EasyJet 2014 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2014 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

www.easyJet.com 95

Governance

Area of focus How our audit addressed the area of focus

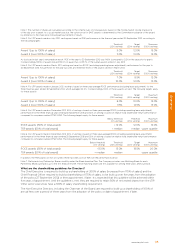

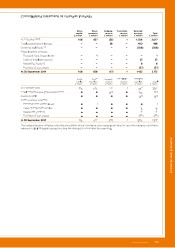

Accruals

The Group records a number of accrual balances which are specific to

the business and its operations. At 30 September 2014, the aggregate

of all accruals is £309 million (refer to notes 1 and 14 to the accounts).

Whilst some accruals are easily and ordinarily calculated and processed,

others contain an element of judgement and are more complex in

nature, for example, customer claims in respect of flight delays,

cancellations and Air Passenger Duty.

We focused on this area because of an inherent level of complexity

in management estimating certain accruals as a result of the

judgements that were to be made. These types of accrual were not

individually material but may, under certain circumstances, be material

in the aggregate.

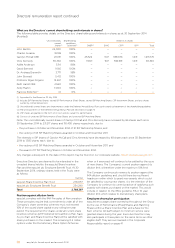

We evaluated the systems, processes and

controls in place over accrual balances and

also assessed key account reconciliation

processes. Amongst other testing, we sought

evidence of post year end cash and other

account movements which provided evidence

as to the validity of the accrual at the year end

and we undertook analytical procedures over

the related income statement cost categories.

We tested and challenged the reasonableness

of the key assumptions underlying certain

accruals, which included passenger claim

history and levels, flight disruptions, no-show

passengers and time periods. We also tested

the accrual input data, reperformed calculations

and performed sensitivity analysis around the

key drivers, as well as considering the likelihood

of material movements to such drivers.

Goodwill and landing rights impairment assessment

Goodwill arises from acquisitions in previous years and has an indefinite

expected useful life. Landing rights (which are an intangible asset)

are considered by management to have an indefinite useful life as

they will remain available for use for the foreseeable future.

Goodwill and landing rights are tested for impairment at least annually

at the cash-generating unit (‘CGU’) level. The Group has one CGU,

being its route network, to which all goodwill and landing rights relate.

At 30 September 2014, they amount, in aggregate, to £459 million

(refer to notes 1 and 8 to the accounts).

We focused on this assessment as the impairment test involves a

number of subjective judgements and estimates by management, many

of which are forward-looking. These estimates include key assumptions

surrounding the strategic plans through to 2019, fuel prices, exchange

rates, long-term economic growth rates and discount rates.

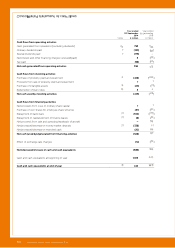

We evaluated and challenged the future cash

flow forecasts of the CGU, and the process

by which they were drawn up, and tested the

underlying value in use calculations. In doing

this, we compared the forecast to the

latest Board approved plans, along with

comparing prior year budget to actual data,

as this informed as to the quality of the

forecasting process.

We also challenged the key assumptions

for fuel prices, exchange rates and long-term

growth rates in the forecasts by comparing

them to economic and industry forecasts;

and the discount rate by assessing the

cost of capital for the Company and

comparable organisations.

We performed sensitivity analysis around the

key assumptions above to ascertain the extent

of change in those assumptions that either

individually or collectively would be required for

the goodwill and landing rights to be impaired.

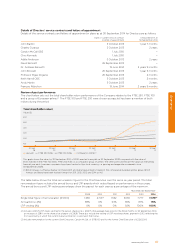

How we tailored the audit scope

We tailored the scope of our audit to ensure that we performed sufficient work to be able to give an opinion on the

accounts as a whole, taking into account the geographic structure of the Group, the accounting processes and controls,

and the industry in which the Group operates.

The Group operates through the Company and its four trading subsidiary undertakings as set out on page 133 and the

Group accounts are a consolidation of these entities. The accounting for these entities is largely centralised in the UK

and our audit scope comprises an audit of their complete financial information. These procedures gave us the evidence

that we needed for our opinion on the Group’s accounts as a whole.