Motorola 2006 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2006 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

89

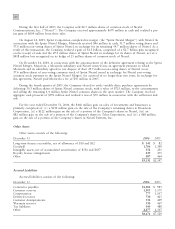

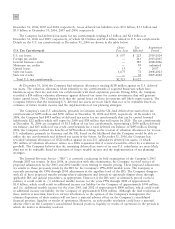

In 2004, the Company retired approximately $2.3 billion of debt, including $1.8 billion of debt retired prior to

maturity. The net charge for the repurchase of the debt and the termination of the associated interest rate swaps, as

presented in Other income (expense) in the Company's consolidated statements of operations, was $81 million.

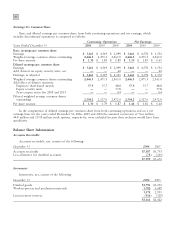

Aggregate requirements for long-term debt maturities during the next five years are as follows: 2007 Ì

$1.3 billion; 2008 Ì $198 million; 2009 Ì $4 million; 2010 Ì $534 million; 2011 Ì $607 million.

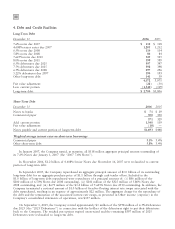

In December 2006, the Company signed a new five-year revolving domestic credit facility (""5-Year Credit

Facility'') for $2.0 billion, replacing the existing facility totaling $1.0 billion. At December 31, 2006, the

commitment fee assessed against the daily average amounts unused was 6.5 basis points. Important terms of the

5-Year Credit Facility include a covenant relating to the ratio of total debt to EBITDA. The Company was in

compliance with the terms of the 5-year Credit Facility at December 31, 2006. The Company's current corporate

credit ratings are ""A¿'' with a stable outlook by Fitch, ""Baa1'' with a positive outlook by Moody's, and ""A¿''

with a stable outlook by S&P. The Company has never borrowed under its domestic revolving credit facilities. The

Company also has $2.0 billion of non-U.S. credit facilities with interest rates on borrowings varying from country to

country depending upon local market conditions. At December 31, 2006, the Company's total domestic and

non-U.S. credit facilities totaled $4.0 billion, of which $175 million was considered utilized.

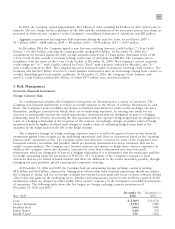

5. Risk Management

Derivative Financial Instruments

Foreign Currency Risk

As a multinational company, the Company's transactions are denominated in a variety of currencies. The

Company uses financial instruments to reduce its overall exposure to the effects of currency fluctuations on cash

flows. The Company's policy prohibits speculation in financial instruments for profit on the exchange rate price

fluctuation, trading in currencies for which there are no underlying exposures, or entering into trades for any

currency to intentionally increase the underlying exposure. Instruments that are designated as part of a hedging

relationship must be effective at reducing the risk associated with the exposure being hedged and are designated as

a part of a hedging relationship at the inception of the contract. Accordingly, changes in market values of hedge

instruments must be highly correlated with changes in market values of underlying hedged items both at the

inception of the hedge and over the life of the hedge contract.

The Company's strategy in foreign exchange exposure issues is to offset the gains or losses on the financial

instruments against losses or gains on the underlying operational cash flows or investments based on the operating

business units' assessment of risk. The Company enters into derivative contracts for some of the Company's non-

functional currency receivables and payables, which are primarily denominated in major currencies that can be

traded on open markets. The Company uses forward contracts and options to hedge these currency exposures. In

addition, the Company enters into derivative contracts for some firm commitments and some forecasted

transactions, which are designated as part of a hedging relationship if it is determined that the transaction qualifies

for hedge accounting under the provisions of SFAS No. 133. A portion of the Company's exposure is from

currencies that are not traded in liquid markets and these are addressed, to the extent reasonably possible, through

managing net asset positions, product pricing and component sourcing.

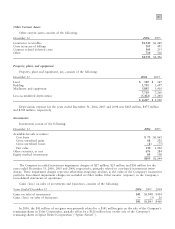

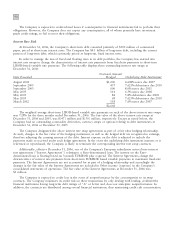

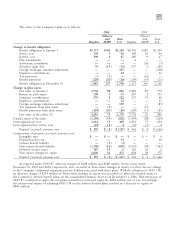

At December 31, 2006 and 2005, the Company had net outstanding foreign exchange contracts totaling

$4.8 billion and $2.8 billion, respectively. Management believes that these financial instruments should not subject

the Company to undue risk due to foreign exchange movements because gains and losses on these contracts should

offset losses and gains on the underlying assets, liabilities and transactions, except for the ineffective portion of the

instruments, which are charged to Other within Other income (expense) in the Company's consolidated statements

of operations. The following table shows the five largest net foreign exchange contract positions as of

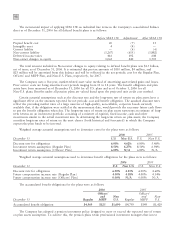

December 31, 2006 and 2005:

December 31,

December 31,

Buy (Sell)

2006

2005

Euro $(2,069) $(1,076)

Chinese Renminbi (1,195) (728)

Brazilian Real (466) (348)

Indian Rupee (148) (70)

British Pound 252 (226)