GNC 2008 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2008 GNC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

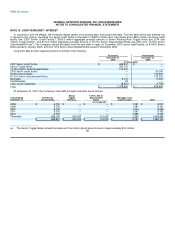

Table of Contents

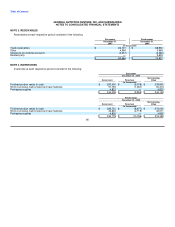

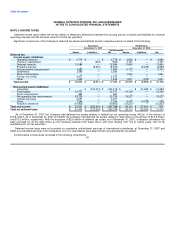

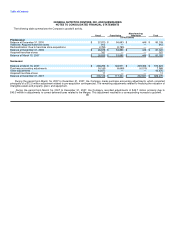

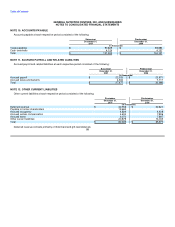

GENERAL NUTRITION CENTERS, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

The Company evaluated the effects of applying SAB 108 and have determined that its adoption does not have a material impact on the

Company's consolidated financial statements or results of operations.

In March 2006, the FASB's EITF issued EITF Abstract Issue No. 06-03, "How Taxes Collected from Customers and Remitted to

Governmental Authorities Should Be Presented in the Income Statement (That is, Gross versus Net Presentation)" ("EITF 06-03"), that clarifies

how a company discloses its recording of taxes collected that are imposed on revenue producing activities. EITF 06-03 is effective for the first

interim reporting period beginning after December 15, 2006. The Company evaluated the effects of applying EITF 06-03 and have determined

that its adoption does not have a material impact on our consolidated financial statements or results of operations.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), "Business Combinations" ("SFAS 141R"). SFAS 141R establishes

principles and requirements for how an acquirer in a business combination recognizes and measures in its financial statements the identifiable

assets acquired, the liabilities assumed and any noncontrolling interest in the acquiree at the acquisition date fair value. SFAS 141R

significantly changes the accounting for business combinations in a number of areas including the treatment of contingent consideration,

preacquisition contingencies, transaction costs, in-process research and development and restructuring costs. In addition, under SFAS 141R,

changes in an acquired entity's deferred tax assets and uncertain tax positions after the measurement period will impact income tax expense.

SFAS 141R provides guidance regarding what information to disclose to enable users of the financial statements to evaluate the nature and

financial effects of the business combination. SFAS 141R is effective for fiscal years beginning after December 15, 2008 with early application

prohibited. SFAS 141R also amends SFAS 109, such that adjustments made to deferred taxes and acquired tax contingencies after January 1,

2009, even for business combinations completed before this date, will impact net income. The Company will adopt SFAS 141R beginning in the

first quarter of fiscal 2009 and is currently evaluating the impact of adopting SFAS 141R on its consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, "Noncontrolling Interests in Consolidated Financial Statements, an amendment of ARB

No. 51" ("SFAS 160"). SFAS 160 changes the accounting and reporting for minority interests, which will be recharacterized as noncontrolling

interests and classified as a component of equity. This new consolidation method significantly changes the accounting for transactions with

minority interest holders. SFAS 160 is effective for fiscal years beginning after December 15, 2008 with early application prohibited. The

Company will adopt SFAS 160 beginning in the first quarter of fiscal 2009 and is currently evaluating the impact of adopting SFAS 160 on its

consolidated financial statements.

In May 2007, the FASB issued FASB Staff Position No. FIN 48-1, "Definition of Settlement in FASB Interpretation No. 48" ("the FSP"). The

FSP provides guidance about how an enterprise should determine whether a tax position is effectively settled for the purpose of recognizing

previously unrecognized tax benefits. Under the FSP, a tax position could be effectively settled on completion of examination by a taxing

authority if the entity does not intend to appeal or litigate the result and it is remote that the taxing authority would examine or re-examine the

tax position. The Company applied the provisions of the FSP during 2007.

79