Neiman Marcus 2002 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2002 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

|

|

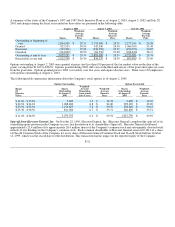

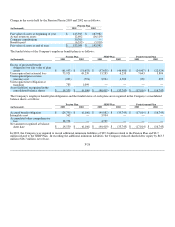

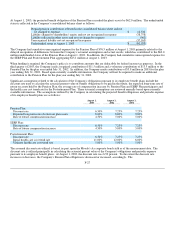

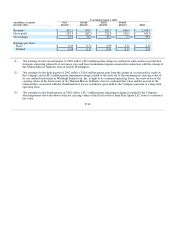

estimated effect of a 0.25 percent decrease in the discount rate would increase the Pension Plan obligation by $7.4 million and

increase annual Pension Plan expense by $1.2 million. The estimated effect of a 0.25 percent decrease in the discount rate would

increase the SERP Plan obligation by $1.5 million and increase the SERP Plan annual expense by $0.2 million. The estimated effect

of a 0.25 percent decrease in the discount rate would increase the Postretirement Plan obligation by $0.7 million and increase the

Postretirement Plan annual expense by an immaterial amount.

The assumed expected long-term rate of return on assets is the weighted average rate of earnings expected on the funds invested or to

be invested to provide for the pension obligation. It is the Company's current policy to invest the Pension Plan assets in equity

securities (approximately 60 percent) and in fixed income securities (approximately 40 percent). The Company periodically evaluates

the allocation between investment categories of the assets held by the Pension Plan. The expected average long-term rate of return on

assets is based principally on the counsel of the Company's outside actuaries and advisors. This rate is utilized primarily in calculating

the expected return on plan assets component of the annual pension expense. To the extent the actual rate of return on assets realized

over the course of a year is greater than the assumed rate, that year's annual pension expense is not affected. Rather this gain reduces

future pension expense over a period of approximately 12 to 18 years. To the extent the actual rate of return on assets is less than the

assumed rate, that year's annual pension expense is likewise not affected. Rather this loss increases pension expense over

approximately 12 to 18 years. During 2003, the Company utilized 8.0 percent as the expected long-term rate of return on plan assets.

The assumed average rate of compensation increase is the average annual compensation increase expected over the remaining

employment periods for the participating employees. The Company utilized a rate of 4.5 percent for the periods beginning August 1,

2003. This rate is utilized principally in calculating the pension obligation and annual pension expense. The estimated effect of a 0.25

percent increase in the assumed rate of compensation increase would increase the pension obligation by $1.5 million and increase

annual pension expense by $0.4 million. The estimated effect of a 0.25 percent increase in the assumed rate of compensation increase

would increase the SERP Plan obligation by $0.7 million and increase the SERP Plan annual expense by $0.2 million.

If the assumed health care trend rate were increased one percentage point, Postretirement Plan costs for 2003 would have been $0.2

million higher and the accumulated postretirement benefit obligation as of August 2, 2003 would have been $2.4 million higher. If the

assumed health care trend rate were decreased one percentage point, Postretirement Plan costs for 2003 would have been $0.2 million

lower and the accumulated postretirement benefit obligation as of August 2, 2003 would have been $2.1 million lower.

The Company has a qualified defined contribution 401(k) plan, which covers substantially all employees. Employees make

contributions to the plan and the Company matches 100 percent of the first 2 percent and 25 percent of the next 4 percent of an

employee's contribution up to a maximum of 6 percent of the employee's compensation. Prior to January 1, 2001, the Company

matched 65 percent of the first 2 percent and 25 percent of the next 4 percent of an employee's contribution up to a maximum of 6

percent of the employee's compensation. The Company also sponsors an unfunded key employee deferred compensation plan, which

provides certain employees additional benefits, a profit sharing and retirement plan for employees of Kate Spade LLC and a qualified

defined contribution 401(k) plan for employees of Gurwitch Products, LLC. The Company's aggregate contributions to these plans

were approximately $9.3 million for 2003, $8.9 million for 2002 and $6.1 million for 2001. Benefits under the plans are based on the

employees' years of service and compensation over defined periods of employment.

NOTE 10. Effect of Change in Vacation Policy

During the third quarter of 2002, the Company terminated its prior vacation plan and the Board of Directors of the Company approved

a new policy related to vacation pay for its employees. The new policy was communicated to employees during the third quarter of

2002. Pursuant to the new policy, which was effective as of April 28, 2002, eligible employees earn vacation pay ratably over the

course of the year in which the services are rendered.

F-28