Neiman Marcus 2002 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2002 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

|

|

Recoverability of goodwill and intangible assets is assessed annually and upon the occurrence of certain events. The recoverability

assessment requires management to make judgments and estimates regarding the fair values. The fair values are determined using

estimated future cash flows, including growth assumptions for future sales, gross margin rates and other estimates. To the extent that

management's estimates are not realized, future assessments could result in impairment charges.

Benefit Plans. The Company sponsors a noncontributory defined benefit pension plan (Pension Plan) covering substantially all full-

time employees. In calculating its pension obligations and related pension expense, the Company makes various assumptions and

estimates, after consulting with outside actuaries and advisors. The annual determination of pension expense involves calculating the

estimated total benefit ultimately payable to Pension Plan participants and allocates this cost to the periods in which services are

expected to be rendered. The Company uses the projected unit credit method in recognizing pension liabilities. The Pension Plan is

valued annually as of the beginning of each fiscal year.

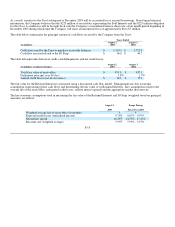

Significant assumptions related to the calculation of the Company's pension obligations include the discount rate used to calculate the

actuarial present value of benefit obligations to be paid in the future, the expected long-term rate of return on assets held by the

Pension Plan and the average rate of compensation increase by Pension Plan participants. These actuarial assumptions are reviewed

annually based upon currently available information.

Self-insurance and Other Employee Benefit Reserves. Management uses estimates in the determination of the required accruals for

general liability, workers' compensation and health insurance as well as short-term disability, supplemental executive retirement

benefits and postretirement health care benefits. These estimates are based upon an examination of historical trends, industry claims

experience and, in certain cases, calculations performed by third-party experts. Projected claims information may change in the future

and may require management to revise these accruals.

Other Long-term Liabilities. Other long-term liabilities consist primarily of certain employee benefit obligations, postretirement

health care benefit obligations and the liability for scheduled rent increases.

Revenues. Revenues include sales of merchandise and services, net commissions earned from leased departments in the Company's

retail stores and shipping and handling revenues related to merchandise sold. Revenues from the Company's retail operations are

recognized at the later of the point of sale or the delivery of goods to the customer. Revenues from the Company's direct marketing

operation are recognized when the merchandise is delivered to the customer. The Company maintains reserves for anticipated sales

returns primarily based on the Company's historical trends related to returns by its retail and direct marketing customers.

Buying and Occupancy Costs. The Company's buying costs consist primarily of salaries and expenses incurred by the Company's

merchandising and buying operations. Occupancy costs primarily include rent, depreciation, property taxes and operating costs of the

Company's retail and distribution facilities.

Selling, General and Administrative Expenses. Selling, general and administrative expenses are comprised principally of the costs

related to employee compensation and benefits in the selling and administrative support areas, preopening expenses, advertising and

catalogue costs, loyalty program costs, insurance expense and income and expenses related the Company's credit card portfolio.

The Company receives allowances from certain merchandise vendors in conjunction with compensation programs for employees who

sell the vendors' merchandise. These allowances are netted against the related compensation expense incurred by the Company.

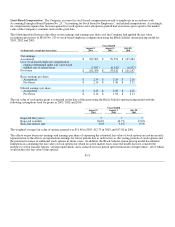

Amounts received from vendors related to compensation programs were $41.1 million in 2003, $37.0 million in 2002 and $33.5

million in 2001.

Preopening Expenses. Preopening expenses primarily consist of payroll and related media costs incurred in connection with new and

replacement store openings and are expensed when incurred. Preopening expenses were $8.0 million for 2003, $5.2 million for 2002

and $2.2 million for 2001.

F-11