Kodak 2014 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2014 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

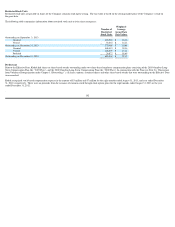

On the Effective Date, the following occurred pursuant to the Amended SAPA and Global Settlement:

SECTION 363 ASSET SALES

On February 1, 2013, Kodak entered into a series of agreements related to the monetization of certain of its intellectual property assets, including the sale of its digital imaging

patents. Under these agreements, Kodak received approximately $530 million, a portion of which was paid by twelve licensees that received a license to the digital imaging

patent portfolio and other patents owned by Kodak. Another portion was paid by Intellectual Ventures Fund 83 LLC (“Intellectual Ventures”) and Apple, Inc., each of which

acquired a portion of the digital imaging patent portfolio, subject to the licenses granted to the twelve new licensees, and previously existing licenses. In addition, Kodak

retained a license to the digital imaging patents for its own use. In connection with this transaction, the Company entered into a separate agreement with FUJIFILM

Corporation (“Fuji”) whereby, among other things, Fuji granted Kodak the right to sub-license certain Fuji patents to businesses Kodak ultimately sold as part of the Plan. The

Debtors also agreed to allow Fuji a general unsecured claim against the Debtors in the amount of $70 million that was discharged pursuant to the terms of the Plan.

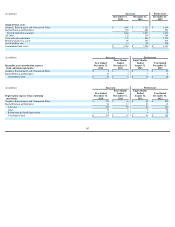

EASTMAN BUSINESS PARK SETTLEMENT AGREEMENT

On June 17, 2013, the Company, the New York State Department of Environmental Conservation and the New York State Urban Development Corporation, d/b/a Empire

State Development entered into a settlement agreement, subsequently amended on August 6, 2013 (the “Amended EBP Settlement Agreement”).

The Amended EBP

Settlement Agreement was subject to the satisfaction or waiver of certain conditions including a covenant not to sue from the EPA. On May 13, 2014, the Bankruptcy Court

approved the U.S. Environmental Settlement, which contained the EPA covenant not to sue, and on May 20, 2014 the Amended EBP Settlement Agreement was implemented

and became effective. The Amended EBP Settlement Agreement included the settlement of certain of the Company’

s historical environmental liabilities at EBP through the

establishment of the EBP Trust as follows: (i) the EBP Trust is responsible for investigation and remediation at EBP arising from the Company’

s historical subsurface

environmental liabilities in existence prior to the effective date of the Amended EBP Settlement Agreement, (ii) the Company funded the EBP Trust on the effective date with

a $49 million cash payment and transferred certain equipment and fixtures used for remediation at EBP and (iii) in the event the historical liabilities exceed $99 million, the

Company will become liable for 50% of the portion above $99 million. Prior to the implementation of the Amended EBP Settlement Agreement, $49 million was already held

in a separate trust and escrow account.

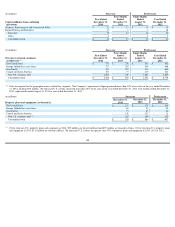

OTHER POSTEMPLOYMENT BENEFITS

On November 7, 2012, the Bankruptcy Court entered an order approving a settlement agreement between the Debtors and the Official Committee of Retired Employees

appointed by the U.S. Trustee under the chapter 11 proceedings (the “Retiree Committee”). Under the settlement agreement, the Debtors no longer provide retiree medical,

dental, life insurance and survivor income benefits to current and future retirees after December 31, 2012 (other than COBRA continuation coverage of medical and/or dental

benefits or conversion coverage as required by applicable benefit plans or applicable law), and the Retiree Committee established a trust from which some limited benefits for

some retirees may be provided after December 31, 2012. The trust or related account was funded by the following contributions from the Debtors: $7.5 million in cash paid by

the Company in the fourth quarter of 2012, an administrative claim against the Debtors in the amount of $15 million that was paid on the Effective Date, and a general

unsecured claim against the Debtors in the amount of $635 million that was discharged upon emergence from chapter 11 pursuant to the terms of the Plan.

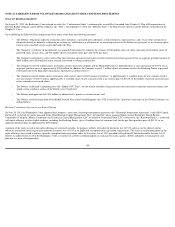

RETIREES

’ SETTLEMENT

The Debtors’ estimated allowed claims for pre-petition obligations for the Kodak Excess Retirement Income Plan (the “KERIP”), the Kodak Unfunded Retirement Income

Plan (the “KURIP”), the Kodak Company Global Pension Plan for International Employees, and individual letter agreements with certain current and former employees that

provided for supplemental non-qualified pension benefits were reported as Liabilities subject to compromise in the accompanying Consolidated Statement of Financial

Position.

On April 30, 2013, Eastman Kodak Retirees Association Ltd. and certain holders of KERIP and KURIP claims (together with the Debtors, the “Settlement Parties”) filed a

motion (the “Motion”) requesting that the Bankruptcy Court appoint a committee pursuant to section 1102(a)(2) of the Bankruptcy Code, to represent the interests of the

holders of the KERIP and KURIP claims, and asserted that they and certain other holders of the KERIP and KURIP claims disagreed with the underlying discount rates and

mortality tables used by the Debtors to calculate the KERIP and KURIP estimated allowed claim amounts. Subsequent to the filing of the Motion, the Settlement Parties

entered into a stipulation (the “Stipulation”) approved by an order of the Bankruptcy Court, which became effective on July 18, 2013, for a total allowed claim of

approximately $244 million. During August 2013 a provision for expected allowed claims of approximately $27 million was reflected in Reorganization Items, net in the

accompanying Consolidated Statement of Operations to increase the recorded liability to what was ultimately agreed to in the Stipulation.

On the Effective Date, the claim was discharged upon emergence pursuant to the terms of the Plan.

• The acquisition by KPP Holdco Limited (“KPP Holdco”), a wholly owned subsidiary of KPP, and certain direct and indirect subsidiaries of KPP Holdco (together

with KPP Holdco, the “KPP Purchasing Parties”), of certain assets of the Business, and the assumption by the KPP Purchasing Parties of certain liabilities of the

Business, for a total purchase price, exclusive of the assumption of liabilities, of $650 million, of which a gross $525 million was paid in cash (net cash consideration

of $325 million) and the balance of which was settled by a $125 million note issued by the KPP (the

“

KPP Note

”

).

• The KPP Note was cancelled after being assigned by the Company to the Subsidiary and subsequently assigned by the Subsidiary to KPP as settlement, by way of

setoff, of an equal amount of outstanding pension liabilities of the Subsidiary to KPP.

• The cash consideration was comprised of $325 million sourced from assets of the U.K. Pension Plan and $200 million sourced from a payment by the Subsidiary to

KPP as payment for outstanding pension liabilities of the Subsidiary to KPP.

• Up to $35 million in aggregate of the purchase price is subject to repayment to KPP if the Business does not achieve certain annual adjusted EBITDA targets over the

four

-

year period ending December 31, 2018.

111