Neiman Marcus 2002 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2002 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

|

|

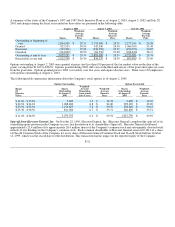

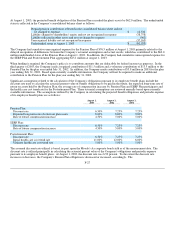

The Company and Harcourt General were parties to an agreement pursuant to which Harcourt General provided certain management,

accounting, financial, legal, tax and other corporate services to the Company. The fees for these services were based on Harcourt

General's costs and were subject to the approval of a special review committee of the Board of Directors of the Company who were

independent of Harcourt General. The agreement with Harcourt General was terminated effective May 14, 2001. The termination of

the agreement with Harcourt General did not have a material effect on the Company's results of operations. There were no charges to

the Company in 2003 or 2002. Charges to the Company amounted to $5.2 million in 2001.

The Company is required to indemnify Harcourt General, and each entity of the consolidated group of which Harcourt General is a

member, against all federal, state and local taxes incurred by Harcourt General or any member of such group as a result of the failure

of the Spin-off to qualify as a tax-free transaction under Section 355(a) of the Internal Revenue Service Code (Code) or the application

of Section 355(e). The obligation to indemnify occurs only if the Company takes action which is inconsistent with any representation

or statement made to the Internal Revenue Service in connection with the request by Harcourt General for a ruling letter in respect to

the Spin-off and as to certain tax aspects of the Spin-off, or if within two years after the date of the Spin-off the Company 1) fails to

maintain its status as a company engaged in the active conduct of a trade or business, as defined in Section 355(b) of the Code, 2)

merges or consolidates with or into any other corporation, 3) liquidates or partially liquidates, 4) sells or transfers all or substantially

all of its assets in a single transaction or a series of related transactions, 5) redeems or otherwise repurchases any Company stock

subject to certain exceptions, or 6) takes any other action or actions which in the aggregate would have the effect of causing or

permitting one or more persons to acquire, directly or indirectly, stock representing a 50 percent or greater interest in the Company.

The Company's obligation to indemnify Harcourt General and its consolidated group shall not apply if, prior to taking any such action

the Company has obtained and provided to Harcourt General a written opinion from a law firm acceptable to Harcourt General, or

Harcourt General has obtained a supplemental ruling from the Internal Revenue Service, that such action or actions will not result in

either (i) the Spin-off failing to qualify under Section 355(a) of the Code, or (ii) the Company's shares failing to qualify as qualified

property for purposes of Section 355(c)(2) of the Code by reason of Section 355(e) of the Code.

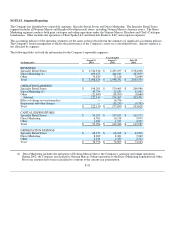

NOTE 7. Stock Repurchase Program

In prior years, the Company's Board of Directors authorized various stock repurchase programs and increases in the number of shares

subject to repurchase. During the second quarter of 2003, the Company repurchased 524,177 shares at an average purchase price of

$28.65. During 2002 and 2001, there were no stock repurchases under the stock repurchase program. As of August 2, 2003,

approximately 1.4 million shares remain available for repurchase under the Company's stock repurchase programs.

F-22