Motorola 2006 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2006 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

90

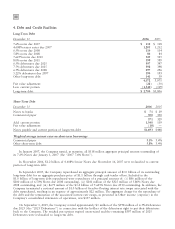

The Company is exposed to credit-related losses if counterparties to financial instruments fail to perform their

obligations. However, the Company does not expect any counterparties, all of whom presently have investment

grade credit ratings, to fail to meet their obligations.

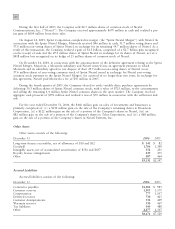

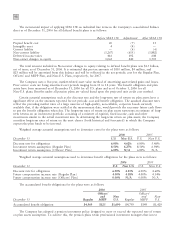

Interest Rate Risk

At December 31, 2006, the Company's short-term debt consisted primarily of $300 million of commercial

paper, priced at short-term interest rates. The Company has $4.1 billion of long-term debt, including the current

portion of long-term debt, which is primarily priced at long-term, fixed interest rates.

In order to manage the mix of fixed and floating rates in its debt portfolio, the Company has entered into

interest rate swaps to change the characteristics of interest rate payments from fixed-rate payments to short-term

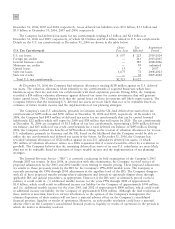

LIBOR-based variable rate payments. The following table displays these outstanding interest rate swaps at

December 31, 2006:

Notional Amount

Date Executed Hedged Underlying Debt Instrument

August 2004 $1,200 4.608% notes due 2007

September 2003 457 7.625% debentures due 2010

September 2003 600 8.0% notes due 2011

May 2003 114 6.5% notes due 2008

May 2003 84 5.8% debentures due 2008

May 2003 69 7.625% debentures due 2010

March 2002 118 7.6% notes due 2007

$2,642

The weighted average short-term LIBOR-based variable rate payments on each of the above interest rate swaps

was 7.29% for the three months ended December 31, 2006. The fair value of the above interest rate swaps at

December 31, 2006 and 2005, was $(47) million and $(50) million, respectively. Except as noted below, the

Company had no outstanding commodity derivatives, currency swaps or options relating to debt instruments at

December 31, 2006 or December 31, 2005.

The Company designated the above interest rate swap agreements as part of a fair value hedging relationship.

As such, changes in the fair value of the hedging instrument, as well as the hedged debt are recognized in earnings,

therefore adjusting the carrying amount of the debt. Interest expense on the debt is adjusted to include the

payments made or received under such hedge agreements. In the event the underlying debt instrument matures or is

redeemed or repurchased, the Company is likely to terminate the corresponding interest rate swap contracts.

Additionally, effective December 31, 2006, one of the Company's European subsidiaries entered into interest

rate agreements (""Interest Agreements'') relating to a Euro-denominated loan. The interest on the Euro-

denominated loan is floating based on 3-month EURIBOR plus a spread. The Interest Agreements change the

characteristics of interest rate payments from short-term EURIBOR based variable payments to maximum fixed-rate

payments. The Interest Agreements are not accounted for as part of a hedging relationship and accordingly the

changes in the fair value of the Interest Agreements are included in Other income (expense) in the Company's

consolidated statements of operations. The fair value of the Interest Agreements at December 31, 2006 was

$1 million.

The Company is exposed to credit loss in the event of nonperformance by the counterparties to its swap

contracts. The Company minimizes its credit risk on these transactions by only dealing with leading, creditworthy

financial institutions having long-term debt ratings of ""A'' or better and, does not anticipate nonperformance. In

addition, the contracts are distributed among several financial institutions, thus minimizing credit risk concentration.