Kodak 2014 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2014 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

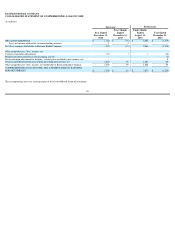

|

|

CASH EQUIVALENTS

All highly liquid investments with a remaining maturity of three months or less at date of purchase are considered to be cash equivalents.

INVENTORIES

Inventories are stated at the lower of cost or market. The cost of all of Kodak’s inventories is determined by the average cost method, which approximates current

cost. Kodak provides inventory reserves for excess, obsolete or slow-moving inventory based on changes in customer demand, technology developments or other

economic factors. In connection with fresh start accounting, Kodak adjusted the net book value of inventories to their estimated fair value as of September 1,

2013. Refer to Note 25, “Fresh Start Accounting.”

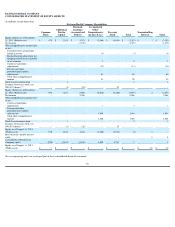

PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment are recorded at cost, net of accumulated depreciation with the exception of property, plant and equipment owned as of the application of

fresh start accounting. Kodak capitalizes additions and improvements while maintenance and repairs are charged to expense as incurred. Upon sale or other disposition,

the applicable amounts of asset cost and accumulated depreciation are removed from the accounts and the net amount, less proceeds from disposal, is charged or credited

to net (loss) earnings. In connection with fresh start accounting, property, plant and equipment were adjusted to their estimated fair value and depreciable lives were

revised as of September 1, 2013. Refer to Note 25, “Fresh Start Accounting.”

Kodak calculates depreciation expense using the straight-line method over the assets’ estimated useful lives, which are as follows:

Kodak depreciates leasehold improvements over the shorter of the lease term or the asset’s estimated useful life.

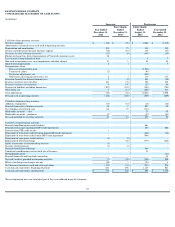

GOODWILL

Goodwill reported in the Successor period represents the reorganizational value of assets in excess of amounts allocated to identified tangible and intangible

assets. Goodwill reported in the Predecessor period represents the excess of purchase price of an acquisition over the fair value of net assets acquired. Goodwill is not

amortized, but is required to be assessed for impairment at least annually. Kodak has historically performed its annual goodwill impairment assessment as of September

30. Upon application of fresh start accounting, Kodak elected October 1 as the annual goodwill impairment assessment date and will perform additional impairment tests

when events or changes in circumstances occur that would more likely than not reduce the fair value of the reporting unit below its carrying amount.

When testing goodwill for impairment, Kodak may assess qualitative factors for some or all of its reporting units to determine whether it is more likely than not (that is, a

likelihood of more than 50 percent) that the fair value of a reporting unit is less than its carrying amount, including goodwill. If Kodak determines based on this

qualitative test of impairment that it is more likely than not that a reporting unit’s fair value is less than its carrying amount, or elects to bypass the qualitative assessment

for some or all of its reporting units, then a two-step goodwill impairment test is performed to test for a potential impairment of goodwill (step 1) and if potential losses

are identified, to measure the impairment loss (step 2). Determining the fair value of a reporting unit involves the use of significant estimates and assumptions. Refer to

Note 5,

“Goodwill and Other Intangible Assets” and Note 25, “Fresh Start Accounting.”

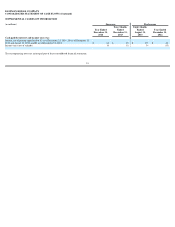

WORKERS COMPENSATION

Kodak self insures and participates in high-deductible insurance programs with retention and per occurrence deductible levels for claims related to workers compensation. The

estimated liability for workers compensation is based on actuarially estimated, discounted cost of claims, including claims incurred but not reported. Historical loss

development factors are utilized to project the future development of incurred losses, and the amounts are adjusted based on actual claim experience, settlements, claim

development trends, changes in state regulations and judicial interpretations. Amounts recoverable from insurance companies or third parties are estimated using historical

experience and estimates of future recoveries. Estimated recoveries are not offset against the related accrual.

Successor

Company

As of

September 1,

2013

Buildings and building improvements

5

-

40

1

-

38

Land improvements

20

1

-

20

Leasehold improvements

3

-

20

1

-

10

Equipment

3

-

15

1

-

20

Tooling

1

-

3

1

-

3

Furniture and fixtures

5

-

10

1

-

10

56