Haier 2007 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2007 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

|

|

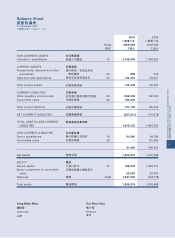

71

Haier Electronics Group Co., Ltd. Annual Report 2007

海爾電器集團有限公司 二零零七年年報

Notes to Financial Statements

財務報表附註

31 December 2007

二零零七年十二月三十一日

2.4 Summary of Significant Accounting

Policies (Cont’d)

Joint ventures

A joint venture is an entity set up by contractual

arrangement, whereby the Group and other parties

undertake an economic activity. The joint venture

operates as a separate entity in which the Group and

the other parties have an interest.

The joint venture agreement between the venturers

stipulates the capital contributions of the joint

venture parties, the duration of the joint venture entity

and the basis on which the assets are to be realised

upon its dissolution. The profits and losses from the

joint venture’s operations and any distributions of

surplus assets are shared by the venturers, either in

proportion to their respective capital contributions,

or in accordance with the terms of the joint venture

agreement.

A joint venture is treated as:

(a) a subsidiary, if the Group has unilateral control,

directly or indirectly, over the joint venture;

(b) a jointly-controlled entity, if the Group does not

have unilateral control, but has joint control,

directly or indirectly, over the joint venture;

(c) an associate, if the Group does not have

unilateral or joint control, but holds, directly or

indirectly, generally not less than 20% of the

joint venture’s registered capital and is in a

position to exercise significant influence over

the joint venture; or

(d) an equity investment accounted for in

accordance with HKAS 39, if the Group holds,

directly or indirectly, less than 20% of the joint

venture’s registered capital and has neither

joint control of, nor is in a position to exercise

significant influence over, the joint venture.

2.4 主要會計政策概要

(續)

合資企業

合資企業為按合約按排成立之實體,由此本

集團及其他訂約方承擔一經濟活動。該合資

企業乃本集團及其他訂約方擁有權益之獨立

經營實體。

合資各方訂立之合營企業協議訂明合資各方

之出資額、合資期限以及於合資企業解散時

將予變現資產之基準。合資企業之經營損益

及任何盈餘資產由合營各方按彼等各自之出

資額比例或按合資企業協議之條款進行分

配。

合資企業會被視為:

(a) 附屬公司,如本集團對合資企業直接

或間接擁有單方面之控制權;

(b) 共同控制實體,如本集團對合資企業

並無單方面控制權,但有直接或間接

共同控制權;

(c) 聯營公司,如本集團並無單方面或共

同之控制權,但直接或間接持有一般

不少於20%之合資企業註冊資本及對

其有重大影響力;或

(d) 按其指示香港會計準則第39 號處理之

股份投資,如本集團直接或間接持有

不足20% 之合資企業註冊資本,且對

合資企業並無共同控制權,或對其並

無重大影響力。