Kodak 2014 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2014 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

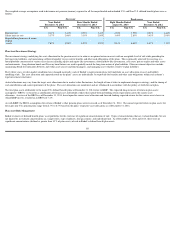

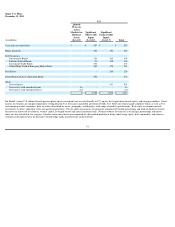

Leeds Plate Manufacturing Facility Exit

On March 3, 2014, Kodak announced a plan to exit its prepress plate manufacturing facility located in Leeds, England. This decision was pursuant to Kodak’s initiative to

consolidate manufacturing operations globally, and is expected to result in a more efficient delivery of its products and solutions. Kodak began the exit of the facility in the

second quarter of 2014, and expects to phase out production at the site from mid to late 2015 and to complete the exit of the facility by the second quarter of 2016.

As a result of the decision, Kodak originally expected to incur total charges of $30 to $40 million, including $8 to $10 million of charges related to separation benefits, $20 to

$25 million of non-cash related charges for accelerated depreciation and asset write-offs and $2 to $5 million in other cash related charges associated with this action. Based

on refinements in estimates, Kodak now expects to incur total charges of $20 to $30 million, including $10 to $15 million of non-cash related charges for accelerated

depreciation and asset write-offs. The estimates for separation benefits and other cash related charges remain unchanged.

Kodak implemented certain actions under this program during 2014. As a result of these actions, Kodak recorded severance charges of $3 million, long-

lived asset impairment

charges of $2 million, and accelerated depreciation charges of $2 million.

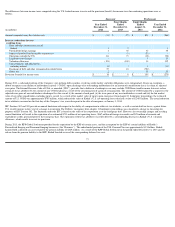

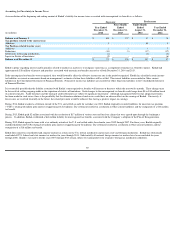

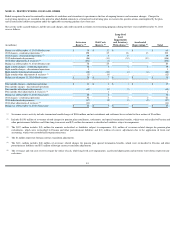

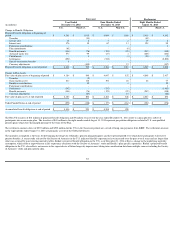

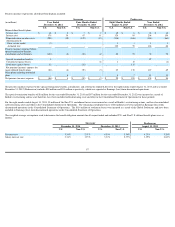

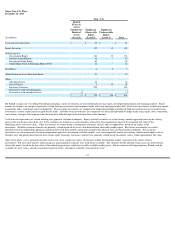

NOTE 16: RETIREMENT PLANS

Substantially all U.S. employees are covered by a noncontributory defined benefit plan, the Kodak Retirement Income Plan (“KRIP”), which is funded by Company

contributions to an irrevocable trust fund. The funding policy for KRIP is to contribute amounts sufficient to meet minimum funding requirements as determined by

employee benefit and tax laws plus any additional amounts the Company determines to be appropriate. Assets in the trust fund are held for the sole benefit of

participating employees and retirees. They are composed of corporate equity and debt securities, U.S. government securities, partnership investments, interests in pooled

funds, commodities, real estate, and various types of interest rate, foreign currency, debt, and equity market financial instruments.

For U.S. employees hired prior to March 1999 KRIP’s benefits were generally based on a formula recognizing length of service and final average earnings. KRIP

included a separate cash balance formula for all U.S. employees hired after February 1999, as well as employees hired prior to that date who opted in to the cash balance

formula during a special election period. In July of 2014 the Company announced an amendment to KRIP, effective January 1, 2015, in which all participants will accrue

benefits under a single, revised cash balance formula (the “Cash Balance Plan”). The Cash Balance Plan credits employees' hypothetical accounts with an amount equal

to 7% of their pay, plus interest based on the 30-year Treasury bond rate. As part of the KRIP amendment, the Company match on contributions to the Savings and

Investment Plan (“SIP”), a defined contribution plan, of up to 3% for employees participating under the previous 4% cash balance formula has been eliminated. The

Company’s contributions to SIP were $5 million and $6 million for 2014 and 2013, respectively.

Many subsidiaries and branches operating outside the U.S. have defined benefit retirement plans covering substantially all employees. Contributions by Kodak for these

plans are typically deposited under government or other fiduciary-type arrangements. Retirement benefits are generally based on contractual agreements that provide for

benefit formulas using years of service and/or compensation prior to retirement. The actuarial assumptions used for these plans reflect the diverse economic environments

within the various countries in which Kodak operates.

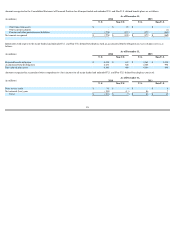

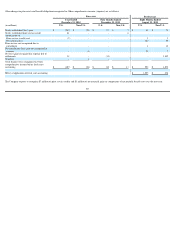

Information on the major funded and unfunded U.S. and Non-U.S. defined benefit pension plans is presented below. The composition of the major plans may vary from year

to year. If the major plan composition changes, prior year data is conformed to ensure comparability.

The measurement date used to determine the pension obligation for all funded and unfunded U.S. and Non-U.S. defined benefit plans is December 31.

83