(“SFAS 157”). SFAS 157 defines fair value,

establishes a framework for measuring fair value, and expands disclosures about fair value measurements. In February 2008, the FASB issued FASB Staff

Position No. FAS 157-1 (“FSP FAS 157-1”) and FASB Staff Position No. FAS 157-2, (“FSP FAS 157-2”), affecting implementation of SFAS 157. FSP FAS 157-1 excludes

FASB Statement No. 13,

Accounting for Leases

(“SFAS 13”), and other accounting pronouncements that address fair value measurements under SFAS 13, from

the scope of SFAS 157. FSP FAS 157-2 delays the effective date of SFAS 157 for nonfinancial assets and nonfinancial liabilities, except for items that are

recognized or disclosed at fair value on a recurring basis, to fiscal years beginning after November 15, 2008. For all other items, SFAS 157 was effective for

Nordstrom as of February 3, 2008. We have adopted SFAS 157 as amended by FSP FAS 157-1 and FSP FAS 157-2 as of February 3, 2008. This adoption will not

have a material effect on our consolidated financial statements.

In February 2007, the FASB issued Statement of Financial Accounting Standards No. 159,

The Fair Value Option for Financial Assets and Financial Liabilities

(“SFAS 159”). SFAS 159 permits entities to choose to measure many financial instruments and certain other items at fair value. SFAS 159 was effective for

Nordstrom as of February 3, 2008. We did not apply the fair value option to any of our outstanding instruments; therefore, SFAS 159 will have no effect on

our consolidated financial statements.

In December 2007, the FASB issued Statement of Financial Accounting Standards No. 141 (Revised 2007),

Business Combinations

(“SFAS 141(R)”). SFAS 141(R)

will significantly change the accounting for business combinations. Under SFAS 141(R), an acquiring entity will be required to recognize all the assets

acquired and liabilities assumed in a transaction at the acquisition-date fair value with limited exceptions. SFAS 141(R) will change the accounting treatment

for certain specific acquisition-related items, including expensing acquisition-related costs as incurred, valuing noncontrolling interests (minority interests)

at fair value at the acquisition date, and expensing restructuring costs associated with an acquired business. SFAS 141(R) also includes a substantial number

of new disclosure requirements. SFAS 141(R) is to be applied prospectively to business combinations for which the acquisition date is on or after January 1,

2009. Early adoption is not permitted. Generally, the effect of SFAS 141(R) will depend on future acquisitions.

Also in December 2007, the FASB issued Statement of Financial Accounting Standards No. 160,

Noncontrolling Interests in Consolidated Financial Statements

– an amendment of ARB No. 51

(“SFAS 160”). SFAS 160 establishes new accounting and reporting standards for noncontrolling interest (minority interest) in a

subsidiary, provides guidance on the accounting for and reporting of the deconsolidation of a subsidiary, and increases transparency through expanded

disclosures. Specifically, SFAS 160 requires the recognition of minority interest as equity in the consolidated financial statements and separate from the

parent company’s equity. It also requires consolidated net earnings in the consolidated statement of earnings to include the amount of net earnings

attributable to minority interest. This statement will be effective for Nordstrom as of the beginning of fiscal year 2009. Early adoption is not permitted.

We are presently evaluating the impact of the adoption of SFAS 160 and believe there will be no material impact on our consolidated financial statements.