Kia 2007 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2007 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

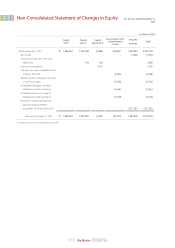

067_

Kia Motors Annual Report 2007

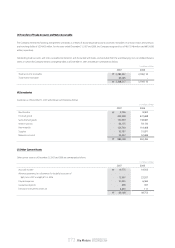

(e) Allowance for Doubtful Accounts

Allowance for doubtful accounts is estimated based on an analysis of individual accounts and past experience of collection. However, when principals of trade

accounts and notes receivable, interest rate or repayment period are changed unfavorably for the creditor by a court imposition, such as on commencement of

reorganization, or by mutual agreement with the Company, and the difference between nominal value and present value is material, the difference is recognized as

bad debt expense.

(f) Transfer of Assets

Transfers of financial assets to third parties are accounted for as sales when control is surrendered to the transferee. The Bank derecognizes financial assets from the

balance sheet including any related allowance, and recognizes all assets obtained, and liabilities incurred, including any recourse obligations to the transferee, at fair

value. Any resulting gain or loss on the sale is recognized in earnings. Conversely, the Bank only recognizes financial assets transferred from third parties on the

balance sheet when the Bank obtains control of financial assets.

(g) Inventories

Inventories are stated at the lower of cost or net realizable value. Net realizable value is the estimated selling price in the ordinary course of business, less the

estimated selling costs. The cost of inventories is determined on the specific identification method for materials in transit and on the moving-average method for all

other inventories. Amounts of inventory written down to net realizable value due to losses occurring in the normal course of business are recognized as cost of

goods sold and are deducted as an allowance from the carrying value of inventories.

The Company recognizes interest costs and other financial charges on borrowings associated with inventories that require a long period in the acquisition,

construction or production as an expense in the period in which they are incurred.

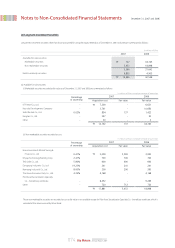

(h) Investments in Securities (excluding in associates, subsidiaries)

Classification

Upon acquisition, the Company classifies certain debt and equity securities(excluding investments in subsidiaries, associates) into one of the three categories: held-

to-maturity, available-for-sale, or trading securities and such determination is reassessed at each balance sheet date.

Investments in debt securities where the Company has the positive intent and ability to hold to maturity are classified as held-to-maturity. Securities that are bought

and held principally for the purpose of selling them in the near term (thus held for only a short period of time) are classified as trading securities. Trading generally

reflects active and frequent buying and selling, and trading securities are generally used to generate profit on short-term differences in price. Investments not

classified as either held-to-maturity or trading securities are classified as available-for-sale securities.

Initial recognition

Investments in securities (excluding investments in subsidiaries, associates) are initially recognized at cost, which consists of the market price of the consideration

given to acquire them and incidental expenses.

Subsequent measurement and income recognition

Trading securities are carried at fair value, with unrealized holding gains and losses included in current income. Available-for-sale securities are carried at fair value,

with unrealized holding gains and losses reported as accumulated other comprehensive income, net of tax. Investments in equity securities that do not have readily

determinable fair values are stated at cost. Investments in debt securities that are classified into held-to-maturity are reported at amortized cost at the balance sheet

date and such amortization is included in interest income.

Fair value information

The fair value of marketable securities is determined using quoted market prices as of the period end. Non-marketable debt securities are recorded at the fair values

derived from the discounted cash flows by using an interest rate deemed to approximate the market interest rate. The market interest rate is determined by the

issuers’ credit rate announced by the accredited credit rating agencies in Korea. Money market funds are recorded at the fair value determined by the investment

management companies.